Q1’25 highlights

M&A volume rises despite deal count dropping to 10-year low

In Q1’25, the number of announced M&A deals declined by 15% YoY to 11,069 globally, compared with 13,062 in Q1’24. However, the total deal value rose by 15% to USD885 billion, making Q1’25 the strongest opening quarter for dealmaking since 2022. Regionally, M&A activity in the US decreased by 14% YoY, with the country accounting for 43% of global deal volume – its lowest share since Q1’20. Conversely, Q1’25 was the most robust first quarter in the past three years for both Europe and APAC, which recorded YoY increases of 12% and 59% in overall activity, respectively. High interest rates, geopolitical tensions, and economic uncertainty on account of tariffs continued to weigh on global M&A sentiment. Despite these headwinds, the technology and financial sectors led the market, each contributing 19% to the total global deal value.

Debt capital markets show resilience

Global debt capital market (DCM) activity remained robust in Q1’25, reaching USD3.2 trillion, up 6% compared to Q1’24. This marks the strongest first-quarter performance for DCM activity since 1980. Despite the overall growth in market value, the number of new DCM offerings declined by 2% YoY, falling to just over 8,540, the lowest in two years. Investment-grade corporate debt issuance dropped by 3% compared to the same period last year, while high-yield debt issuance declined by 2%, making this quarter the slowest start to the year for global high-grade corporate debt in the past two years. Green bond issuance totaled USD126 billion, representing a 13% decline from Q1’24. However, on a QoQ basis, green bond activity surged by 53% compared to Q4’24, indicating renewed momentum in sustainable finance. From a sectoral perspective, the technology, consumer staples, and materials sectors experienced double-digit percentage increases in DCM activity compared to Q1’24.

Global ECM activity slows in Q1’25, despite strong IPO performance

In Q1’25, global equity capital market (ECM) activity declined to USD142 billion, representing a 5% YoY decrease and marking the slowest opening quarter for global ECM activity in two years. The US accounted for 33% of total issuances, with proceeds falling 18% compared to Q1’24. In contrast, ECM activity in China tripled YoY, reaching its highest first-quarter share of global ECM activity in the past two years. Global initial public offerings (IPOs), excluding special purpose acquisition companies (SPACs), totaled USD26 billion, up 17% YoY, making it the strongest first quarter for IPOs since 2022. IPO proceeds on US exchanges rose by 12% YoY, reaching a four-year high. Convertible offerings amounted to USD24 billion, down 6% YoY, and accounted for 17% of total ECM deals. The technology, financial, and healthcare sectors were the most active, collectively representing 63% of all convertible issuances in Q1’25.

Top five M&A deals (Q1’25)

|

Date of announcement

|

Acquirer’s Name

|

Acquirer’s Location

|

Target

|

Target’s Location

|

Value (USD billion)

