July 14, 2025

Prologue

Reflecting on the late 1990s and early 2000s evokes a deep sense of nostalgia – especially for millennials, the generation that came of age during that transformative era. Now entering midlife, they have witnessed the rise of cable television, the dawn of the internet age, the trauma of 9/11 and the war on terror, and the financial upheaval of 2008 – all shaping their worldview. It’s no wonder that when Britney Spears – an icon of their youth –revealed her struggles under a court-imposed conservatorship[1] in a podcast titled, Britney's Gram, in 2020, the response was swift and passionate. Many of her fans, now in their late 30s and early 40s, rallied behind her, amplifying a movement that had simmered since 2008. Their advocacy helped drive a historic legal turnaround, culminating in the termination of her conservatorship in November 2021[2] – finally giving the pop star full control over her life and finances.

A similar (if not identical) movement is quietly gaining traction on Wall Street, energized further since the second Trump administration took office earlier this year, with a clear focus on reducing government ownership. Fannie Mae and Freddie Mac – cornerstones of the U.S. housing market – currently support around 70%[3] of all mortgages nationwide. Following the 2008 Financial Crisis, both entities were placed under federal conservatorship, with oversight transferred to the Federal Housing Finance Agency (FHFA). Now, 17 years later, calls for ending that conservatorship are growing louder among policymakers and financial insiders alike. Leading the charge is billionaire hedge fund manager Bill Ackman, one of the most vocal proponents of returning the GSEs (Government-Sponsored Enterprises) to private hands.

Oops! … Bill Tweets It Again

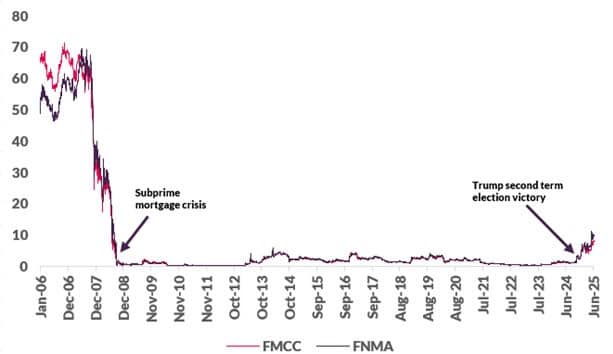

The push to privatize Fannie Mae and Freddie Mac isn’t new – it was initially proposed during the first Trump administration, but ultimately stalled due to limited congressional support and the onset of the COVID-19 pandemic. Investors who acquired GSE shares in the aftermath of the 2008 Financial Crisis, when their value had virtually plunged to zero (see figure 1), now stand to benefit substantially from a potential reprivatization. Among them is Bill Ackman, CEO of Pershing Square Capital Management, whose holdings in the two firms are estimated at roughly 210 million common shares[4] – which may yield up to $1 billion[5] if plans to privatize both firms go through. Since the revival of these efforts under the second Trump administration, stock prices have surged dramatically, with Fannie Mae rising nearly 600% year-over-year and Freddie Mac climbing approximately 700% as of the June 24 market close (as shown in figure 1).

In a 2017 interview[6] , Ackman highlighted the potential benefits of ending Fannie Mae and Freddie Mac’s conservatorship, noting that the necessary conditions for resolving their status were already in place. He renewed his advocacy in a December 2024 tweet[7] , outlining a credible two-year path toward privatization. The following January, Ackman published a comprehensive proposal titled, The Art of the Deal, projecting that future Initial public offerings (IPOs) of both entities could generate roughly $300 billion for the government. His plan recommended reducing the capital requirement to 2.5% and forgiving a portion of the Treasury’s preferred equity stake, which he argued would raise the GSEs’ stock prices to around $30 per share – without exerting upward pressure on mortgage rates.

Description: Fannie Mae/Freddie Mac share prices had virtually plunged to zero post the 2008 subprime mortgage crisis. Post Trump’s election victory in November 2024, share prices of Fannie Mae and Freddie Mac have exploded, with Fannie Mae seeing a roughly 600% surge in the last year and Freddie Mac’s stock price having risen by nearly 700% during this period. Source: Yahoo! finance.

Till the Sweep Ends

Home loans in the US are generally backed by five principal authorities – the United States Department of Veterans Affairs, the Federal Housing Finance Agency, and the Federal Housing Administration, alongside Fannie Mae and Freddie Mac. Fannie and Freddie operate by purchasing loans from lenders and bundling them into Mortgage-Backed Securities (MBS), which are then sold to investors – effectively influencing national mortgage rates. Following the 2008 subprime crisis, both GSEs recorded combined losses of $109 billion[8] that year due to exposure to high-risk loans. In response, the U.S. Treasury extended two $100 billion credit lines under the Preferred Stock Purchase Agreement (PSPA). By 2011, total losses surged to $266 billion, with the bulk attributed to subprime mortgages originated during 2006–2007.

