A Modern Gold Rush

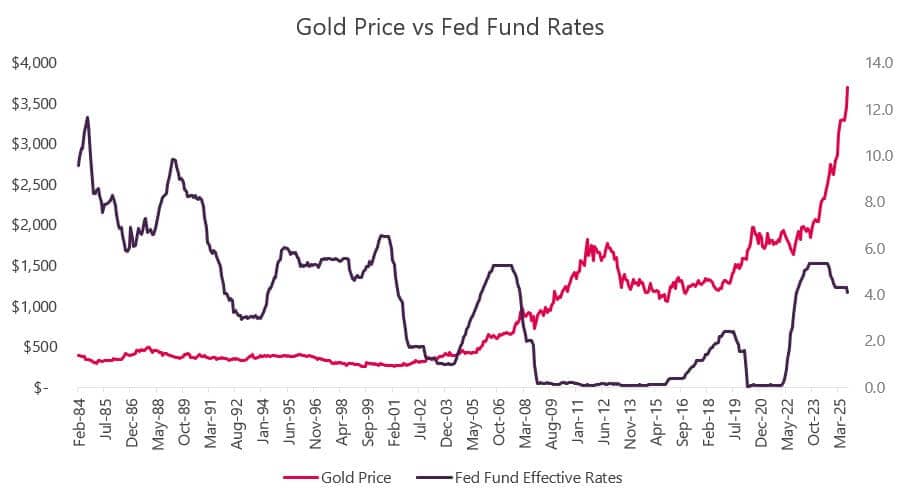

Gold, the age-old symbol of wealth and stability, is experiencing an unprecedented surge in value. Currently it is hovering around $3,800 per ounce, marking a record high and an 83% return since 2024. This meteoric rise resembles a modern gold rush, driven by global uncertainty and structural shifts in the financial landscape. Several trends have fueled this surge, including escalating geopolitical tensions, uncertain macroeconomic policies (particularly the return of aggressive tariff measures and their inflationary effects), a structural shift in global reserve management led by central banks, and strong investor demand. By mid-September 2025, gold prices had risen nearly 42% YTD in US dollar terms, far outpacing the 27% gain in 2024. Last year, the metal broke multiple records and continued its rally in 2025, surpassing $2,900 per ounce in February, $3,500 in April, and about $3,700 in September. Historically, gold has delivered average annual returns of 4–6%, but recent years have produced extraordinary gains. This surge highlights gold’s growing role in diversified portfolios. Figure 1 illustrates key events that triggered major price movements and shows their inverse relationship with interest rates.

Let us explore the key drivers behind the rally, identify sectors positioned to benefit, and present a framework for navigating this unique investment environment to help investors, asset managers, and buy-side research teams understand the powerful forces shaping this new era.

Trends Shaping the Industry

Geopolitical Tensions

As global conflicts and political uncertainties intensify, investors are turning to gold as insurance against market instability and potential crashes. The World Gold Council's (WGC) analysis indicates that without a broad and lasting resolution to current conflicts, demand for gold will remain strong. Figure 3 illustrates the impact of multiple geopolitical events on gold prices over the past five years.

Shift in Reserve Management

Central banks are driving a structural shift in global reserve management as they seek to diversify away from the US dollar. Concerns over potential sanctions and the need for greater financial autonomy in an increasingly multipolar world have accelerated this trend. These banks have been on a gold-buying spree, extending their accumulation for 15 consecutive years. In 2024, net central bank demand exceeded 1,000-tonnes for the third year in a row, far above the 490-tonne annual average recorded between 2014 and 2021. This strong buying momentum is expected to continue, with purchases estimated at 900-tonnes in 2025 and similar levels projected for 2026.

Moreover, the freezing of Russia’s foreign reserves by Western nations after the Ukraine conflict served as a wake-up call for many central banks. It showed that even US dollar-denominated assets could be weaponized and seized. This realization has accelerated an existing trend of de-dollarization among many countries, from major economies like China to smaller emerging markets. Central banks are buying gold not only to hedge against inflation or a weakening dollar but also to protect financial sovereignty and national security. This creates a strong, long-term demand floor for gold that is less sensitive to short-term economic fluctuations.

Concerns about US debt and fiscal policy add another layer to this trend. Holding a large share of reserves in US government bonds is essentially a bet on the country’s long-term fiscal stability. Central banks are becoming increasingly cautious about the US’s growing debt burden. As debt-to-GDP ratios climb and political gridlock clouds fiscal policy, many central banks are reassessing their exposure to US assets. This shift benefits gold, which carries zero sovereign risk. Unlike government bonds, gold is a tangible asset with no counterparty risk. The move away from Treasuries and towards gold signals a fundamental change in how central banks perceive risk.

Fear of Recession and Tariffs

Tariffs act as a catalyst for cost-push inflation, making it harder for central banks such as the Federal Reserve to maintain monetary policy targets. Uncertainty about future interest rate decisions, the potential for a ‘stagflationary’ environment, and fears of a recession are expected to reinforce gold's safe-haven appeal and push prices higher by 10–15%. US President Trump's aggressive tariff announcements, 50% on India, 15% on the European Union, 25% on Mexico, and additional tariffs on 14 other countries, including Japan and South Korea, have triggered retaliatory measures and created significant market volatility. These developments are driving investors towards gold as a safe asset. Moreover, countries that export to the US will likely experience slower GDP growth due to retaliatory tariffs and a decline in global trade.

