Indonesia is an emerging ground for electric vehicle (EV) market, estimated to surpass over USD 20 billion by 2030. This surge is underpinned by the government’s bold target to deploy 2 million units of electric four-wheelers and 13 million two-wheelers on the roads. With less than five years left towards the goal, untapped opportunities for growth span the entire EV ecosystem, especially for companies from China, whose robust supply chains and technology leadership offer a blueprint for scale in Indonesia. Extending beyond the EV manufacturing value chain, further prospects for cross-border collaborations across the entire EV ecosystem in Indonesia exist, spanning EV battery production, charging infrastructure development, and innovative mobility services.

EV Manufacturing: Unlocking Growth in Four-wheel Segment

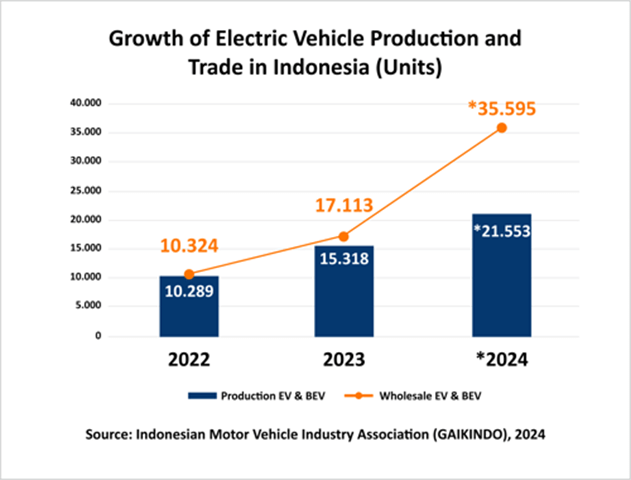

The two- and three-wheel EV segments in Indonesia have been saturated with 63 companies in the market, jointly possessing annual production capacity of 2.28 million units. In contrast, the four-wheel and bus segments are in still nascent stage, comprising just 16 manufacturers with a total annual capacity of slightly over 70,000 units. Despite a staggering 78% growth in the EV population since 2023, Indonesia still lags behind from reaching the government’s ambitious target, registering only 207,000 EVs in 2024.

Within a short timeframe, Chinese manufacturers have surged to the top of Indonesia’s electric car sales, outpacing other established global brands, such as Tesla, Toyota, Hyundai, BMW, Mitsubishi, Volvo and Mercedes Benz. In 2024, the products of BYD, Wuling, and MG occupied top eight list of electric car sales, being the only products each surpassing 2,000 units in sales. Notably, BYD claimed 36% of market share in less than a year. The domination of Chinese manufacturers is expected to continue in the long run as ten products from these top 3 players collectively occupied over 84% of Indonesia’s EV market in the first half of 2025 alone, showing a clear sign of growing Indonesian consumer acceptance.

The significant gap between current sales figures, production capacity, and government targets highlights vast opportunities for new entrants to invest in local EV manufacturing. Chinese brands are particularly well-positioned to break into Indonesia market and expand further, owing to their rapid dominance which signals strong brand acceptance, competitive pricing, and effective localization strategies. The great combination of the expanding middle class market, government subsidies, tax incentives, and existing positive sentiment towards products from Chinese manufacturers, opens the doors for other Chinese EV manufacturers to expand their presence in Indonesia’s evolving four-wheel EV market.

Battery Ecosystem: Maximizing Potentials of Indonesia’s Nickel Reserves and Downstream Effort

Indonesia has emerged as a global powerhouse in upstream nickel industry, accounting for 42% of the world’s nickel reserves and 51% of global mine production based on 2023 data. Recognizing the immense strategic potential of its abundant nickel resources, the current administration has pushed nickel downstreaming to the center stage as one of the top priority industries. To accelerate this transformation, Indonesia has launched several measures such as restricting raw nickel export and promoting investment in nickel processing and downstream industries, with the aim to become a global hub for EV battery production.