|

Target’s Industry

|

Deal type

|

|---|---|---|---|---|---|---|---|

|

Mar 18, 2025

|

Alphabet

|

US

|

Wiz

|

US

|

32.0

|

Tech

|

Cash

|

|

Jan 10, 2025

|

Constellation Energy

|

US

|

Calpine

|

US

|

26.9

|

E&P

|

Cash & stock

|

|

Jan 13, 2025

|

Johnson & Johnson

|

US

|

Intra-Cellular Therapies

|

US

|

14.6

|

Healthcare

|

Cash

|

|

Jan 24, 2025

|

Monte dei Paschi

|

Italy

|

Mediobanca

|

Italy

|

13.9

|

Financials

|

Stock

|

|

Jan 31, 2025

|

Borouge Group

|

Austria

|

Nova Chemicals

|

Canada

|

13.4

|

Industrials

|

Cash

|

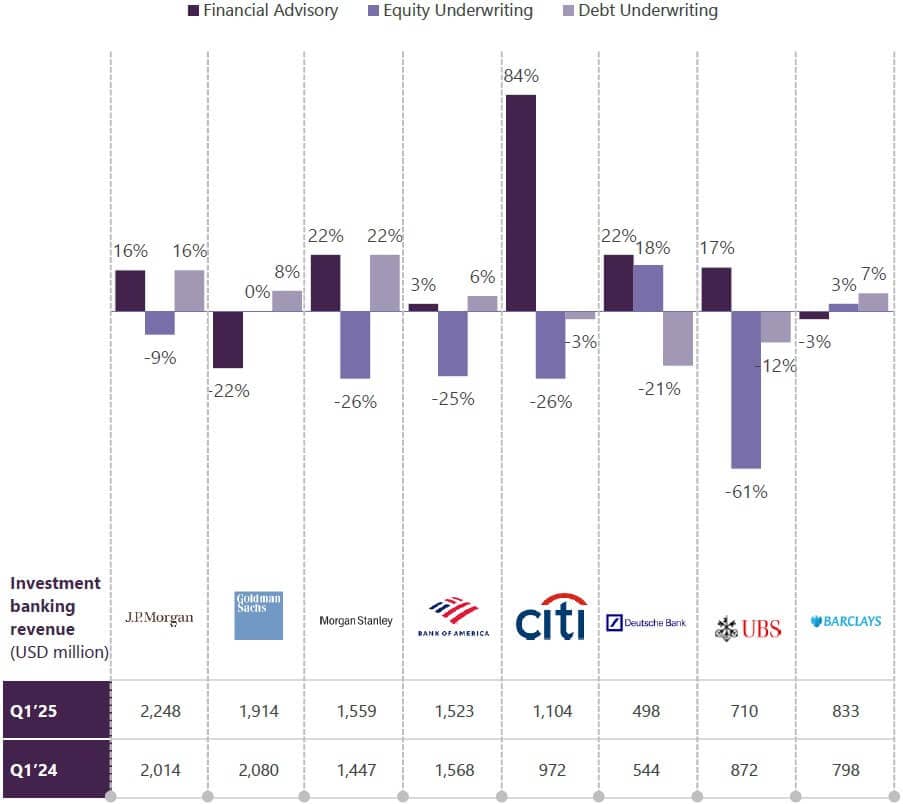

Investment banking revenues rebound amid improved market conditions

In Q1’25, investment banking revenues across all major banks rebounded, driven by improved global market conditions, however both equity and debt underwriting activities are still facing headwinds. The resurgence of mega deals, growing boardroom confidence fueled by strong corporate earnings, expectations of potential interest rate cuts later this year, and buoyant capital markets were key contributors to this recovery. Looking ahead, market performance is expected to strengthen in 2025, supported by pent-up demand for mergers and acquisitions and a robust deal pipeline, provided macroeconomic conditions remain stable on account of tariffs, trade policy and inflation.

Note: Revenue for Deutsche and Barclays were converted into USD using the exchange rate as of March 31, 2025

Revenue for Deutsche Bank reflects revenue from Origination & Advisory services

Bulge bracket investment banks – Q1’25 highlights

JP Morgan’s investment banking fees rose 12% YoY in Q1’25, driven by strong performance in debt underwriting and advisory services, which were partially offset by a decline in equity underwriting fees. Advisory fees increased by 16%, supported by the closing of deals announced in 2024, while debt underwriting fees also climbed by 16%, primarily due to heightened refinancing activity, especially in Leveraged Finance. In contrast, equity underwriting fees fell 9% YoY, reflecting ongoing challenges in the ECMs. Amid these conditions, the bank is maintaining a cautious outlook for its investment banking division but remains optimistic about the strength and potential of its deal pipeline.

Goldman Sachs’ investment banking fees declined by 8% YoY in Q1’25, primarily due to significantly lower net revenues from advisory, which were partially offset by gains in debt underwriting. The bank’s investment banking fee backlog increased QoQ, driven mainly by a rise in advisory activity, though it was partially offset by a decline in equity underwriting. Advisory net revenues fell 22% compared to Q1’24, while equity underwriting revenues remained flat. Debt underwriting revenues increased, primarily reflecting stronger performance in asset-backed and investment-grade issuance. Despite the mixed results, Goldman Sachs remains optimistic about its 2025 outlook and anticipates a further pickup in M&A and IPO activity.

In Q1’25, Morgan Stanley’s investment banking revenue rose by 8% YoY, supported by continued strength in advisory services and fixed income underwriting. Advisory revenue increased by 22% YoY, driven by a higher volume of completed M&A transactions. Fixed income underwriting revenue also grew by 22%, primarily due to increased issuance of non-investment grade loans. However, equity underwriting revenue declined by 26% YoY, as both issuers and investors remained cautious amid ongoing market uncertainty. The bank has a healthy and diversified M&A pipeline that surpasses levels seen in recent years, and it believes the business is well positioned for a sustained rebound in dealmaking activity.

Bank of America’s investment banking fees declined by 3% YoY in Q1’25, primarily due to lower equity issuance fees, which were partially offset by higher revenues from debt underwriting and advisory services. It reported strong performance in the DCM, particularly in leveraged finance, as well as continued momentum in the ECM. Considering the ongoing market volatility and concerns about potential economic shifts, the bank has adopted a conservative outlook for its investment banking business in FY’25.

Citi’s investment banking fees rose by 14% YoY in Q1’25, driven primarily by strong growth in advisory services, which was partially offset by declines in both equity and debt capital markets. Advisory fees surged by 84%, as the bank gained share across multiple sectors. The upside was supported by sustained client engagement and the successful completion of previously announced acquisitions, aided by a more favorable macroeconomic environment. Meanwhile, ECM fees declined by 26% YoY, reflecting a dip in the market wallet for follow-on offerings and convertible issuances. DCM fees fell by 3% YoY, compared to a particularly strong performance in the prior year.

