As AI reshapes semiconductor competition, South Korea is attempting to turn memory leadership into a broader, more resilient ecosystem—anchored by system semiconductors, supply-chain localization, and execution discipline.

The new semiconductor moat is execution

The global semiconductor race has entered a new phase. It is no longer defined simply by who commits the most capital, but by who can execute at scale, align ecosystems, and translate investment into output reliably. In an AI-driven cycle, where speed-to-capacity, supply assurance, and ramp efficiency increasingly determine who captures value, execution has become the new moat.

That shift matters because the industry’s constraints have changed. Capital remains essential, but it is no longer the scarcest input. What increasingly limits competitiveness are operational frictions: infrastructure readiness, tool and material availability, qualification timelines, yield learning, and access to specialized engineering talent.

Against this backdrop, South Korea offers one of the most revealing case studies in industrial resilience. Its semiconductor strategy is not only about preserving strength in memory; it is about reengineering the broader ecosystem so Korea can remain competitive in a more complex, AI-shaped market.

Korea’s strategic tension: strong in memory, vulnerable in structure

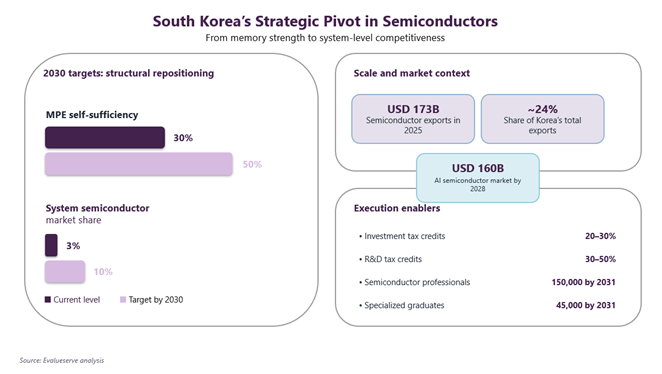

South Korea’s strength in semiconductors is undeniable—but increasingly unbalanced. Semiconductors are the country’s largest export category, reaching approximately USD 173 billion in 2025, or nearly 24% of total exports. Chips are therefore not just an industrial priority, but a core pillar of national competitiveness.

Yet Korea’s strength also reveals its central vulnerability: it remains heavily concentrated in memory semiconductors. That concentration has historically been highly profitable, but it also leaves the country exposed to two structural risks: cyclicality, given the pricing volatility of memory markets, and concentration risk, since too much of Korea’s semiconductor performance remains tied to a single segment.

This is the real strategic tension at the heart of Korea’s semiconductor policy. The question is no longer whether Korea can remain strong in memory. The more important question is whether Korea can convert memory leadership into broader system-level competitiveness before concentration becomes a drag on long-term resilience.

Why system semiconductors are the real test

If memory semiconductors have been Korea’s competitive foundation, system semiconductors represent its most important strategic inflection point—and its largest upside opportunity. They offer a pathway out of both memory cyclicality and segment concentration.

System semiconductors span a broad set of technologies, including AI and high-performance logic chips such as GPUs, NPUs, ASICs, and SoCs; power semiconductors critical to EVs and energy systems; automotive semiconductors with long product cycles and high entry barriers; and increasingly advanced packaging and heterogeneous integration, where system-level performance is defined.

Unlike memory, which is largely a volume-and-scale game, system semiconductors are more design-intensive, more application-specific, and more tightly linked to end-market ecosystems. The basis of competition therefore shifts from manufacturing scale to system integration capability.

AI is not just increasing semiconductor demand; it is reshaping where value is created across the stack. The AI semiconductor market is expected to grow at around 24% CAGR between 2023 and 2028, potentially reaching USD 160 billion by 2028, while AI workloads increasingly depend on architectures that combine compute, memory, and interconnect.

In practice, that means value is moving toward compute architectures, energy efficiency, data movement optimization, and advanced packaging such as HBM integration, chiplets, and 3D stacking. These are precisely the areas where system semiconductor capabilities matter most.

For Korea, this makes system semiconductors far more than a diversification theme. They are the test of whether the country can move from being a dominant component supplier to becoming a full-stack semiconductor power.

Korea’s answer: build resilience through ecosystem expansion

If memory semiconductors have been Korea’s competitive foundation, system semiconductors represent its most important strategic inflection point—and its largest upside opportunity. They offer a pathway out of both memory cyclicality and segment concentration.

System semiconductors span a broad set of technologies, including AI and high-performance logic chips such as GPUs, NPUs, ASICs, and SoCs; power semiconductors critical to EVs and energy systems; automotive semiconductors with long product cycles and high entry barriers; and increasingly advanced packaging and heterogeneous integration, where system-level performance is defined.

Unlike memory, which is largely a volume-and-scale game, system semiconductors are more design-intensive, more application-specific, and more tightly linked to end-market ecosystems. The basis of competition therefore shifts from manufacturing scale to system integration capability.

AI is not just increasing semiconductor demand; it is reshaping where value is created across the stack. The AI semiconductor market is expected to grow at around 24% CAGR between 2023 and 2028, potentially reaching USD 160 billion by 2028, while AI workloads increasingly depend on architectures that combine compute, memory, and interconnect.