Meanwhile, China has developed a robust EV battery ecosystem and dominated the global market, contributing 70% of global production capacity and 38% of global supply in 2024. Despite having merely 4.4 million tons of nickel reserve, leading Chinese electric vehicle battery producers like Contemporary Amperex Technology Co. (CATL) and Tsingshan Holding Group have invested in nickel mining sites worldwide to secure raw material supplies, driving China’s nickel ore import to become a USD 3.3 billion market as of 2023.

Indonesia’s vast nickel reserves and supportive regulatory environment for EV battery manufacturing, coupled with China’s global leadership in the EV battery market, create substantial opportunities for Chinese companies to pursue vertical integration. By investing capital and deploying their technological prowess in Indonesia to establish integrated battery production facilities in Indonesia, these players can secure stable access to raw materials and diversify their production bases amid geopolitical uncertainties and growing EV demand, ultimately reducing costs. The synergy strengthens Indonesia’s competitive edge as a regional EV supply chain hub and helps address crucial supply chain security and cost challenges in the future global EV battery market.

Charging Infrastructure: Public-Private Partnerships for Nationwide Expansion

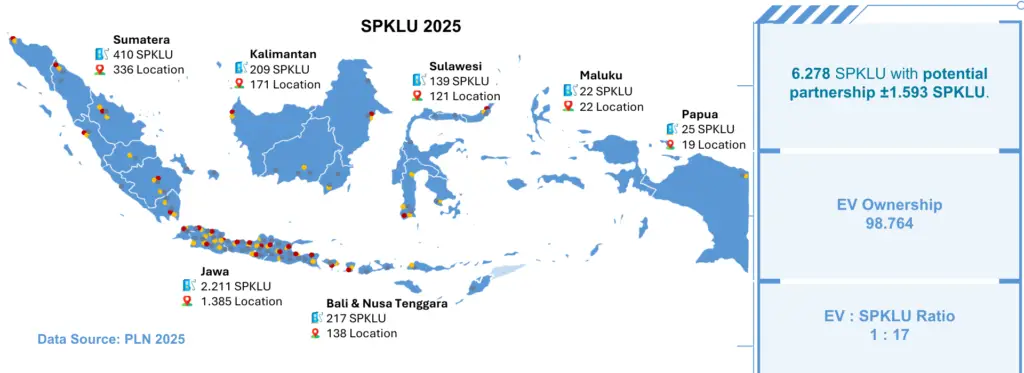

Mirroring the rapid progress in Indonesia’s EV market, the EV infrastructure segment also shows promising growth as charging demand in Public Electric Vehicle Charging Stations (locally known as SPKLU) skyrocketed by 337% from the previous year, recording 402,509 transactions in 2024. Responding to this growing demand, state-owned electricity company, PT PLN (Persero), who plays an essential role in developing the EV infrastructure in the country, boosted the number of charging stations by 299% to 3,233 units in 2024. This marks 10% progress to reach the government’s target of 32,000 SPKLUs by 2030. Additionally, Home Charging Services also saw a stellar growth by 302% in 2024 for Home Charging Services, totaling 28,356 units.

Indonesian government is actively working on providing regulations to boost private sector participation in both the investment and operation of EV charging stations. These measures promise easier access for foreign companies to build presence in the country’s EV infrastructure sector, particularly from China which has established itself as global leader of EV infrastructure market in terms of number of installations, service extension, and diverse range of options.

In recent years, PT PLN (Persero) has forged partnerships with multiple players across the EV infrastructure vertical to keep up with the increasing demand, including partnership in Home Charging Services to raise adoption with 22 electric car brands, such as BYD, Wuling, and Neta. These incumbent players have paved the way for Chinese companies for further collaboration with PT PLN (Persero) to disrupt Indonesia’s EV infrastructure market by contributing innovative technologies and expanding charging options, while tapping access to the state-owned company’s vast national network of power infrastructure.

