Overview

In the last three years, the consumer and retail sector witnessed more disruption and transformation in consumer behavior and preference than it did over the past two decades. Although the direct impact of COVID-19 faded to a large extent in 2022, its indirect effects will be felt for years to come.

As we publish our third annual update on M&A and capital market activity in the North American consumer and retail sector, an unstable geopolitical environment, a sharp rise in the cost of living, and a looming recession are threatening to add more uncertainty to purchasing behavior and, ultimately, to the sector’s performance.

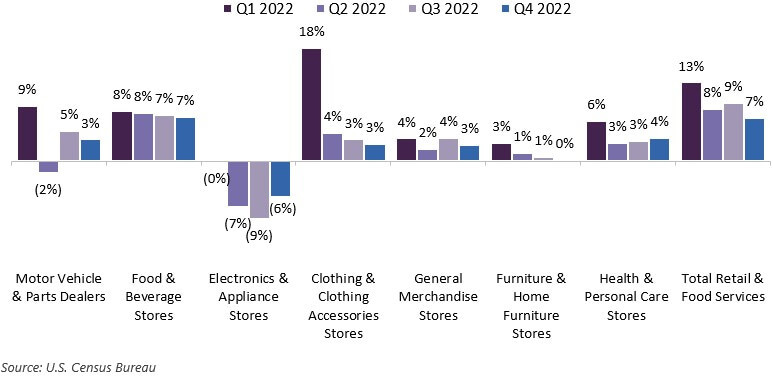

According to the US Census Bureau’s seasonally adjusted data, retail and food services sales grew by 7.0% Y-o-Y to USD 2,054 billion in Q4 2022 from USD 1,920 billion in Q4 2021. For FY 2022, retail and food services sales grew 9.3% Y-o-Y to USD 8,125 billion, compared with USD 7,434.8 billion in FY 2021. The upside was driven primarily by key segments such as food and beverages, healthcare and personal care, motor vehicles and parts, and clothing and clothing accessories. Furthermore, general merchandise played a prominent role in Q4 2022.

In December 2022, US retail sales continued to decline 1.1% on a M-o-M basis, to USD 677.1 billion. This decline was due to a pullback in consumer spending amid inflation and rising interest rates, as consumers grew more cautious and moderated their spending during November and December.

As per Comscore’s State of Digital Commerce report, in 2022, online retail sales (excluding travel) surpassed USD 1 trillion for the first time. E-commerce sales also witnessed their highest-ever quarter in Q4 2022, at USD 332.2 billion.

Figure 1: Y-o-Y Change (%) in US Retail Sales

According to a report by the US Bureau of Labor Statistics, the unemployment rate in the US declined slightly to 3.4% in January 2023, compared with 3.5% in December 2022. The number of unemployed people fell by 517,000 over the same period to 5.7 million as more jobs became available thanks to the improving performance of the leisure and hospitality, professional and business services, and healthcare segments. The unemployment rate in January was the lowest that the US has seen in over five decades. It reflects a stubbornly tight labor market and poses a potential headache for Federal Reserve officials fighting inflation.

