Global Healthcare Market – 2021

It’s been over 16 months since the start of the pandemic, and we are still fighting against the deadly coronavirus. Economic recovery across regions has been diverse due to differences in the pace of vaccine rollouts and policy support. The consistent and equitable implementation of tools to control the pandemic continues to be a challenge for governments across the globe. Mass vaccination drives in advanced economies are instilling positive market sentiments with the presumption of stability. However, the emergence of a Delta variant of COVID-19 in Europe, the US, and China is fueling the need for ‘booster shots’ to sustain global recovery.

According to the IMF, the global economy is likely to grow by 5.9% in 2021 and 4.9% in 2022 driven by a stronger recovery in the advanced economies where additional fiscal stimulus and a broader vaccination strategy has higher visibility. Nonetheless, “the fault lines opened up by COVID-19 are looking more persistent” with every pocket of resurgence leaving minimal headroom for policy support.

The resiliency of the healthcare industry has been on display throughout the pandemic with investors continuing to view the sector in terms of its historical position as a ‘go-to’ market, given its proven ability to be structurally stable and offer impressive prospects across the economic cycle.

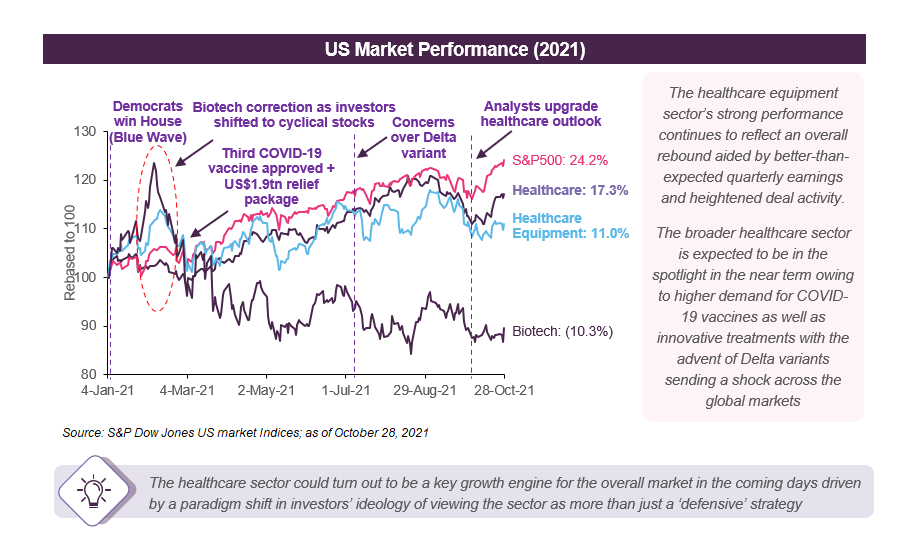

Within the healthcare industry, healthcare equipment continues to outperform (refer to the graph below) driven by the urgent need for innovative care delivery in new or alternative settings and expedited recovery of demand especially for elective procedures. On the other hand, Biotech heavily underperformed post Q1’21 primarily due to the shifting of focus towards cyclicals and negative sentiments arising as of result of greater regulatory clampdown on transformative deals and drug pricing.

Some of the sub-sectors within the healthcare industry continue to receive windfall gains driven by COVID-19. The prolonged period of uncertainties and the release of positive efficacy data supporting the recent launches of vaccines have helped in sustaining the investors’ demand. However, the current recovery continues to be volatile as the global economy is in the midst of a fourth wave and the spread of resistant mutations.

Global Healthcare M&A: Unprecedented Fightback 2.0

The unprecedented surge of deals witnessed globally during the second half of last year gained further momentum in 2021 as dealmakers strived to stay ahead of the deal curve. A y-o-y comparison shows a record growth aided by a muted H1’20 during which investors were forced to hold off on deal-making because of the onset of COVID-19.

The pandemic induced impediments which had initially shifted the M&A timelines, has since witnessed a robust global recovery driven by the announcements and closures of several ‘big ticket’ deals, especially in the US and EMEA. The ability to identify, negotiate and realize value from increasingly complex partnerships and alternative collaboration models has become an important competitive advantage. The following trends have resulted in an overall improvement in M&A sentiments in the industry vs 2020:

- Unprecedented levels of alliances in the R&D ecosystem as several major biopharma companies collaborated to effectively leverage their resources to stem innovation

- Sponsor deals rebounded exceptionally. Several deals, which were under discussion, were re-initiated and provided well-timed opportunities for investment banks

- Independent hospitals and smaller systems have started to explore partnerships to ensure uninterrupted services

- Healthcare service providers focusing on a consumer drive health operating model

- MedTech’s urgent focus on real-time data

- Rapid paradigm shift towards utilizing data and actionable insights to implement person-centric network strategies.