Customer Mobility: Electrifying Indonesia’s Taxi Market

Beyond the production value chain, untapped opportunities are emerging in the service sector with one of the most promising areas being customer mobility. Xanh SM, Vietnam’s first all-electric taxi operator, debuted in the Indonesian market in late 2024, marking its venture into the third Southeast Asian country following Vietnam and Laos. As the taxi arm of Vinfast, a Vietnam’s flagship EV brand, Xanh SM pioneered a shift in Indonesia’s mobility industry by operating an entirely electric fleet comprised exclusively of VinFast cars. Starting with a pilot launch in Jakarta, Xanh SM has announced plans to expand to Bali and ramp up its fleet to 10,000 electric taxis.

Although Xanh SM was not Indonesia’s first taxi provider in Indonesia to operate EV in its fleet, its entry has reinvigorated competition and motivated other players to accelerate EV adoption within their fleets. For EV Chinese brands, this opens a window of opportunities to tap into customer mobility segment, taking advantage of their established presence in the country’s four-wheel EV market. Potential strategies include direct entry into taxi business or establishing partnerships with local taxi operators to integrate the Chinese-branded electric cars into the fleet. Such initiatives allow Chinese brands to offer firsthand experiences of their EV products to potential customers, cultivate brand familiarity, and enhance market reputation beyond traditional dealerships channels.

What’s in it for Indonesian players?

The investment of Chinese players in Indonesia’s EV ecosystem opens new avenues for local entities to partake in accelerating the government’s EV targets. Collaborations between domestic companies and Chinese investors extend beyond capital injection, serving as vital channels for two-way knowledge transfer and capacity building. Through joint research and development efforts, Indonesian firms can leverage their deep understanding of local market dynamics, culture, and consumer behavior, whereas Chinese partners can bring their cutting-edge technologies, industry expertise, and valuable lessons gathered from successful EV rollouts in China and globally.

The impact of Chinese investment goes beyond the EV ecosystem itself, creating positive spillover effects across multiple sectors. Integrating one or more links of the EV value chain with relevant industries allows EV players to reach broader consumer segments across Indonesia’s vast archipelago and capture Chinese customers concurrently. In addition to mobility services, promising use cases for EV integration are also identified in other customer-facing sectors, such as logistics, retail, transportation, financial services, food and beverage, and tourism.

What’s to Look Forward to?

Indonesia’s EV ecosystem is poised for transformative growth, driven by a combination of ambitious government targets, vast natural resources, and strategic collaboration with Chinese industry leaders. China’s global dominance in multiple links across EV value chain provides critical technological expertise and investment that can accelerate Indonesia’s ambitions while fostering deep integration across the value chain. By capitalizing on these synergies, Indonesia can position itself as a regional leader in sustainable mobility, innovation, and green economic development, setting a compelling example for emerging markets worldwide.

The development of the EV ecosystem in Indonesia is just one example of the many bilateral business prospects between ASEAN and China. Abundant cross-border opportunities are also present for stakeholders in other Southeast Asian countries to seize amid dynamic global markets, fueled by rapid advances in innovation and technology. In upcoming blogs, we will bring you in-depth analysis surrounding business potentials in other markets such as Thailand and Vietnam, uncovering new trends and emerging bidirectional opportunities across Southeast Asia and China.

Evalueserve in Asia

Since 2005, Evalueserve has been serving as a strategic hub for delivering research and analytics solutions tailored to the complexities of Asian markets. Our team of 250+ consultants and knowledge specialists in the region support decision-makers across Greater China, Japan, South Korea, and Southeast Asia.

We are a trusted partner to the world’s largest financial institutions, corporate enterprises, and professional services firms. We help our clients with scalable, multilingual expertise and regionally grounded insights in Asia, enabling them to navigate local market dynamics, regulatory environments, and competitive landscapes with confidence. Our ISO 27001-certified operations ensure that data integrity and confidentiality remain central to every engagement.

Talk to One of Our Experts

Get in touch today to find out about how Evalueserve can help you improve your processes, making you better, faster and more efficient.

{kind=link}