White Paper

Mining for Tomorrow: Digitization, Sustainability, and Strategy for a Net-Zero Era

Introduction

From the copper wiring in our homes to the lithium powering our phones, the mining industry is the backbone of modern civilization. Every road we drive on, every building we enter, and every device we hold in our hands exists because of the metals and minerals extracted from the earth. Yet, the story of mining is more than just digging deep into the ground—it’s a story of growth, innovation, and adaptation in a world that is constantly evolving.

For centuries, mining has fueled progress. It supplied the raw materials that built empires, powered industrial revolutions, and kickstarted the digital age. Today, the global mining industry is valued at over $2.1 trillion USD. The industry has experienced steady growth driven by increasing urbanization, industrialization, and demand for advanced technologies. As cities rise and industries evolve, the demand for iron ore, aluminum, and copper surges.

But the industry is undergoing a transformation. The world’s focus is shifting toward clean energy and sustainability, and with it, the demand for lithium, cobalt, and rare earth elements (REEs) has skyrocketed. These once-overlooked minerals are now the key to building a greener future, powering the batteries in electric vehicles, the magnets in wind turbines, and the circuits in solar panels. Mining is no longer just about extraction—it’s about unlocking the resources that will shape the next era of human progress.

Key Economies

As global demand for critical minerals shifts and surges, a handful of key economies dominate the mining sector.

China

Plays a dominant role, particularly in REEs and critical minerals. This stronghold gives them significant influence over global supply chains, especially in industries reliant on high-tech materials like semiconductors.

Has the largest zinc (Zn) reserves in the world and significant nickel (Ni), bauxite, cobalt (Co), copper (Cu), and lithium (Li) reserves. Industry giants like Rio Tinto and BHP are embracing AI by investing in automation, predictive analytics, and MLMs to enhance efficiency and lower costs.

Australia

Russia

Holds some of the world’s largest deposits of Ni, palladium (Pd), platinum (Pt), and uranium (U). Russia struggles with geopolitical tensions and economic sanctions but is actively strengthening ties with China and India to bypass Western restrictions and maintain its position as a key exporter.

The U.S. has a coal-dominated mining economy but also has strategic potash, iron ore, and Cu reserves. However, they have limited REE and critical minerals reserves. To bridge this gap, the U.S. is forming strategic alliances, especially with Saudi Arabia, to acquire Cu, Li, and Co assets in Africa.

United States

Saudi Arabia (KSA)

Mining is a cornerstone of its economic diversification strategy, aiming to reduce dependence on oil and gas while advancing its net-zero ambitions. Over the next decade, it plans to bring numerous mining sites into production, extracting essential minerals to fuel the transition to a green economy.

Home to 561 operational mines as of January 2025 and is the largest producer of Pt and has the largest reserves of manganese (Mn), chromite (Cr), and platinum-group metals. However, illegal mining threatens both economic stability and environmental sustainability.

South Africa

Deep Sea Mining for Critical Minerals

Deep-sea mining, a nascent yet contentious sector, is experiencing a surge in interest due to the escalating global demand for critical minerals. Specifically, the rising market of electric vehicles (EVs) and renewable energy industries require substantial quantities of cobalt, nickel, manganese, and rare earth elements, all of which are found in abundance within deep-sea mineral deposits. For instance, polymetallic nodules, scattered across vast abyssal plains, are estimated to contain billions of tons of these valuable metals. Cobalt-rich ferromanganese crusts, found on seamounts, and polymetallic sulfides, formed at hydrothermal vents, offer additional significant reserves. Currently, the industry remains primarily in the exploratory phase, with the International Seabed Authority (ISA), under the United Nations Convention on the Law of the Sea (UNCLOS), playing a pivotal role in drafting regulations for future commercial exploitation. The ISA has issued numerous exploration contracts, covering millions of square kilometers of seabed. The future of deep-sea mining rests on the precarious balance between securing vital resources and safeguarding the marine environment. The development of robust environmental impact assessments, the implementation of stringent monitoring protocols, and the adoption of innovative, less invasive mining technologies are paramount.

The Digital Transformation of Mining

For decades, the Metals and Mining sector relied on traditional methods, trailing behind other industries in adopting Industry 4.0 technologies—but that is rapidly changing. With the advent of sophisticated digital technologies, mining companies are reimagining their operations. Generative AI, IoT-powered sensors, automated robots, and blockchain technology lead this change. These advancements are not just enhancing operational efficiency and productivity but are creating safer and more sustainable mining ecosystems.

Global Leaders Pioneering Mining Automation

Top mining nations like Australia and Canada are rapidly deploying autonomous mining fleets to reduce human deployment at mine sites. They have been investing in advanced HEMMs such as Automated Drilling rigs (ADRs) and Autonomous Hauling Systems (AHSs). Coupled with next generation, multimedia technologies, these HEMMs ensure continuous remote monitoring, enhanced safety, and reduced emissions.