Deutsche Bank’s revenue from its origination and advisory business declined by 8% YoY in Q1’25, primarily due to a loss on a partial sale and a markdown on a specific loan position within the leveraged DCM segment. Despite this, equity origination and advisory revenues rose by 18% and 22% YoY, respectively, reflecting a growing industry fee pool and market share gains. The upside was driven by businesses benefiting from prior strategic investments. Looking ahead, the leveraged DCM business aims to build on the recovery seen in the prior year, while its investment grade debt segment seeks to sustain the strong 2024 performance, both gained the market share due to expanding fee pools. The advisory business is looking to capitalize on the momentum from a robust prior year and leverage targeted hires made over the past two years.

UBS’s advisory revenue increased by 17% YoY in Q1’25, primarily driven by higher M&A transaction activity. In contrast, capital markets revenue declined by 28% YoY, largely due to a reduction in the accretion of purchase price allocation (PPA) adjustments on financial instruments and other related effects. Excluding the PPA impact, underlying capital markets revenue fell by 13% YoY, mainly due to weaker performance in leveraged capital markets. Within capital markets, DCM revenue declined by 12%, while ECM revenue plummeted by 61% in Q1’25. Despite the downsides, UBS’s board remains optimistic due to the strength of its M&A and leveraged capital market pipeline, as well as its improved positioning in the Americas – factors expected to support YoY revenue growth in 2025.

Barclays’ income from investment banking (IB) increased by 4% YoY in Q1’25, reflecting both an expansion in the overall fee pool and gains in market share. ECM fees rose by 3% YoY, while DCM fees grew by 7%, supported by heightened activity in leveraged finance and investment-grade issuance. However, advisory fee income declined by 3% during the same period.

M&A advisory firms – Q1’25 highlights

Like investment banks, major advisory firms experienced a rebound in revenue during Q1’25. While most firms acknowledge the elevated risks stemming from ongoing geopolitical tensions, economic uncertainty, inflationary pressures, and volatile market conditions, they remain optimistic. Looking ahead to the remainder of 2025, these firms anticipate improved access to debt capital and a pickup in deal-making activity but uncertainty around tariffs pose a key risk.

Note: Houlihan Lokey’s fiscal year ends in March (represents numbers for twelve months ending March-25)

M&A advisory firms’ performance and updates

Lazard reported a 17% YoY decline in revenue from financial advisory in Q1’25. Despite this decrease, the firm maintained a strong global presence and continued to advance its 2030 strategic plan, which emphasizes geographic expansion and service diversification. Since the beginning of Q1’25, Lazard has been actively involved in several high-profile and complex M&A transactions across global markets. Its leading restructuring and liability management practices have successfully handled a broad spectrum of challenging restructuring and debt advisory mandates. Additionally, the firm’s sovereign advisory division remains active, providing strategic counsel to governments and sovereign entities in both developed and emerging markets.

Houlihan Lokey’s revenues grew by 25% YoY in FY’25, mainly due to an increase in fee events driven by better M&A activity. The firm’s financial and valuation advisory business is gaining momentum with market recovery. Despite ongoing macroeconomic uncertainties, the firm remains optimistic about this fiscal year, expecting continued improvements in M&A and capital markets activity. Looking ahead, the firm anticipates fiscal 2026 to exhibit similar seasonality to 2025.

Moelis reported a 41% YoY increase in revenue for Q1’25, driven primarily by strong growth in its M&A and capital markets businesses compared to the same period last year. The firm continues to execute its strategy for organic growth and has recently added a technology-focused managing director in Europe and has another managing director specializing in business services in Europe committed to joining. Encouraged by the positive momentum heading into the remainder of 2025, Moelis believes it is better positioned to continue delivering value to both its clients and shareholders.

PJT Partners reported a 2% YoY decline in advisory revenues for Q1’25, primarily due to decreases in restructuring and private capital solutions revenues, which were largely offset by growth in strategic advisory revenues. The firm’s full-year outlook remains largely unchanged, with expectations for a significant increase in strategic advisory activity in H2’25. Additionally, PJT is positioning itself for potential growth in restructuring mandates should economic pressures persist.

Evercore reported a 30% YoY increase in advisory fees for Q1’25, driven by higher revenues from large transactions and a greater number of advisory engagements. In contrast, underwriting fees declined by 2% YoY, reflecting a decrease in the number of transactions the firm participated in. Entering 2025 with strong momentum, Evercore anticipates a gradual improvement in dealmaking activity over the course of the year.

