The World Health Organization changed the status of the novel coronavirus from epidemic to pandemic on March 11, 2020, signaling all governments to get their healthcare systems ready for a challenge. While healthcare providers across the globe are trying to get as many hands-on deck as possible to fight the virus, COVID-19 has shaken the very foundation of the global economy. According to the International Monetary Fund, the recession triggered by the pandemic will likely be “way worse” than the 2008–09 global financial crisis.

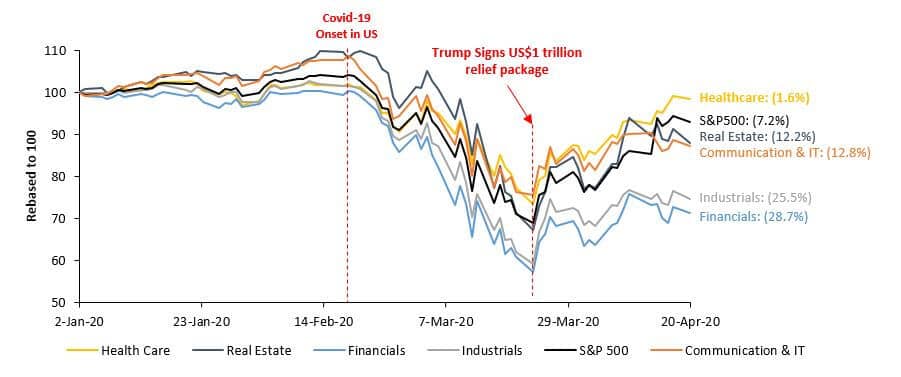

Along with all other business segments, the pandemic is also testing the resilience of the healthcare industry, which has been receiving strong investor support due to robust demand for healthcare. Moreover, the industry is less susceptible to economic shocks, owing to its “defensive” nature, and has outperformed the broader market (refer to US S&P Dow Jones Indices graph below).

US Market Performance (YTD)

Source: S&P Dow Jones US market Indices; Covid-19 onset in the US started from 20-Feb-20

On the flip side, the social and political chaos, volatility in financial markets, and uncertainty in the global economy have been weighing on merger & acquisition (M&A) activities across industries, including healthcare. Following the outbreak, M&A activities have slowed down noticeably in the industry. The difficult funding environment is leading to the postponement of deals, especially those that require financial support.

Global Healthcare M&A (YTD)

Source:Visit https://www.refinitiv.com/en/products/deals-intelligence deals as of 09-Apr-20; YTD 2019 figures represent approximate values

Source:Visit https://www.refinitiv.com/en/products/deals-intelligence deals as of 09-Apr-20; YTD 2019 figures represent approximate values

M&A Transactions at Risk

The latest casualty in the healthcare M&A space is Novartis’ generics brand – potential buyer Aurobindo Pharma scrapped the USD900m buyout plan announced in September 2018. The plan was terminated based on mutual agreement, as the involved parties could not obtain approval from the US Federal Trade Commission (FTC) within the expected timelines, and the deal value was no longer realistic in the current scenario. The only silver lining in this case was that there was no break-up fee involved, which sometimes are quite significant.

Other pending “big ticket” deals in the industry include Abbvie’s USD63bn buyout of Allergan, Mylan’s merger with Pfizer’s Upjohn, and Stryker’s USD5.4bn bid for Wright Medical. Let’s see where these deals stand at this moment:

- The closure of the Abbvie-Allergan deal is primarily reliant on the completion of paperwork (which would have been a mere formality had it not been for the global lockdown).

- The Stryker-Wright Medical deal is indefinite now, due to uncertainties related to FTC approval and topline.

- The closure of the Mylan-Upjohn deal has been delayed because the crucial EGM was postponed until June 2020 due to the current lockdown situation.

Key Pending Healthcare M&As

Source: Evaluate Pharma and Company filings as of 13-Apr-20

On the other hand, deals signed during the COVID-19 pandemic, such as Hypera Pharma’s acquisition of Takeda’s brands and Thermo Fisher’s takeover of Qiagen, might not necessarily be at risk, as the involved companies would have considered counter measures to mitigate any risks. Although one cannot be certain if the involved parties have comprehended the associated risks, it is highly likely that the pandemic will delay deal-related activities. If that happens, target valuations could change vis-à-vis the time when the deal was initiated.

Overcoming Short-term M&A Challenges

Let’s look at some of the key risks that buyers and sellers could potentially face in the current environment, and assess how these can be mitigated:

- Delay in regulatory clearance: The current lockdown will without doubt result in regulatory clearance/approval-related delays. This challenge can be mitigated by both parties by accelerating timelines related to due diligence, transaction evaluation, etc., so that the process can be completed as soon as the situation normalizes.

- Changes of pre-COVID valuation: Because of the impact of the pandemic on companies, both buyers and sellers may reject the previous deal value and quantify the impact of the pandemic. To handle this challenge, companies can consider financial statements after discounting the quantifiable impact of COVID-19; this may lead to a revision of the purchase price at closing.

- Nullification of pre-COVID due diligence: If a deal is postponed, the involved parties may demand another round of thorough due diligence to make provisions for new disclosures that may have a material impact on the deal. In case of such a demand from any of the involved parties, it would be in the best interest of both to arrive at a strategic agreement on how the transaction should proceed. They should plan out any new arrangements.

- Delayed third-party approval: Due to lockdowns, buyers’ due diligence activities will likely be delayed. Routine activities, such as on-site visits, audits and inspections, may also become unmanageable. Sellers can try to handle this challenge and offset delays, to a certain extent, by extending the deadlines and creating provisions for these delays.

Is there Light at the End of the Tunnel?

Although the current M&A scenario seems extremely gloomy, we believe there is light at the end of the tunnel. Many governments and their respective central banks are offering financial relief packages to “cushion” the impact of COVID-19. Such measures could ensure liquidity in financial markets. We also see the following factors positively affecting M&A activity in the industry:

- Extremely attractive valuations are making a strong case for multiple buy-out discussion. We foresee significant buy-out activities in the hospital segment, considering the relevance of hospitals in the COVID-19 scenario. In addition, innovation-focused biotech stocks and large pharma companies working to find a cure for the virus will also experience a surge in valuation.

- Estimated high buying capacity of USD2.0tr among private equity firms. Their capital position provides these firms with plenty of firepower to assess and capture resilient assets in the near term. In 2019, the value of private equity M&A deals in the healthcare industry stood at a record USD78.9bn in disclosed value (as per Bain Capital).

- High probability of increase in stock deals due to the difficult funding environment. Considering the healthcare industry has seen significant market correction in the last few months, equity deals may turn out to be the solution of the hour, given the already stretched balance sheets.

In the long term, the COVID-19 pandemic may actually act as a catalyst for future M&A activities in the healthcare industry. Although M&As are expected to be relatively low during Q2’20–Q3’20, the industry’s attractive valuation, robust demand with relatively minimal supply disruptions, and the opening up of bond markets may accelerate deal activity towards the end of this calendar year.

Amid this new normal, both buyers and sellers, as well as third parties, have to adapt quickly to the changing environment to re-focus on their long-term growth strategy.