A deep dive into the key sub-sectors reveal just how broad-based the deal activity has been. The healthcare services and equipment markets continued their strong recovery, as patients started to move back to traditional healthcare settings. Tele-medicine has been an M&A hotspot, as COVID-19 has catalyzed the rapid regulatory and reimbursement shifts favoring the sector. Pharma and biotech continued their blockbuster momentum, as they generated more evidence on ‘efficacy’ and rolled out their authorized vaccines in a phased manner.

Source: Refinitiv as of September 30, 2021; M&A Heat Index is based on the equal weightage of average deal size and number of deals during each quarter; bubbles represent overall deal activity in USD billion during the respective quarter

Healthcare Funding – Normalization of ‘Cash Runways’

The financial markets witnessed a record surge in activities in the equity and debt capital markets (ECM and DCM) wherein borrowers continued to seek opportunities to refinance and extend debt maturities in the present low-interest-rate environment thereby building ‘fortress balance sheets’. Lenders, on the other hand, have focused on generating higher yields, with refinancing emerging as the major avenue for the deployment of their ‘eager’ capital. Though DCM expectedly witnessed a slowdown in 2021 post a record-breaking run last year, the Syndicated Loans market has turned into a hotspot with record levels of issuances. The recent scrutiny of SPAC IPOs has resulted in a ‘cool-off’ period in the otherwise red-hot ECM this year. The revival of traditional IPOs and a favorable secondary market has sustained the investors’ demand which however, we expect to normalize at current level of ‘cash runways’.

Global Healthcare Capital Markets Activity

- In the ECM, biopharma and digital health companies continued to lead the way with record levels of IPOs and follow-on deals. However, the market is in a ‘cool-off’ period owing to a slowdown in SPAC IPOs

- DCM issuances declined post a rapid surge in 2020 as corporates had pre-funded their capital requirements

- Rapid surge in Syndicated Loans market was primarily driven by faster economic recovery, low interest rates, repricing, strong investor demand and refinancing

The impetus from the capital markets over the course of the past year had resulted in major healthcare providers undertaking multiple financing rounds and accumulating plenty of dry powder. They are currently ‘shopping’ for potential targets and aiming to close out deals in order to enhance their portfolios and expand market share, despite the ongoing uncertainties surrounding COVID-19, economic recovery and the ever-changing political landscape.

There is growing evidence (below chart) which indicate that majority of the key consolidators have already started to deploy their dry powder post identification of key assets in 2021. While others, who still have some headroom relating to their leverage positions, have continued to shore up their balance sheets at a steady pace with the likely presumption of potential M&As. However, given the recent slowdown in financing it seems that these consolidators have reached peaked cash runaways and are just few steps away from deploying their reserves further.

Source: Company filings, FactSet as of September 30, 2021; figures represent changes in cash position since December 31, 2020, in USD; AstraZeneca’s cash build includes amount raised for Alexion’s acquisition which was completed on July 21, 2021 (yet to come out with Q3’21 results)

Healthcare SPACs: Spotlight on Rising Redemptions

The heightened regulatory scrutiny has to a certain extent ‘put the brakes’ on Special Purpose Acquisition Companies (SPACs) activity from Q2’21 onwards post a record surge from last year till Q1’21. In April, the Securities Exchange Commission (SEC) in the US had announced that they were coming up with a set of new guidance relating to the issuance of warrants to the investors. This along with concerns around transparency and disclosures, mixed post-deal performance, rising redemptions during De-SPAC and potential overcrowding has resulted in growing investors’ doubts about SPACs’ ability to deliver high-quality companies. However, the Healthcare sector has been the second most active for De-SPAC deals in 2021. According to the NYSE, last year there were 50 SPACs that went public with Healthcare being their target sector. This positioned 2021 as a potential blockbuster year for SPAC M&A.

Healthcare SPAC M&A Activity: Merger Clock Continues to Tick Louder

According to Evercore, there are currently around 60 SPACs that are actively screening for target companies across the healthcare and life sciences industries. Hence, it is expected that more healthcare startups might choose to go public through this exit pathway throughout 2021. Though it might be too early to differentiate SPACs based on market returns, the following factors continues to shape the market demand and supply in 2021.

