As the world’s leading producer of natural rubber, Thailand plays an outsized role in shaping global supply and trade dynamics, supplying around 36% of global output in 2025. The industry, however, is entering a period of transition driven by three major forces: China’s expanding influence as the dominant buyer and investor, increasingly strict sustainability and traceability requirements, and stronger government initiatives aimed at modernizing production and upgrading the value chain. Together, these shifts are redefining how rubber is produced, processed, and traded, steering Thailand away from a volume-driven model and toward a more diversified, sustainable, and higher-value industry structure.

Supply Structure and Emerging Pressures

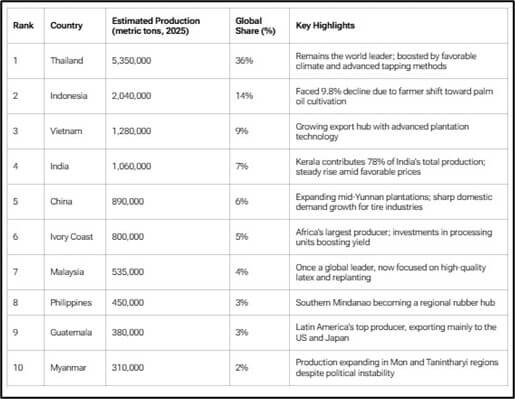

Across Southeast Asia, natural rubber production is concentrated within a few key countries, with Thailand, Indonesia, and Vietnam together accounting for about 68% of global output. Thailand sits at the heart of this supply base, supported by a large smallholder network in the southern provinces and maintaining its position as the world’s largest exporter, with 2025 shipments projected at 4.25 million tons. Yet overall supply is tightening. The Association of Natural Rubber Producing Countries (ANRPC) expects global production to rise only marginally to 14.9 million tons in 2025, while the Rubber Authority of Thailand (ROAT) forecasts a slight decline in Thailand’s own output to 4.79 million tons. The producer ranking below highlights Thailand’s 36% global share and the growing competition from emerging suppliers.

Thailand’s export profile remains weighted toward lower-value segments. Bank of Thailand (BOT) data shows that around 65% of export volume consists of intermediate processed rubber, while only 35% comes from downstream goods such as tires and medical-grade latex products. Although intermediate exports are expected to generate about USD 5.76 billion in 2023, their value remains 26% below that of downstream rubber. This reflects a structural margin gap that Thailand has yet to capture. Globally, intermediate rubber represents only a small share of total export value, whereas downstream products, particularly tires in Europe and China and gloves in Malaysia, dominate. The charts below illustrate this contrast and highlight the scale of opportunity for Thailand to expand into higher-value segments.

Several structural pressures are now accelerating the need for transformation. Rising labor costs, farmer migration into more profitable crops, and persistent price volatility are weighing on upstream competitiveness. At the same time, global buyers are tightening sustainability and traceability requirements, raising the bar for suppliers. China’s rapid expansion in downstream manufacturing, especially in tires and gloves, further shifts value creation away from raw-material exporters. These forces collectively signal a turning point for Thailand, where moving into more technology-intensive, traceable, and higher-value production is becoming essential for long-term resilience and growth.

China–Thailand Dynamics and Emerging Growth Drivers

China’s Rising Centrality in Thailand’s Rubber Market

China now anchors Thailand’s rubber demand. In the first half of 2025, Thailand shipped 1.34 million tons to China, far more than to the EU, US, or Japan, underscoring China’s position as the region’s price-setter and primary growth engine. This dependence is not new. The Ministry of Agriculture and Cooperatives previously coordinated an MoU between Thai Hua Rubber and five Chinese and Taiwanese firms for significant rubber purchases in 2013-2014. This agreement marked an early step in building China’s lasting importance as Thailand’s dominant buyer.

The relationship is now moving into a new phase. Recent discussions between RAOT and Chinese authorities include a plan to grant 0% import tariffs for Thai rubber shipped via the Mekong River. A pilot shipment of 400 tons will commence in September 2025, with capacity expected to scale above 10,000 tons per month. If fully implemented, this preferential access will significantly enhance Thai competitiveness, lower logistics costs, and deepen Thailand–China integration across the rubber supply chain.