In 2012, the U.S. Treasury implemented a net worth sweep[9] of Fannie Mae and Freddie Mac's profits, aiming to recoup the full amount pledged in financial support. This mechanism effectively barred GSE shareholders from retaining future earnings. By 2019, the Treasury had collected over $190 billion[10] in senior preferred shares – carrying a 10% dividend rate – along with warrants covering 79.9% of the GSEs’ common stock under the PSPA. These senior shares ultimately generated more than $300 billion[11] in dividends, leading the FHFA to end the sweep in September 2019.[12] This decision enabled Fannie and Freddie to retain future profits and begin rebuilding their capital positions.

As of December 2024, the Treasury’s senior preferred stake in the GSEs totaled $341 billion[13] , while the combined net worth of Fannie Mae and Freddie Mac climbed to $160.3 billion by the first quarter of 2025 (see figure 2) – providing renewed momentum for the Trump administration’s efforts to end the companies’ federal conservatorship.

Description: Fannie Mae’s net worth increased to $98.3bn in Q1 2025*, while Freddie Mac’s total shareholders’ equity rose to $62bn during this period, propelling the combined net worth of both mortgage giants to $160.3bn. Source: Fannie Mae and Freddie Mac

Stronger than yesterday: regulatory shortfall at its lowest

Under the Enterprise Regulatory Capital Framework (ERCF)[14] , Fannie Mae and Freddie Mac are required to maintain a Tier 1 capital ratio of 2.5% of their total adjusted assets as part of their leverage capital obligation. As of Q1 2025, the capital requirement stands at $187 billion for Fannie Mae and $147 billion for Freddie Mac, resulting in a combined target of $334 billion. This is offset by a combined net worth of $160.3 billion, bringing the regulatory capital shortfall down to $173.7 billion – the lowest level recorded since mandated disclosures began in 2021 (see figure 3). According to Sajjad Hussain, Managing Director of Global Fixed Income, Currency & Commodities (GFICC) at J.P. Morgan, bridging this shortfall organically would take approximately seven years, assuming annual earnings of $25 billion across both enterprises.[15]

Description: GSEs total regulatory capital shortfall as of Q1 2025 (shown as diagonal stripes on secondary Y-axis) has fallen to $173.7bn due to a progressive increase in their net worth, which increased to $160.3bn during that period. Capital shortfall is the difference between the combined capital requirement of the GSEs (shown as a stacked bar chart on the primary Y-axis) and their combined net worth (shown as the shaded area on the secondary Y-axis). Source: Fannie Mae and Freddie Mac

Pershing Square’s privatization plan – GSEs comeback hit?

In January, Pershing Square released a proposal to privatize Fannie Mae and Freddie Mac without requiring congressional approval. The plan recommends setting the GSEs’ regulatory Tier 1 capital requirement at 2.5% – as suggested under the ERCF framework – which is significantly lower than their current 4.5% level. It assumes that the Treasury’s $341 billion preferred equity stake has been substantially offset by $301 billion in dividend payments tied to approximately $191 billion in quarterly draws since 2008, yielding an internal rate of return (IRR) of 11.6% (see figure 4). That outcome exceeds the original 10% dividend structure by roughly $25 billion. However, Pershing Square CEO Bill Ackman noted that the federal government, which owns around 80% of the GSEs, would need to write off approximately 20% of its remaining preferred equity to facilitate the companies’ transition to private ownership.

The plan preserves the existing PSPA, ensuring uninterrupted government credit guarantees to the GSEs in exchange for a 25bp commitment fee to the Treasury. As part of cleanup of the existing capital structure, the Treasury would retain warrants of 79.9% of common stocks, preserving upside for taxpayers, while junior preferred shares would either remain outstanding or be converted to common stock on a negotiated basis. Finally, the plan would pave the way for both firms to go public – Fannie Mae by end-2026, which would raise about $5bn through an IPO, followed by Freddie Mac by end-2027, which would raise about $15 billion in new common equity. Ackman claims that both stocks could rally to $30/share without putting upward pressure on mortgage rates, a sharp rise from their current $8-$9 range.

Description: The Treasury’s $341bn preferred share position in GSEs has been paid off with an 11.6% IRR, thanks to $301bn in combined dividend payments accrued on $191bn in quarterly draws since the two firms were placed under conservatorship in 2008. Under the original 10% dividend rate, the Treasury would have recouped ~$25bn less than what it has actually recovered. Source: Pershing Square and FHFA

…Baby One More Recap

The Congressional Budget Office (CBO) has examined three administrative paths for recapitalizing Fannie Mae and Freddie Mac, centered on allowing the GSEs to retain earnings over three- or five-year periods before issuing common stock to investors. Capital requirement targets range from 3%-to-4.5%-to-6%, with key redemption objectives that include repaying $191 billion in Treasury-held preferred shares, redeeming $35 billion in junior preferred stock, and delivering value for the Treasury’s outstanding warrants.