Key Growth Drivers:

- Faster access to the market: in weeks or a few months vs the 12-18 months for an IPO

- Certainty of knowing the valuation and pricing resulting better negotiations and deal structuring

- Opportunity to put forward a more complicated equity story aided by the ability to use projections especially in the case for high-growth healthcare companies

- Larger pool of investors and higher liquidity than in traditional private equity investments

Key Market Restraints:

- Overcrowding has resulted in lack of attractive private healthcare companies

- High uncertainty about the business being acquired given shrinking valuations post De-SPAC

- Reduction in market volatility has taken the shine off SPACs’ attractiveness vs traditional IPOs

- Poor performance and heightened regulatory scrutiny have forced investors to tread cautiously

Outlook 2021: Focus on Resilience and Transformation

With the spotlight been on enhancing scale and resilience of business portfolios, companies and investment firms have rushed to get ahead of the potential changes in healthcare delivery. Even though valuations remain sky-high and a sellers’ market endures, demand for quality assets and sellers’ willingness to sell them are accelerating deals. Buyers are also re-assessing where they fit in the value chain and whether M&A would be the right step forward. In the light of these developments, we foresee the following key M&A trends to define the overall deal-making for the remainder of 2021:

- Innovation continues to be rewarded: We continue to foresee any incremental M&A push to be broad-based across major healthcare sub-sectors, as innovation gets rewarded by investors. These include companies that are directly involved in addressing the spread of COVID-19, like those focused on diagnostics and vaccine development, as well as consolidation among medical devices manufacturers, which were severely impacted by restrictions on elective procedures last year.

- Estimated dry powder of ~USD2.0tr among private equity firms: The strong capital position of private equity firms continues to create opportunities for them to assess and capture resilient healthcare assets. In H1’21, the disclosed value of private equity M&A deals in the healthcare industry stood at a record c.USD56bn, up 51% y-o-y (as per Refinitiv).

- Alternative avenues of deal-making continue to be on the rise: Minority stakes, joint ventures, strategic alliances, and mergers with SPACs are expected to continue to gain traction in 2022 amid prolonged market recovery.

- Vaccine developers set to gain market share: Successful vaccine developers are expected to earn a windfall of excess cash and market positioning given enormous demand for their products. These companies will be able to reshape the competitive landscape of the pharmaceutical industry. Additionally, the companies which have utilized the new mRNA technology to develop their vaccines will have earned an important first-mover advantage in the innovation process of applying mRNA to other therapeutic areas.

- Environmental, Social and Governance (ESG) factors set to take center stage: The COVID-19 pandemic has shown that ESG is key to crisis-resilient long-term value creation. Companies with dynamic business cultures were more resilient during the shutdowns given their ability to absorb the ‘shock’. As a result, deal makers are expected to continue to place greater emphasis on ESG criteria while screening out assets and determining valuations.

- Scarcity of attractive assets may serve as a ‘deal-breaker’: The unprecedented surge in deals in the last three quarters backed by a ‘liquidity flush’ may result in an overheated market in Q4’21 while heading into 2022. Investment banks might find it tougher to negotiate terms between the parties due to a lack of available white space.

- Greater scrutiny on biopharma M&As going forward: Governments and antitrust enforcers across the globe are teaming up to rethink their approach toward pharmaceutical merger review. This is expected to curb transactions that are responsible for raising prices or dampening innovation in the sector.

- Heightened shareholder activism: While activist investors played the waiting game for much of 2020, they have remained active behind the scenes by utilizing their time to raise funds and prepare for a busy 2021. As the dust starts to settle, activist investors are in a strong position to identify and target companies ripe for activist involvement.

We continue to expect cross-sector deals to become more prominent as existing players and new entrants alike push for ecosystem strength throughout the healthcare value chain. Prime focus will be to remain agile and push for innovative business models and optimization of corporate portfolios.

Global dealmakers are still not out of the woods, with the advent of a fourth wave of COVID-19 cases across Europe and China, increasing foreign direct investment (FDI) restrictions imposed by governments globally, uncertainties around the economic policies in the US, and the ongoing Brexit negotiations.

However, considering the importance of the healthcare industry’s role in the current pandemic, we continue to foresee many new companies (such as Infrastructure Funds, FMCG and large technology companies) entering this space to diversify their business portfolio. These companies armed with marketing expertise, global footprint and strong balance sheets could change the healthcare sector’s landscape in the days to come.

If this year is anything to go by then we are amid one of the most robust and broad-based M&A markets witnessed in the last few decades. Hence, we continue to believe that the digitalization, robust demand supported by supply chain normalization, and the M&A firepower of strategies, sponsors and SPACs will help in sustaining the recent acceleration in M&A activity for the remainder of 2021 heading into the new year.