New Opportunities in Tires, Medical Rubber, and Sustainability

China’s rapid growth in downstream rubber manufacturing is creating a new wave of opportunities for Thailand to upgrade beyond raw and semi-processed rubber. Several major Chinese tire producers now operate or continue to expand manufacturing in Thailand. These include Prinx Chengshan, which has an established tire plant in Thailand; Linglong Tire, which has expanded regional capacity; and Chengshan Tire, which has reinforced its presence through local production partnerships. Their Thailand-based operations increasingly focus on EV-compatible tire technologies that require higher-grade, more consistent natural rubber inputs. This shift positions Thailand to supply more technical and premium-spec materials, rather than only upstream commodities.

Medical rubber provides a parallel avenue for growth. The pandemic highlighted the importance of gloves, catheters, and condoms, and global healthcare demand remains robust. Thailand’s strong latex base gives it a competitive foundation, but further investment in manufacturing standards, clean-room facilities, and quality certification will be essential to capture this segment.

Sustainability requirements are also reshaping the industry. New regulations such as the EU’s Deforestation-Free Regulation (EUDR) will require importers to prove that rubber entering the EU is not linked to deforestation or illegal land use. This policy, coming into force for large companies in 2025, is expected to redefine sourcing strategies for tire manufacturers and other downstream buyers. Thailand has responded by introducing the Thailand’s Rubber Trade (TRT) blockchain platform. Built on blockchain technology, TRT is designed to trace rubber from plantation to port, giving buyers verifiable data to comply with emerging sustainability requirements. This system not only supports EU market access but also builds confidence among global partners who are under pressure to demonstrate responsible sourcing.

Taken together, China’s industrial pull, rising demand for higher-grade rubber products, and tightening global sustainability standards are opening clear pathways for Thailand to shift from an upstream-dominated model toward more technology-driven and higher-value growth.

Policy and Industry Support Framework

Thailand’s policy environment is increasingly geared toward stabilizing supply and improving long-term sector competitiveness. The Rubber Authority of Thailand (RAOT) is advancing replanting programs, price-stabilization measures, seasonal tapping management, and credit support to reduce income volatility for smallholders. A recent example is the 2025 replanting initiative, where RAOT allocated USD 86.66 million to assist farmers who cut and replant aging rubber trees using their own funds. The program aims to lower replanting costs and help farmers renew low-yield plantations.

Industrial upgrading is being supported through monetary and investment policy. The Bank of Thailand (BOT) emphasizes diversification into higher-value downstream production, while the Board of Investment (BOI) offers incentives for technology-intensive and eco-friendly rubber processing, especially in EV materials and medical-grade latex goods. These measures aim to attract advanced manufacturing and shift Thailand beyond a commodity-heavy export model.

Thailand also collaborates with Indonesia and Malaysia through the International Tripartite Rubber Council (ITRC) to coordinate supply management and respond to global price volatility.

Strategic Implications and Outlook

Thailand’s sector transition creates clear openings for global players. Chinese manufacturers gain a reliable raw-material base and an expanding platform for tire, glove, and technical rubber production. International buyers benefit from Thailand’s growing emphasis on traceability and sustainability, which helps meet tightening ESG rules such as the EU’s deforestation-free regulation. For Thai companies, deeper collaboration with foreign investors provides access to technology, premium markets, and upgraded production standards, especially as systems like TRT strengthen verified sourcing.

Looking ahead, Thailand will remain the anchor of global natural rubber supply, but long-term competitiveness hinges on shifting from a commodity-driven model to a more sustainable, value-added hub. With China as a core partner in demand, investment, and advanced manufacturing, Thailand is well positioned to supply growth in electric mobility, healthcare, and green materials. The next phase of competitiveness will depend on timely action: investment in downstream capacity, sustainable sourcing, technological upgrading, and closer industry collaboration to secure Thailand’s role in an increasingly ESG-driven global supply chain.

Talk to One of Our Experts

Get in touch today to find out about how Evalueserve can help you improve your processes, making you better, faster and more efficient.