Equity issuance in 2027 (three-year earnings retention): Under a baseline scenario with a 3% capital requirement (CR) and an 8% return on capital (ROC) and earnings growth, the GSEs would need a total capital buffer of $247 billion by end-2026. That figure stands substantially below the $370 billion and $494 billion required under 4.5% and 6% capital requirements, respectively. After three years of retained earnings, the GSEs are projected to build $208 billion in capital, resulting in a regulatory shortfall of just $39 billion under scenario 1. By contrast, shortfalls under the 4.5% and 6% frameworks would reach $162 billion and $286 billion, respectively (see figure 5). A more modest capital requirement not only streamlines the recapitalization process, but it also enhances valuation – Scenario 1 forecasts a combined equity value of $521 billion. This would fully offset the Treasury’s $191 billion in senior preferred shares and $35 billion in junior preferred stock while generating approximately $206 billion in value from outstanding warrants.

Under Scenario 2, assuming a 10% return on capital, the GSEs' combined equity would reach $368 billion – sufficient to eliminate the regulatory shortfall and repay junior preferred shareholders. However, covering the Treasury’s senior preferred stake would require exercising common stock warrants. Scenario 3, which includes a 12% ROC but negligible earnings growth, yields a lower equity value of $292 billion. While this amount would bridge the regulatory capital gap, it would fall short of fully satisfying obligations to both junior preferred shareholders and the Treasury’s remaining preferred position.

Equity issuance in 2029 (Five-year earnings retention): Under the baseline scenario – which assumes a 3% capital requirement alongside 8% ROC and earnings growth – the GSEs would need a total capital buffer of $267 billion by end-2028. This figure is notably lower than the $400 billion and $534 billion required under the respective 4.5% and 6% capital requirement scenarios. By retaining earnings over five years, the GSEs are projected to accumulate $273 billion in capital, resulting in regulatory shortfalls of $127 billion in Scenario 2 and $260 billion in Scenario 3 (as shown in figure 5).

Scenario 1 also projects a combined equity valuation of $563 billion – sufficient to repay the Treasury’s $191 billion senior preferred stake and generate $271 billion through warrant execution. Under Scenario 2, which assumes a 10% ROC, the estimated equity value of $398 billion would be enough to eliminate the capital shortfall, cover both the Treasury’s preferred shares and junior preferred obligations and yield $37 billion via warrant conversion. In contrast, Scenario 3 – with a 12% ROC and nil earnings growth – produces a lower equity value of $316 billion, which would address the regulatory shortfall and repay junior preferred shares but fall short of fully redeeming Treasury’s remaining preferred interest.

Description: The CBO has analyzed three scenarios with potential common-stock offerings in 2027 or 2029. The plan assumes that Fannie Mae and Freddie Mac may keep 100% of their earnings for a period of three years or five years. After this period, each GSE would issue common stock to investors, and proceeds from these offerings would be utilized to buy back the Treasury’s senior and junior preferred shares. Source: Congressional Budget Office (CBO)

Epilogue

Despite her conservatorship being transferred to her father, Jamie Spears, after a highly publicized emotional breakdown following her divorce from Kevin Federline, Britney Spears continued to thrive creatively. She released four successful albums – Circus, Femme Fatale, Britney Jean, and Glory – and made notable television appearances, including serving as a judge on The X Factor USA. Her ability to tour globally, perform at major venues, and maintain professional momentum during the conservatorship underscored her capability to manage her own finances, make independent life decisions, and responsibly raise her teenage sons. Her continued success helped spark a powerful online movement, with numerous celebrities[16] – such as Christina Aguilera, Mariah Carey, and Justin Timberlake – voicing support for ending the conservatorship. Their advocacy played a vital role in amplifying public awareness and exerting pressure for its termination, which ultimately came in November 2021. Upon regaining her autonomy, Britney expressed heartfelt gratitude to her fans for their unwavering campaign to #Free Britney[17].

