In 2023, the asset and wealth management (AWM) industry witnessed profound global uncertainty, the possibility of a recession, increased interest rates, and growing margin pressure, highlighting the need for a sustainable business model that uses differentiated growth strategies. AWM leaders no longer have the liberty to delay their transformation efforts, more so because according to PwC, 16% of existing AWM firms are expected to be either acquired or shut shop by 2027, which is double the historical rate of turnover.

Despite the challenges, 2023 closed with a few early signs of optimism, as the tremendous pace of digital transformation and integrated technologies, such as artificial intelligence, machine learning, and digital assets, started playing a key role in increasing operational efficiency and improving client experience. Prominent AWM firms are learning to deal with these challenges and are, in fact, using these innovations to become more resilient and agile while galvanizing their commitment to re-access their strategies, operating models, and embracing new digital capabilities to drive value. This is raising the competitive bar and widening the gap between leaders and laggards.

However, experts expect 2024 to remain challenging for the industry due to continued volatility, primarily driven by existing / escalating conflicts and geopolitical uncertainties and their impact on various economies and markets. Restrictive central banks, limited fiscal flexibility, and geopolitical instability are expected to adversely affect global growth and wealth creation.

Below are some key themes that shaped the industry in 2023 and are expected to continue dominating in 2024:

Long-term scalability through M&A and strategic partnerships

In order to reinvent their business models, AWM firms will continue opting for inorganic growth through M&A and strategic partnerships. This will allow firms to gain scale, efficiency, capabilities, and new customers and tap into shared revenue opportunities while optimizing and streamlining operations and reducing costs.

- Asset managers are capitalizing these opportunities to venture into new asset classes and investor segments, explore new channels to capture market share and investor wallet, as well as access new geographies.

- Wealth managers are entering into strategic partnerships to improve their top line, optimize cost structures, reduce supervisory burden, build new capabilities, and tap new clients and advisors.

Increased focus on offering private market products both to high net worth (HNW) and retail investors

The AWM industry has been successful in making private markets more accessible to retail investors. Managers are keen to offer products that are beyond traditional investment options to create additional revenue streams and stay competitive. The industry is also witnessing increased interest from retail investors, as these products were traditionally off-limits for them due to the need for high investment minimums and illiquid structures. Technological advancement, investors’ growing interest in diversifying, and new and proposed regulations have driven the take-up of private market products among larger investor pools.

- Both registered and alternative asset managers are targeting retail investors for offering alternatives to grow overall AUM and compensate for institutional investors who are limiting their allocations towards alternatives. Retail investors offer an untapped opportunity (beyond HNW investors) for asset managers and enable them to focus on mass affluent and younger clients who wish to diversify their portfolios beyond traditional public market strategies.

- Wealth managers targeting HNW clients are educating their advisors on alternative investments and providing the right tools and platforms. They are also developing solutions for secondary market trading, liquidity and lending to increase wallet share which was not an option earlier.

Private markets are expected to fuel global AUM growth (at a CAGR of 13% in 2022-27, compared with the CAGR of 19% in 2017-22). Private equity is expected to outgrow other segments and account for 16% of global AUM by 2027, (compared with 12% in 2022), despite fundraising challenges following a slowdown in institutional allocation.

GenAI is a game-changer that will transform the traditional AWM business model

Recent developments in generative artificial intelligence (GenAI) have taken the industry by storm. The technology has made significant strides due to applicability in almost every aspect of the AWM business, including operations, finance, research and analytics, risk management, investment relations, compliance, and M&A. Advanced analytics is being leveraged for portfolio optimization, investment strategies, asset allocation, and algorithmic trading to enhance risk management processes. Risk can be managed by continuous monitoring of market conditions, news and analysis sentiments, and providing early signals. GenAI can significantly improve operational efficiency also, like enhancing data collection and sharing across firm, mine structured financial data and unstructured data, analyze and personalize client’s investment portfolios and make recommendations, summarize reports, execute trades, keep track of tax and regulations, customer segmentation, engagement, and personalizing marketing materials. These curated and real-time insights and market intelligence can help portfolio managers in investment research and help them make informed and data-driven investment decisions.

Wealth managers can use GenAI to customize personal advice. Chatbots and virtual assistants are engaging customers to know their preferences, objectives, financial obligations, risk threshold, etc. to help in offering individualized advice and better financial outcomes resulting in business growth through new client acquisition and increased wallet share of existing clients. Wealth managers are using/planning to use Gen AI to boost productivity and accuracy across the value chain by automating manual administrative tasks including pre- and post-meeting paperwork, dynamic agendas, or tracking life events and milestones for clients in real time.

