Introduction

There is a global sprint towards reduction of carbon dioxide (CO2) emissions and greenhouse gases (GHG) across industries, in response to decarbonization needs outlined in the Net Zero 2050 goals as a part of the 2015 Paris Agreement. However, there are no immediate decarbonization remedies for emissions of certain types and from certain industries or in specific parts of their respective value chains. Carbon offsets have been developed to overcome this hurdle, wherein any individual, company, or government can purchase an emission reduction to compensate its carbon emissions made elsewhere.

These carbon offsets can be traded or transferred in marketplaces known as exchanges. These form the voluntary carbon markets (VCMs). VCMs are rapidly gaining traction as businesses realign their interests to better mitigate climate impact, meet investor and regulatory demands, as well as towards a more transparent move to decarbonisation. This is leading to investments and earmarking to the tune of billions of dollars in VCMs.

Carbon offset credit: It is a transferable emission reduction, certified by either government or independent certification bodies. Each unit represents an emission reduction equivalent to 1 metric tonne (Mt) of CO2 emissions, or other GHG emissions of equal value. In a VCM, the traded units are referred to as Carbon Credits – Voluntary Emission Reduction (VER). As against compliance market carbon credits which are only meant for large-scale emitters, credits in the VCM can be traded by any organization or individual who wishes to offset their emissions.

Carbon credit generation: Carbon credits are created by the work of project developers and organizations working with the aim to reduce, avoid, or remove GHG emissions from the planet’s atmosphere. These credits can then directly be purchased from said projects or traded through listings on VCMs. Purchasing these credits essentially leads to funding for the GHG emission mitigation activities of that project.

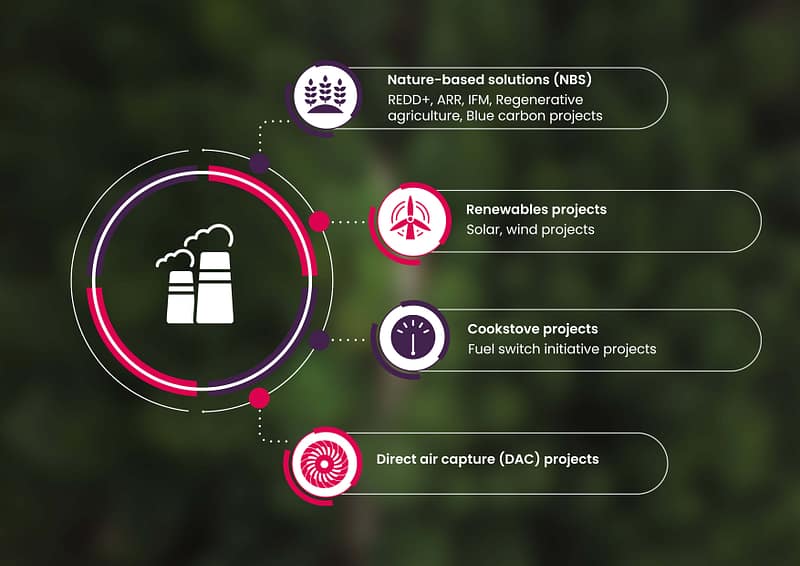

There are 2 broad categories of carbon credit projects – carbon avoidance or reduction projects as well as carbon removal or sequestration projects.

When a carbon credit is retired, it cannot be traded further and its impact goes towards compensating the GHG emissions of its owner, it becomes a carbon offset.

Project types for carbon offsets:

Voluntary carbon markets v/s compliance markets

Voluntary carbon markets, as their name suggests, are different from the compliance carbon markets (CCMs), which are mandatory and usually governed by national or regional law directing them to meet GHG emissions reduction mandates. CCM mandates usually fall under the Kyoto Protocol’s Clean Development Mechanism (CDM), Joint Implementation (JI) or Emission Trading Scheme (ETS). Whereas, in the VCM, emissions reductions are traded as a commodity and participants can buy and sell carbon offset credits voluntarily.

Key facts and figures

VCM demand drivers

With the above data, coupled with the wide adoption of decarbonization-aligned Environmental, Social, and Governance (ESG) performance goals by corporate entities globally, it is a no surprise that VCMs are witnessing an explosive growth trajectory. The same will continue to be case if we are to meet the annual, short-term, and long-term targets to reach Net Zero by 2050. Here are some key driving factors:

1

Rising pressure from stakeholders on organizations, corporations, asset managers, as well as governments on making and meeting Net Zero commitments.

2

Big players: A major chunk of the carbon credit demand so far has come from large organizations such as Microsoft, Google, Coca-Cola and the like making massive commitments. Their commitments to deep emission cuts in the short to medium-term cannot be met without use of carbon credits.

3

Increasing speculative activity in VCMs has also been noticed. This indicates that VCM participants have been buying credits with the intent to sell them for higher rates in the future.

4

High retirement rates of carbon credits to claim the offsets and a sudden surge in their buying have caused the inventory of voluntary carbon credits to diminish to some extent in recent years. This has only driven their demand higher.

Challenges ahead

With the above data, coupled with the wide adoption of decarbonization-aligned Environmental, Social, and Governance (ESG) performance goals by corporate entities globally, it is a no surprise that VCMs are witnessing an explosive growth trajectory. The same will continue to be case if we are to meet the annual, short-term, and long-term targets to reach Net Zero by 2050. Here are some key driving factors:

Credit prices rising is a challenge for carbon offset credits traded in VCMs. Amongst the most bought credit types in the demand explosion were energy project-based credits, which have historically been the cheapest to purchase, and have hence been taken up on priority. This is leading to more reliance from participants on NBS credits from agriculture, forestry and other land use (AFOLU) projects, which cost twice or more than energy ones.

Quality of carbon credits could be an offshoot challenge of the high demand low supply situation. Hence quality control of carbon credits will be a key factor to watch out for, as not all carbon credits may be created equal in a rapidly growing market. To keep up with the demand explosion, the quality of traded credits could get compromised to a degree.

Complexity and time required to develop projects that can issue high-quality credits to VCMs can also pose a challenge. Typically, carbon credits from a new project may take an average of 2-3 years to reach the market.

Lack of standardization needs to be addressed. There is no one singular standard for carbon credits. This means the quality and parameters to gauge carbon credits vary from region to region and market to market. Having a global standard would mean all VCM participants could access the same quality of carbon credits, with a measured and comparable environmental impact of each project and its credits.

Additionality is imperative to prove the legitimacy of carbon offset credits generation and issuance. This means that projects need to prove the carbon credits they are issuing are truly in addition to those that would have been created anyway by their project. So, they need to be clear that the credits were generated based on being incentivized from VCMs.

Overcoming challenges to grow

While there are a host of challenges to VCM participation, it is still early days for these markets. And a key mantra to success is getting there earlier than others. Various advantages to VCM participation at this stage or in the near future include the incentivisation of projects for carbon emissions reduction and removal from the atmosphere, increased transparency from participants reporting their carbon emissions reductions leading to increased accountability, as well the most important takeaway – reducing the global carbon footprint through a proactive and impactful approach.

Carbon Offset Platform: To tackle these challenges and gain all the advantages of participation in voluntary carbon markets, our team of experts at Evalueserve has developed our very own Carbon Offset Platform. This platform comprises a global database of projects from across various carbon offset registries, which helps you in analysing the best-fit project in terms of abatement as well as economics. To know more about how our Carbon Offset Platform can empower your decarbonisation journey, please connect with our team of experts today.

Get decarbonization publications delivered to your inbox by filling out the form below.