Since incurring multi-billion-dollar losses during the 2008 Financial Crisis, the GSEs have also made notable strides in rebuilding their financial standings. By Q1 2025, their combined net worth had climbed to $160.3 billion, accompanied by sharp gains in their stock prices – bolstering calls for their return to private ownership. Influential investors,[18] such as Bill Ackman, John Paulson, and Carl Icahn, have publicly championed the privatization of Fannie Mae and Freddie Mac, arguing that the companies have repaid their government bailout and should be released from conservatorship. A central element of Ackman’s privatization and recapitalization proposal involves writing down a portion of the Treasury’s $341 billion in preferred shares. The Congressional Budget Office’s evaluation of three recapitalization scenarios also indicates the same – even under the most favorable conditions, fully repaying the Treasury’s preferred equity stake may prove unfeasible. As a result, a partial write-down of the Treasury’s interest could be required – an outcome that, in our view, would likely face significant political resistance and undermine prospects for bipartisan support.

A secondary – but still noteworthy – challenge highlighted in the CBO’s recapitalization scenarios is the regulatory capital shortfall, currently estimated at $173.7 billion. Assuming that the GSEs generate $25 billion annually in combined earnings, it would take nearly seven years to organically build the required capital buffer. While a future IPO could provide additional proceeds to close the gap, potential logistical complexities and legislative roadblocks may pose hurdles to execution. Another critical consideration is Implicit Guarantee Status, which enables the GSEs to access the remaining $256 billion from the original $446 billion Treasury backstop – $190 billion of which has already been utilized. Although the Trump administration previously affirmed that such guarantees would remain[19] in place following privatization, terminating the conservatorship could jeopardize this advantage and introduce uncertainty with regard to continued federal support.

The 30-year fixed mortgage rate surpassed 7% in January and remains elevated at approximately 6.67% as of July 3[20] , contributing to increased borrowing costs. Currently, mortgage loans are effectively backed by the U.S. government, as both Fannie Mae and Freddie Mac remain under federal oversight, which provides strong assurance to investors that loans purchased from lenders will be repaid, given the implicit guarantee of government support. Returning the GSEs to private ownership is likely to be welcomed by long-term investors who have remained committed for the past seventeen years, anticipating that their patience would eventually yield strong returns. After all, the financial conservatorship was intended as a temporary intervention. During this period, the stock prices of both firms remained depressed, as the conservatorship prioritized stabilizing the mortgage market and maintaining housing affordability over enhancing shareholder value. Privatization would likely lead to a surge in stock prices; however, it could also increase the firms’ appetite for risk—potentially leading to upward pressure on mortgage rates over time and exacerbating the housing affordability crisis – a matter of significant political sensitivity. Should rates continue rising, many prospective homebuyers may shift toward Federal Housing Administration (FHA) loans, which could diminish the role of Fannie Mae and Freddie Mac as the primary mortgage guarantors in the U.S. market.

Footnotes

[1] Conservatorship of Britney Jean Spears v. Britney J Spears, 2:08-cv-01021 (CourtListener.com)

[2] Judge Ends Conservatorship Overseeing Britney Spears’s Life and Finances (The New York Times)

[3] About Fannie Mae & Freddie Mac (GSEs) (National Association of Realtors)

[4] No Congress, no rate hikes: Bill Ackman’s plan to privatize the GSEs (Housingwire)

[5] Ackman Could See $1 Billion Gain on Fannie Mae, Freddie Mac Investments (Barron’s)

[6] Watch the full interview (Yahoo! finance)

[7] Ackman says Fannie Mae, Freddie Mac ‘particularly interesting today’ (Nasdaq)

[8] The Fannie and Freddie Bailout Continues: Do They Now Need $800 Billion? (Manhattan Institute)

[9] Treasury Department Announces Further Steps to Expedite Wind Down of Fannie Mae and Freddie Mac (US Treasury Department)

[10] Quarterly Draws on Treasury Commitments to Fannie Mae and Freddie Mac per the Senior Preferred Stock Purchase Agreements (FHFA)

[11] Dividends on Enterprise Draws from Treasury (FHFA)

[12] Trump administration working to end Fannie/Freddie profit sweep in September (Housingwire)

[13] Recapitalizing the GSEs through Administrative Action (Urban Institute)

[14] Enterprise Regulatory Capital Framework – Public Disclosures for the Standardized Approach (FHFA)

[15] GSE Reform Resurfaces: Challenges and Implications (J.P. Morgan)

[16] ‘We love you’: Celebrities rally around Britney Spears after her call to end conservatorship (NBC News

[17] Britney Spears Thanks The #FreeBritney Movement For Saving Her Life (Vogue)

[18] Hedge funds could make billions from a Fannie Mae and Freddie Mac spin-off (Yahoo! Finance)

[19] Trump pledges government will continue Fannie Mae, Freddie Mac guarantees (Axios)

[20] Heading into the Holiday Weekend, Mortgage Rates Decrease (Freddie Mac)

Talk to One of Our Experts

Get in touch today to find out about how Evalueserve can help you improve your processes, making you better, faster and more efficient.