In practice, that means value is moving toward compute architectures, energy efficiency, data movement optimization, and advanced packaging such as HBM integration, chiplets, and 3D stacking. These are precisely the areas where system semiconductor capabilities matter most.

For Korea, this makes system semiconductors far more than a diversification theme. They are the test of whether the country can move from being a dominant component supplier to becoming a full-stack semiconductor power.

Korea’s answer: build resilience through ecosystem expansion

South Korea’s response reflects that strategic reality. Its semiconductor strategy is built on a clear pivot: from memory champion to integrated semiconductor powerhouse. Two national targets illustrate that repositioning: raising MPE (materials, parts, and equipment) self-sufficiency from roughly 30% to 50% by 2030, and expanding system semiconductor market share from roughly 3% to 10% by 2030.

The logic is straightforward. Korea is trying to do three things at once:

- Reduce supply-chain vulnerability by strengthening domestic MPE capabilities

- Diversify profit pools beyond memory into system semiconductors

- Capture AI-era growth through advanced architectures, packaging, and computing applications

This is why system semiconductors sit at the heart of the strategy. Korea’s plan explicitly aims to expand system semiconductor capabilities through targeted funding for AI and system semiconductor R&D, investment in power and automotive semiconductor programs, development of next-generation architectures such as Processor-in-Memory (PIM) and on-device AI chips (NPUs), and support for fabless ecosystem expansion.

These efforts are designed to address Korea’s main structural gap: strong manufacturing capability, but comparatively weaker system design depth and ecosystem breadth.

Execution enablers: policy continuity, talent, and clusters

Seen through this lens, Korea’s policy design matters not because it is flashy, but because it is intended to reduce execution risk. Unlike some peers that rely more heavily on large upfront subsidies, South Korea emphasizes policy stability and long-term incentives. Key tools include investment tax credits of 20–30% for equipment and facilities, R&D tax credits of 30–50%, and targeted funding for next-generation semiconductors and AI-related innovation.

The objective is to lower breakeven risk and sustain investment momentum across cycles—not simply to win headlines.

Talent is the second major execution enabler. One of the most underestimated constraints in semiconductors is human capital, and Korea’s strategy treats it accordingly. The country aims to train 150,000 semiconductor professionals by 2031, develop 45,000 specialized graduates, and expand visa programs to attract global engineering talent.

Clusters are the third pillar. The broader strategy links MPE localization, cluster development, and talent expansion to the same objective: building an ecosystem where design, manufacturing, packaging, suppliers, and specialized labor reinforce one another. In system semiconductors especially, the constraint is not fabs alone—it is whether the surrounding ecosystem can operate as an integrated system.

Why this matters: system semiconductors as Korea’s re-rating engine

System semiconductors matter not just for growth, but for valuation, positioning, and long-term resilience. If Korea can scale meaningful system semiconductor capability, the result would be a shift in profit pools: value capture would extend beyond memory cycles, margins could become less volatile, and exposure to high-growth end markets such as AI, EVs, and industrial applications would increase.

It would also reposition Korea in the global value chain. Expanding system capabilities would allow Korea to participate more deeply in the AI infrastructure stack, automotive electronics platforms, and next-generation computing architectures. That would move Korea from being primarily a component supplier to a more integrated system-level player.

Finally, it would broaden the opportunity landscape around Korea’s semiconductor ecosystem. A more capable system semiconductor base would create second-order opportunities across advanced packaging, materials and equipment tied to logic processes, and design, verification, and software-related layers. In that sense, system semiconductors are not just another product category; they are Korea’s re-rating engine.

This is where the competitive frontier is moving.

Implications for investors and executives

For investors, South Korea should be evaluated not as a single incentive package, but as an execution ecosystem. In markets where the key risk is schedule slippage, yield instability, and ecosystem bottlenecks, execution reliability can matter more for IRR than marginal differences in subsidy size.

For executives, the key implication is strategic positioning. The Korean opportunity is no longer confined to memory. Supply partnerships, co-development, M&A, and localization strategies should be designed with the expectation that Korea is trying to expand beyond memory into a broader system semiconductor ecosystem.

For both groups, talent should be tracked like capex. Graduation throughput, retention, visa practicality, and engineering availability are not side issues; they are leading indicators of whether announced capacity can actually translate into output. In semiconductors, talent is the gatekeeper of execution.

Final insight: Execution—not ambition—is becoming the true measure of competitive advantage.

In the AI era, semiconductor leadership will not be determined by who spends the most—but by who can design and execute a complete, resilient system. It is about engineering resilience across the entire system—reducing concentration risk, localizing critical supply layers, building out system semiconductor capability, and aligning policy, capital, and talent to support execution.

That makes Korea’s experience relevant far beyond semiconductors. It reflects a broader shift in industrial competition: leadership increasingly belongs to those who can align policy, supply chains, skills, and technology into a coherent and executable system.

Talk to One of Our Experts

Get in touch today to find out about how Evalueserve can help you improve your processes, making you better, faster and more efficient.