Meanwhile, in India and Saudi Arabia, the focus is on digitalization. These economies are heavily investing in the digitization of geological repositories and the implementation of advanced mining planning software. With these data analysis tools and 3D modeling, mining companies can consolidate and analyze geological data while assessing risks, generating production schedules, and optimizing mine designs. Digitization also ensures seamless knowledge-sharing among stakeholders and easy access to data for investors.

AI in Mining Industry

In the coming decade, miners across geographies will increasingly adopt advanced technologies across all their sites as regulatory requirements become more stringent. This accelerating shift toward automation and AI-driven decision-making will propel the mining automation market to grow at a CAGR of approximately 6.40%, reaching USD 7.5 billion by 2034.

Here are a few use cases for AI in the mining industry.

- Create production schedules that maximize asset utilization and energy efficiency for improved operations.

- Monitor and assess emerging technologies to support informed decarbonization strategies and future sustainability initiatives.

- Deploy predictive maintenance programs that leverage early fault detection to prevent performance decline and reduce downtime

- Analyze policy and regulatory shifts to proactively assess their potential impact on development and operational strategies.

Forging a Sustainable Future: The Mining and Metals Sector’s Journey Toward Net-Zero

The mining industry contributes to 7-8% of global greenhouse gas (GHG) emissions and has long been regarded as a hard-to-abate industry. As stakeholders—including governments, investors, and consumers—become increasingly conscious of climate change's negative impacts, more organizations focus on sourcing sustainable products from responsible miners and metal manufacturers.

However, the paradox is clear: while mining is often criticized for its environmental impact, it is also indispensable for the net-zero transition. Critical minerals and REEs, like lithium and cobalt, are essential for renewable energy infrastructure, electric vehicles, and battery storage systems.

Mining’s Path to a Greener Future

In accordance with the Paris Agreement, which aims to limit global warming to below 2°C—and ideally within 1.5°C—above pre-industrial levels, mining companies are accelerating their shift toward renewable energy. Across the globe, mines are integrating long-duration Battey Energy Storage Systems (BESS) connected to renewable grids, ensuring a stable and sustainable power supply that reduces emissions and enhances the mine’s productivity. Many companies are also investing in Carbon Capture, Utilization, and Storage (CCUS) technologies to offset emissions.

Sustainable Metals Manufacturing

On the production front, metals manufacturers are moving away from relying on virgin ores and towards adopting the 3R principles—Reduce, Reuse, and Recycle—to minimize waste and emissions. Steel and aluminum manufacturers are taking bold steps to cut Scope 1 and Scope 2 emissions by incorporating recycled scraps into their charge mix.

The impact is already visible.

- In 2021, around 400 million tons of steel scrap were recycled and used instead of iron ore and coke.

- In 2024, aluminum smelters globally consumed more than 30 million tons of recycled metal.

- By 2050, 50-60% of global aluminum production is projected to come from recycled sources.

According to Project Drawdown, this shift in material sources could result in a 5.05-6.02 gigaton reduction in carbon emissions, a significant contribution to global decarbonization efforts.

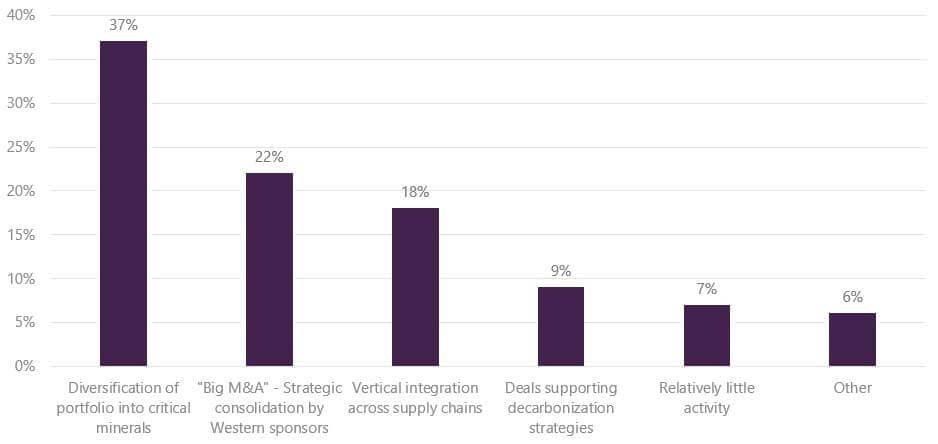

The Surge in Mining Mergers: How Consolidation is Shaping the Future of the Industry

The mining industry has long been fragmented, with large corporations and smaller specialized firms coexisting, offering varied services across geology, mineral extraction, and processing. However, the landscape is rapidly shifting as the industry faces rising costs, tighter ESG regulations, fluctuating commodity prices, and scarce investment. Mergers and acquisitions have become a strategic necessity to stay relevant in the industry. As a result, larger mining giants increasingly absorb smaller firms with niche capabilities, specialized knowledge, advanced technologies, and a highly skilled workforce.