PWP reported a 107% YoY increase in Q1’25 revenue, primarily driven by heightened M&A activity and increased demand for financing and capital solutions, supported by larger transactions and related fee-generating events across the business. Amid ongoing market volatility and a rapidly evolving geopolitical landscape, the firm continues to support clients in achieving their strategic and financial goals, while also investing in top talent across high-potential industry sectors to accelerate long-term growth for its shareholders.

The road ahead

Financial sponsors poised to reemerge as key drivers of M&A activity

Over the past three years, elevated interest rates have increased borrowing costs and compressed corporate valuations, prompting financial sponsors to delay asset exits. This has led to a buildup of unsold assets, creating a backlog that is expected to fuel a strong resurgence in M&A activity in 2025. Private equity firms, under growing pressure to return capital to investors, will be incentivized to monetize existing assets before launching new fundraising efforts. Additionally, the relatively lower valuations of publicly traded companies outside the US present compelling opportunities for sponsors to strategically deploy excess capital.

Corporates set to accelerate capital deployment through M&A

Globally, corporations are transitioning from being net sellers to net buyers, signaling a renewed appetite for strategic acquisitions. The trend is expected to gain momentum throughout 2025, supported by a more favorable macroeconomic and regulatory backdrop. As the US Federal Reserve’s interest rate target is projected to decline to 3.75–4% by year-end, the opportunity cost of holding cash will rise. In response, corporates are likely to shift their capital allocation strategies, favoring mergers and acquisitions over dividends and share buybacks. Moreover, a more accommodative antitrust and regulatory environment under the new US administration is anticipated to further stimulate strategic deal-making across a broad range of transaction sizes.

Valuation gaps and regional growth expected to fuel cross-border M&A

Over the past five years, the US economy has consistently outperformed those of Europe and the UK, prompting European companies to consider acquiring US firms to gain exposure to a more dynamic market. Conversely, US corporations are increasingly eyeing European targets to expand their international footprint and capitalize on comparatively lower valuations. Meanwhile, fast-growing economies in Asia continue to attract strong interest from private equity firms. As global M&A momentum builds, cross-regional dealmaking in Asia is expected to accelerate significantly, driven by both strategic expansion and the pursuit of high-growth opportunities.

Activist campaigns expected to remain elevated in 2025

With peak interest rates now behind and inflation largely under control, shareholder activism is poised to gain further momentum in 2025. Activist funds are raising larger pools of capital and increasingly targeting bigger, more prominent companies. As geopolitical and market conditions become more conducive to mergers and acquisitions, activists are expected to intensify pressure on corporate boards, particularly those perceived to have missed strategic M&A opportunities. Companies that resolved activist challenges in 2024 but continue to underperform may face renewed scrutiny and a potential second wave of activism. A more robust M&A environment, where buyers are more readily available, will likely embolden activist investors to push for structural changes at undervalued firms, especially through corporate separations and spin-offs aimed at unlocking shareholder value.

Global trend towards corporate simplification expected to continue

The global shift toward corporate simplification is likely to remain a key driver of M&A activity in 2025. Companies are increasingly focused on unlocking value by highlighting undervalued assets, separating non-core or divergent business units, and sharpening their geographic focus. This trend will see firms streamlining their portfolios to align with long-term secular trends, reallocating capital to higher-return opportunities, and enhancing strategic clarity. Regional separations are expected to become more common, enabling companies to better target specific investor bases and address the operational inefficiencies of managing cross-regional entities. Additionally, valuation disparities across markets will continue to encourage M&A, as companies seek more favorable capital environments through changes in domicile, stock exchange listings, or corporate headquarters.

Industry-focused M&A activity set to persist

Following several years of heightened regulatory scrutiny, the outlook for bank M&As is improving. Regulatory agencies are expected to ease entry barriers for new market participants and adopt a more accommodating stance toward mergers that meet statutory requirements. Beyond banking, industries such as energy, technology, and healthcare, which have already experienced significant deal activity in recent years, are poised for continued momentum in 2025. This will be driven by strategic realignments, consolidation efforts, and the pursuit of operational efficiencies. Moreover, the anticipated wave of industry transformation fueled by artificial intelligence is catalyzing M&A across the technology sector, with companies of all sizes seeking to strengthen their capabilities and competitive positioning through targeted acquisitions.

Tariff uncertainty puts global M&A activity on hold

As the M&A market contends with a turbulent landscape shaped by sweeping tariffs and broader market volatility, dealmaking has slowed considerably. These new complexities are forcing both buyers and sellers to adopt more nuanced approaches to transaction structuring and risk allocation. At the same time, economic and political instability is making financial forecasting increasingly difficult, further dampening confidence in executing cross-border deals. As a result, global M&A activity has entered a period of hesitation, with many transactions delayed or restructured in response to the evolving trade environment.

Talk to One of Our Experts

Get in touch today to find out about how Evalueserve can help you improve your processes, making you better, faster and more efficient.