In addition, the consumer sentiment index dropped to 55.4 in September 2025, down from 58.2 in August and 61.7 in July. However, the probability of a recession this year has fallen sharply to 8% from 70% in May, according to Kalshi. Market expectations of such an environment, combined with these drivers, position gold for sustained gains.

Falling US Dollar

As the dollar weakens, gold becomes more attractive to foreign buyers, reinforcing the US Dollar Index's (DXY) inverse relationship with the metal. The structural decline in the US dollar's share of global reserves underscores a long-term diversification trend, with gold serving as a politically neutral and universally recognized alternative. The DXY represents a weighted average of six major currencies: euro, Japanese yen, pound sterling, Canadian dollar, Swedish krona, and Swiss franc. An increase in DXY signals a stronger US dollar, while a decline indicates a weaker dollar.

Figure 7 illustrates this inverse relationship. After tariff announcements, gold prices began to rise while the DXY started to fall. More notably, the US dollar's share of global reserves dropped by 0.62 percentage points to 57.8% in 2024. This trend suggests a broader effort by central banks and other large institutional investors to diversify away from the US dollar. Gold, as a universally recognized and politically neutral asset, remains an ideal alternative.

Surge in Gold Investment Products

Globally, gold exchange-traded funds (ETFs) recorded unprecedented inflows, with total assets under management (AUM) rising 41% to $383 billion in the first half of 2025. During the period, total holdings in these ETFs increased by 397 tonnes to 3,616 tonnes, the highest month-end level since August 2022. Investor demand for gold is projected to remain strong, averaging about 710 tonnes per quarter this year. Non-commercial futures and options long positions in COMEX gold, the primary market for trading metal derivatives, reached a new high in 2024, signaling strong speculative and hedging interest. Combined holdings in bars, coins, ETFs, and net non-commercial futures positions in COMEX gold grew 3% year over year in 2024 to approximately 49,400 tonnes, including about 45,400 tonnes of physical bars and coins held by private investors.

The record AUM in ETFs, elevated futures positioning, and sustained demand for physical gold reflect investors' confidence in gold's tangible safe-haven qualities. These factors provide significant depth, liquidity, and resilience to the gold market, making it less vulnerable to single-factor shocks or abrupt reversals.

Sectors Poised to Benefit from Gold’s Rally

The outlook for gold remains strong, supported by the same forces that drove its recent surge. The WGC’s analysis, based on its Gold Valuation Framework, projects that under current consensus expectations for key macroeconomic variables, gold will likely stay rangebound in the second half of 2025, closing 0–5% higher than current levels, equivalent to a 30–35% annual return. The WGC estimates if economic and financial conditions worsen, safe-haven demand could push gold prices 10–15% higher from current levels, but if a broad and lasting resolution of global conflicts is achieved (an unlikely outcome in the current environment), prices could dip by 12–17%.

Key factors to watch include US trade policy and global tariffs, inflation trends (especially cost-push elements), central bank monetary policy responses (with a focus on real interest rates), and geopolitical developments. The trend of higher central bank buying and sustained investor interest in ETFs and futures markets is expected to provide a strong demand floor for gold.

While direct investment in bullion, ETFs, or futures offers straightforward exposure, deeper analysis reveals that several sectors and companies are also poised to benefit from the sustained strength in gold:

- Gold Mining: Rising gold prices can significantly boost profitability due to fixed and semi-fixed operating costs. Higher revenue from gold sales often expands margins faster than the price of gold itself. Investors can gain exposure through individual stocks (e.g., Newmont, Barrick Gold) or gold mining ETFs (e.g., VanEck Gold Miners ETF). However, mining stocks carry risks such as operational challenges, geological uncertainty, and geopolitical exposure.

- Gold Financing and Lending: As gold collateral values rise, firms in this sector can extend larger loans, thereby strengthening balance sheets and improving profitability. The sector benefits directly from the increasing value of its core collateral.

- Jewelry and Luxury Goods: While high gold prices can dampen consumer demand, brands with strong equity and premium positioning can pass on higher costs to customers. Companies holding significant gold inventory may also benefit from appreciation in inventory value, improving financial performance.

- Electronics and Industrials: Gold remains essential in electronics, dentistry, and other industrial uses. Semiconductor and electronics firms that rely on gold may face higher input costs, but those with efficient supply chains and pricing strategies can maintain margins.

While factors such as interest rates, economic conditions, and geopolitical tensions influence gold prices, investor sentiment remains a powerful force that can often defy logic. Market psychology can shift rapidly, leading to unexpected price movements. Therefore, understanding these underlying factors is essential, but staying attuned to market sentiment is equally important to make informed investment decisions.

Evalueserve: A Trusted Partner for Sector-Level Intelligence

Evalueserve helps buy-side research teams decode the evolving dynamics of key industries, such as mining, energy, and materials, with precision and foresight. Our sector expertise, combined with advanced GenAI capabilities, enables clients to identify macro and micro trends, assess competitive positioning, and evaluate supply chain vulnerabilities across sectors where gold and other strategic resources play a critical role. We deliver tailored insights that go beyond price movements, highlighting how regulatory changes, technological innovation, and geopolitical developments are reshaping the investment landscape. With our support, you can accelerate research workflows, gain clarity on sector fundamentals, and focus on high-impact strategic decisions. In a world where gold is more than a commodity and functions as a strategic asset, we can help you understand its role within the broader sectoral context, making your portfolio more resilient and future-ready.

Talk to One of Our Experts

Get in touch today to find out about how Evalueserve can help you improve your processes, making you better, faster and more efficient.