In 2024 alone, 30 mergers with $2.43 billion were announced, indicating a 4% year-on-year increase in acquisitions. This acceleration in deals is not just about financial growth; it is about securing untapped resources, complying with regional laws, strengthening sustainability commitments, sharing workforces, and leveraging technological innovations to streamline extraction and processing. Furthermore, more consolidation is expected in mining and metals operations in the coming decade. Four primary factors drive this:

-

Business Re-invention

-

Strategic Mineral Exploration & Extraction

-

Sustainability

-

Partnerships

Policy-Level Interventions: Navigating the Geopolitical Shifts in Mining

In 2024, geopolitics deeply affected the metals and mining sector, leading to fragmented supply chains, resource nationalism, and tariff imposition. Furthermore, China’s dominance – controlling nearly 70% of the world’s critical mineral extraction and processing – has become a growing concern for global economics. This concentration of power presents a significant strategic vulnerability, especially considering past actions such as sudden export bans. In response, major economies like the US, KSA, and India are investing more in domestic geological exploration activities of strategically essential minerals.

But the stakes are even higher. The gap between supply and demand for seven critical minerals – lithium, cobalt, copper, nickel, neodymium, graphite, and rare earth – threatens to derail the world’s clean energy ambitions. This gap will increase 1.5 to 7 times by 2032 under the Net Zero Emissions (NZE) scenario.

Governments are responding urgently, with policymakers around the world crafting incentive-rich frameworks to pour investment into new mining projects. Capital infusion strategies, fast-tracked environmental clearances, land allotment reforms, and streamlined acquisition processes are expected to accelerate the timeline from exploration to production. The goal is clear: bring more mines online faster—but also responsibly.

At the same time, the mining industry must clean up its act. Many key players in the sector favor introducing a carbon tax to incentivize the shift towards less carbon-intensive fuels, deployment of energy efficiency measures, and investment in clean alternatives across the entire value chain. Yet, this proposed shift might make smaller players more vulnerable. For them, carbon taxes could mean thinner margins, higher costs, and the risk of being pushed out of the market. Balancing the drive for decarbonization with the need to maintain a competitive and inclusive industry will be one of the mining sector’s most pressing challenges in the years to come.

Streamlining Mining Approvals

For years, mining approvals have been bogged down by bureaucratic delays, environmental regulations, and slow permitting processes, significantly affecting the pace of exploration. Some countries, like Canada and Brazil, boast efficient approval frameworks, granting mining clearances in 1-2 months. In contrast, India faces one of the longest approval timelines, exceeding 5 years, causing project stagnation and investor hesitation. To address these inefficiencies, many nations are exploring a "single-window clearance" system, ensuring that all necessary permits and approvals are granted within a fixed timeframe. This policy shift would:

- Reduce the time and complexity of obtaining exploration licenses and mining leases.

- Encourage faster deployment of resources by eliminating unnecessary administrative bottlenecks.

- Attract foreign investment by creating a more transparent and predictable regulatory environment.

By implementing fast-track approval mechanisms, mining nations can accelerate exploration, unlock new reserves, and maintain their competitive edge in the global mineral supply chain.

Financing the Future

Mining exploration and extraction are capital-intensive, requiring significant upfront investments before operations become profitable. However, given the role of critical minerals and REEs in achieving net-zero goals, global financial institutions and policymakers are taking proactive steps to fund sustainable mining initiatives.

- Special funding allocations by international financing bodies—targeting exploration of essential minerals for green technologies, EV batteries, and renewable energy storage.

- Crowdsourced equity funding, which has been legislated in Australia since 2017 but has now been fully enacted, could allow smaller mining firms and startups to access capital without relying solely on institutional investors.

- Incentives for sustainable mining—governments may introduce tax breaks, subsidies, and investment incentives for companies implementing low-carbon extraction technologies.

How Evalueserve Can Help

At Evalueserve, we are committed to helping mining companies navigate this evolving landscape with data-driven insights, AI-powered analytics, and strategic advisory services. Our expertise spans the entire mining value chain—from resource exploration and operational optimization to digital transformation and policy alignment.

Contact us today to speak with an expert at Evalueserve and discover how we can help your mining company unlock new opportunities, drive efficiency, and achieve sustainable growth.

About the Authors

Jyotirmoy Saha

Consultant - Insights & Advisory

Tamal Roy

Principal Consultant - Insights & Advisory

Talk to One of Our Experts

Get in touch today to find out about how Evalueserve can help you improve your processes, making you better, faster and more efficient.