M&A Activity

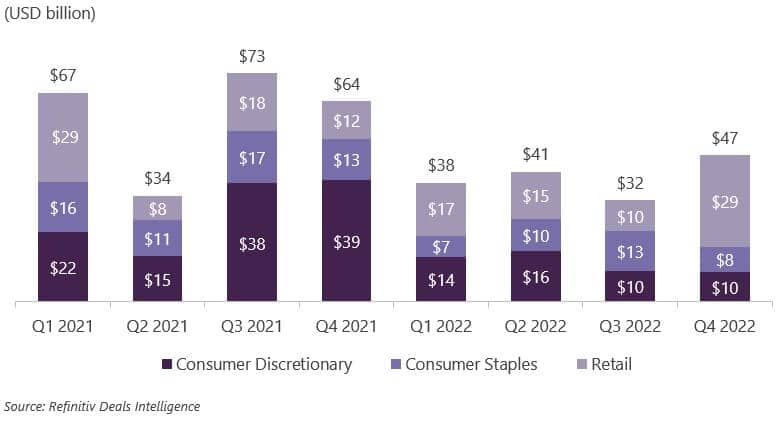

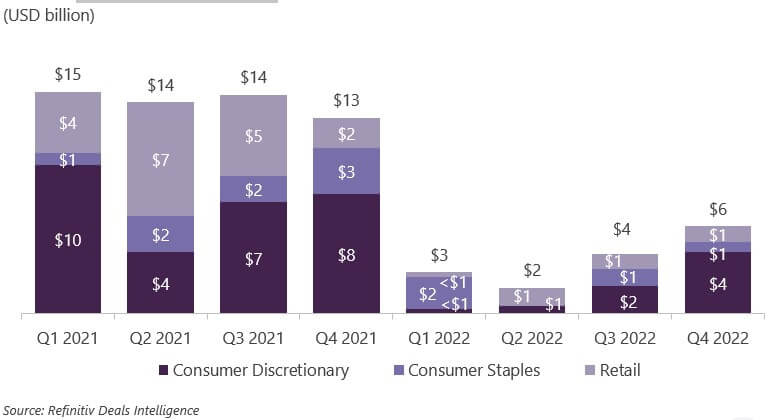

M&A activity in the consumer and retail sector in the Americas (North America, the Caribbean, and Latin America) surged by 44.6% in Q4 2022 to USD 46.7 billion, compared with USD 32.3 billion in Q3 2022. The upside can be attributed to a significant increase in M&A activity in the retail segment.

However, it declined by 33.2% to USD 158.2 billion in 2022, compared with USD 236.8 billion in 2021. As

of December 12, 2022, 3,170 M&A deals had been announced in the sector, down by 4.4% on a YTD basis from December 2021. The persistent decline in M&A activity was primarily due to inflationary pressure, rising interest rates, restricted debt markets, geopolitical risks, and labor shortage, all of which hurt investor confidence.

While M&A volume in FY 2022 was lower than in FY 2021 (which witnessed record growth in deal volume), it was similar to the pre-COVID levels. As we enter 2023, the short-term economic outlook remains clouded by global recession fears and an interest rate hike by the Federal Reserve. However, we expect significant capital and several investment opportunities to be available in 2023 as companies look for strategic opportunities to scale operations, secure access to key products, and optimize portfolios.

Figure 2: M&A Deal Value

Bankruptcies

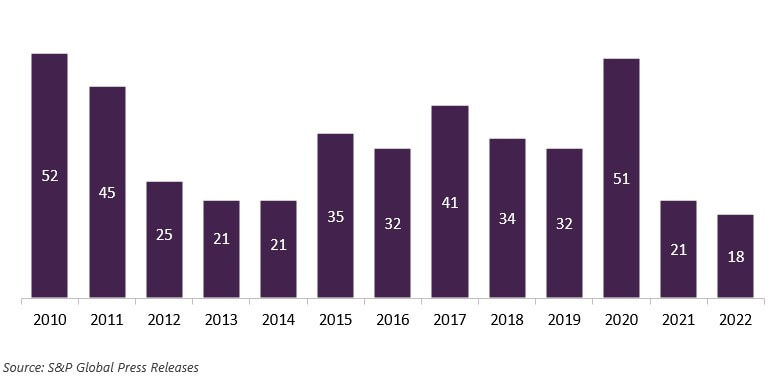

In FY 2022, 18 companies in the US retail sector had filed for bankruptcy, the lowest across comparable periods since 2010. The low number of bankruptcy filings can be attributed to a significant rebound in offline retail activities as consumers returned to stores. However, this does not imply that the sector is out of danger now. We expect retail bankruptcies to resurface in 2023, considering the recent price increases and the pullback in consumer spending.

Figure 3: Number of Bankruptcies in US Retail Sector (2010–2022)

Among the retail companies filing for bankruptcy was Vital Pharmaceuticals (VPX), a developer of performance beverages, supplements, and workout products. The company filed for Chapter 11 bankruptcy in October 2022, backed by USD 100 million of additional financing from VPX’s syndicate lenders to help ensure uninterrupted operations during the restructuring process.