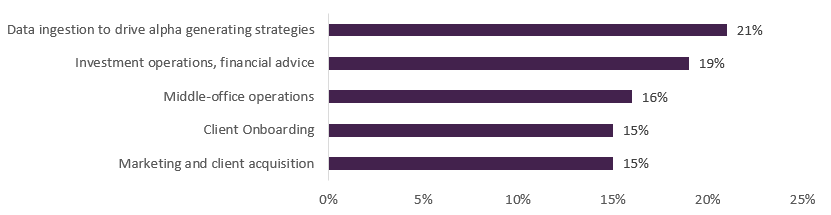

As per an EY August 2023 survey of wealth and asset management firms with more than $2 billion in revenue, alpha generation and financial advice were considered to be the highest-impact use case for Gen AI.

It also levels the playing field as smaller firms can compete with big players in research, sales, and technology because GenAI can ‘democratize’ coding.

Different approaches to ESG; standardization and reliable metrics imperative for trust building

There was a tremendous investor demand for ESG products in 2023; 2024 is unlikely to be different, as sustainability is becoming deeply ingrained in the financial foundations of companies. As per PwC, almost one-third of CFOs are already looking at the potential effects of climate change on financial outcomes.

However, AWM firms are approaching sustainable investing in different ways because of increasing regulatory pressure and scrutiny, anti-ESG backlash, under-performance, and persistent fund outflows. These factors have raised questions and concerns about the ‘sustainability’ of current ESG products and have divided players into two groups. First and the larger group will integrate ESG factors into existing mandates and will customize based on client preferences (for example, using direct indexing). The second group is expected to focus more on the ESG impact on real world through differentiated offerings such as sustainable thematic investing and impact funds, which can define and track desired outcomes for investors in a better manner. Therefore, this group will benefit from favorable demand trends (for instance, average net flows for climate-specific funds were 19% compared with only 2% for all ESG funds over the last year), thereby increasing their market share.

On the regulatory front, there is a growing need for standardization and reliable ESG scoring metrics to build trust among clients. Therefore, regulations around ESG traceability and scoring are becoming tighter due to pressure from investors. Some recent regulations include the Sustainable Finance Disclosure Regulation (SFDR) and the Corporate Sustainability Reporting Directive (CSRD). In 3Q 2023, the EU adopted the new European Sustainability Reporting Standards to support its CSRD, which covers a whole spectrum of ESG issues (like human rights, biodiversity, and climate change). Moreover, the EU’s new SFDR amendments, which aim to make the sustainability level of investee companies transparent, accessible, and comparable, are set to go into effect in 2024.

Accentuated costs and outsourcing as a plausible solution

Apart from their relentless pursuit of gaining competitive advantage to differentiate, accelerating operational rigor and technical agility, AWM firms will also have to continue focusing on streamlining cost structures. Identifying cost inefficiencies and targeting scalability gaps will not only help managers scale back and streamline their operating models, but also prioritize strategic growth and build core competencies. To achieve this, AWM firms plan to continue exploring options like outsourcing or location strategies to control/manage costs. Not just cost, but outsourcing can also help AWM firms address the issues related to resource/process inefficiency and lack of skilled experts. Outsourcing can help firms build resiliency into daily operations by transitioning in-house operational processes to outsourced middle- and back-office service providers. As per Deloitte’s 2024 outlook survey, in the next 12-18 months, 29%, 23%, and 28% of firms are planning to opt for outsourcing for front, middle, and back-office processes, respectively (compared with 4%, 5%, and 5% who are planning to build a strategy for front-, middle-, and back-office processes, respectively).

Overall, AWM firms are being more selective about taking up transformative projects with increased focus on shorter duration ones that balance cost optimization with innovation. Business model or product innovation and improved customer experience are projected to drive majority growth. High-quality, agile firms that have or are working towards operations effectiveness, product optimization, and client engagement advances will significantly outperform their peers.

Evalueserve – A valued partner

Evalueserve offers a hybrid and scalable insights program that includes news of competitors, thought leadership, industry trends, tech disruptions, product launches, and more to provide actionable and timely results. Its unified view of the competitive landscape helps users to compete intelligently and make informed decisions.

Key offerings

Insightsfirst Competitive Intelligence (CI) – An AI-driven proprietary platform

- Competitive market watch, powered by AI / NLP engines

- Thought leadership and publication tracking, using scraping and text analytics

Knowledge solutions from domain experts

- Competitive landscape analysis

- Industry factbooks for retail / institutional market

- Industry landscape analysis for intermediary distribution channels (brokers, advisors, etc.)

- Detailed competitor analysis and profiling

- Product benchmarking and white space analysis

- Brand assessment and positioning studies

Benefits

- Powering up competitive intelligence programs

- AI / NLP-based multi-fold scaling

- Curated to specific requirements of departments (marketing, strategy, CIO office, etc.)

- Domain experts to provide additional intelligence and ensure zero noise

- Support in the adoption of a smart and process-oriented approach to track competitors and collaborate internally (using newsletters, dashboards, alerts, etc.)

Talk to One of Our Experts

Get in touch today to find out about how Evalueserve can help you improve your processes, making you better, faster and more efficient.