Capital Market Activity

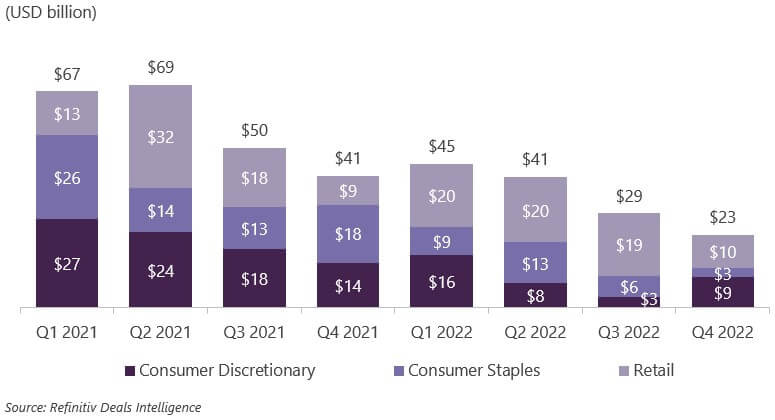

Capital-raising activity in the Americas continued to move towards historically low levels in 2022 due to macroeconomic headwinds such as inflation, rising interest rates, and geopolitical uncertainties. The US leveraged loan markets and high-yield bond markets witnessed significant declines in issuance during the year, as soaring inflation and rising interest rates drove up borrowing costs, which in turn dampened the risk appetite of investors and significantly reduced M&A activity. The value of debt-raising activity in the Americas declined by 22.5% to USD 22.7 billion in Q4 2022, compared with USD 29.3 billion in Q3 2022. Overall, in 2022, debt-raising activities declined by 39.6% Y-o-Y to USD 137.4 billion, compared with USD 227.3 billion in 2021.

Figure 4: DCM Quarterly Deal Volume

The value of equity-raising activities in the Americas surged by 46.2% to USD 5.7 billion in Q4 2022 vs. USD 3.9 billion in Q3 2022. The upside was primarily driven by a surge in equity-raising activities in the consumer discretionary segment. Overall, equity-raising activities declined by 74.7% annually in 2022 to USD 14 billion, compared with USD 55.4 billion in 2021, owing to a slowdown in IPO activity due to high inflation, rising interest rates, and an uncertain economic scenario. We believe investors are likely to be selective on pricing/valuation until confidence in equity market valuations returns to pre-pandemic levels.

Figure 5: ECM Quarterly Deal Value

The Road Ahead

Inflationary pressures, geopolitical risks, rising interest rates, labor shortages, input cost increases, and other issues persisting at the start of 2023 are likely to gradually tone down during the year. Consumer and retail companies are expected to continue to focus on scale, technology, and customer experience as key competitive advantages. Consumers will likely continue to be careful about how and where they spend their money, favoring necessities over discretionary purchases and seeking more value with better price points from cost-effective brands.

M&A activity will likely remain subdued due to market volatility for some more time, particularly for listed companies that have recently undergone price corrections. However, small consumer companies with solid product pipelines are likely to remain attractive M&A propositions for larger companies and sponsors. Opportunistic M&A will be expected to rise, backed by private equity funds with significant dry powder and large corporates. On the other hand, companies that are highly leveraged will actively pursue divesting non-core assets across their portfolios, which will further create opportunities for opportunistic buyers as these assets come to market. Investors will continue to focus on refining their portfolios, especially in direct-to-consumer, to adapt to consumer trends that have accelerated during the COVID-19 pandemic. Crisis resilience and adaptation to new ways of working and living will drive deal activity as well as the ever-important strategic search for growth and margin.

Debt markets may struggle in the near term, as economic headwinds will likely keep issuers on the sidelines and investors are expected to demand higher returns on riskier assets.

2023 will likely be an exciting year for the consumer and retail sector, after witnessing a significant decline in M&A as well as in capital market activities in 2022 due to the volatile macroeconomic backdrop. However, given the inflationary pressure and recessionary fear at the same time, things depend on how soon the US Federal Reserve will decide to end the interest rate increases. We believe this will act as a major catalyst for greater stability and certainty, leading to an upswing in the overall activities within the sector.