A Federal Dilemma ꟷ Product of a “three-front” war on inflation

March 6, 2023

It has been over a year since the start of the Russia-Ukraine war and the Fed’s rate-hiking cycle that kicked off in March last year[1]. As the war continues unabated, the hikes have come down by a quarter percentage point from the previous increase in December and are 50bps lower than the first six successive three-quarter point increases. The Fed raised the benchmark rate during the February FOMC meeting by 25bps, bringing the target rate to 4.50‑4.75%, the highest range since October 2007. The Fed also announced “ongoing increases[2]”, pushing back against market expectations[3] that rate cuts will begin as inflation softens in the final few months of the year; however, inflation is still hovering around its highest level since the early 1980s. Markets anticipate another 25bp hike in March, followed by two more quarter percentage point increases in May and June this year[4].

Combating inflation through monetary policy…

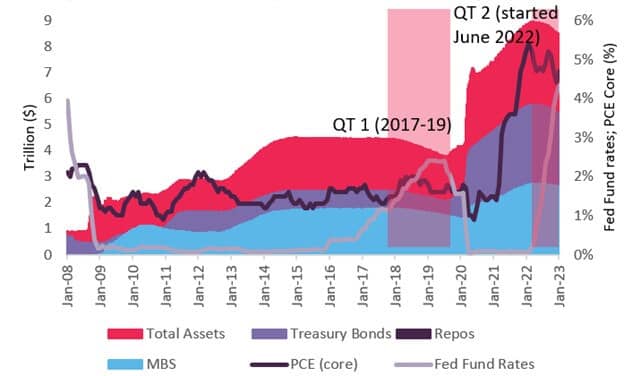

The US Federal Reserve has already increased its benchmark rate by a cumulative 4.50% since the start of the rate-hiking cycle. It has reduced its asset portfolio by $445bn since June 2022 as part of its balance sheet runoffs (see figure 1). The Fed’s balance sheet level has fallen to ~$8.47tn from a record ~$9tn in June 2022 after the Fed introduced a bond-buying program at the onset of the COVID-19 pandemic, leading to excessive liquidity and high inflation. Although these measures have helped cool down core inflation to 4.7% in January from a 40-year high of 5.4% in early 2022, it is still significantly above the Fed’s 2.0% long‑term target. We expect quantitative tightening (QT) to last until 2024; however, the Fed may slow the runoffs once bank reserves fall to around 10-11% of GDP[5]. We also foresee an early end to QT if the reserves drop to a limit that starts draining liquidity out of the market, which happened during QT1 in 2018-19. Although the Fed has already set up a standing repo facility to maintain liquidity during a crunch, there is always the risk of an equity sell-off or an overshoot of overnight financing rates under these scenarios.

Figure 1: The Fed has reduced its balance sheet by ~$445bn since June 2022

Description: The Fed has reduced its balance sheet (as shown on the primary y-axis) by $445bn ($95bn/month) since June 2022 and has raised the rates eight times (Fed Fund rates and PCE as shown on the secondary y-axis) since the hiking cycle that began in March 2022, tightening liquidity in the market through the utilization of every monetary tool at its disposal. Source: Fred.stlouisfed.org

…and legislative tools (Inflation Reduction Act[6], 2022)

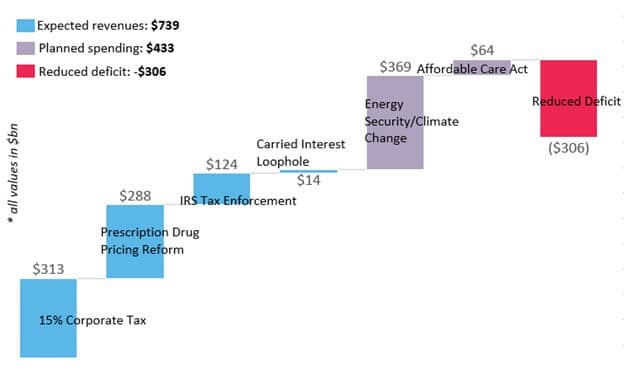

The Biden administration signed the Inflation Reduction Act into law in August last year, which aims to reduce the fiscal deficit by more than $300bn over a period of ten years by investing $433bn in energy security, climate change, and affordable healthcare (see figure 2). A record $369bn would be spent on energy and climate change, which should lead to a boost in domestic output and reduction of carbon emissions of about 40% by 2030. Another $64bn would go toward subsidies that would lower the insurance premium costs for families covered under the Affordable Care Act[7].

The bill is estimated to raise $739bn in revenues over the next ten years through corporate tax and prescription drug pricing reforms and by funding the Internal Revenue Service (IRS) tax enforcement policies. The legislation seeks a 15% minimum tax[8] on corporations with revenues in excess of $1bn/yr and expects to bring in $313bn over the next decade. The bill also provides for $80bn in funding to the IRS that would help the agency crack down on fraudulent tax practices and potentially generate $124bn in revenues over the same period. Another key provision of the bill allows Medicare to negotiate prescription drug prices, which is estimated to result in about $288bn in revenues in the form of savings. Lastly, the bill attempts to close loopholes by implementing a tax rate of up to 37% on compensation that asset managers receive for managing their clients’ portfolios. The measures are expected to raise $14bn over the next ten years. However, there has also been debate on the legislation’s impact on inflation, with the University of Pennsylvania’s Penn Wharton Budget Model[9] concluding that over the next decade “the impact on inflation is statistically indistinguishable from zero and that the act would reduce non-interest cumulative deficits by only $264 billion over the budget window“.

Figure 2: The Inflation Reduction Act (IRA) aims to reduce the deficit by more than $300bn over the next ten years

Description: The IRA signed into law in August 2022 directs $433bn in federal spending with a goal of generating revenues of ~$739bn, targeting more than $300bn in deficit reduction over a period of ten years. Source: Democrats.Senate.Gov

The Dilemma

The US Federal Reserve has been on a hiking spree to contain inflation since March last year and has been reducing its reserves by about $95bn/month, causing the fiscal deficit to rise, which is not in line with the objective of the IRA that aims to reduce inflation by shrinking the total deficit. Over the past 11 years, the US Federal Reserve had made on average $4-12bn a month that it accumulated through Interest Payments from the Securities Portfolio (IPSP). The Fed’s expense primarily comes from Reverse Repurchase agreements and reserve balances rates and since last year both of these rates have been above the average coupon of total SOMA (System Open Market Account) holdings, as a consequence of consecutive rate hikes. The benchmark rates had largely been below the IPSP, especially after the financial crisis of 2008 and the arrival of COVID-19 pandemic when they were cut down to 0.25% in March 2020. A larger IPSP/fed fund spread meant the central bank was paying a small amount of interest to financial entities that parked their cash at the Federal Reserve, while it was making more money on its own assets through interest that traded at large premiums to the benchmark rates. The Fed had been passing this surplus to the Department of Treasury (DoT), thus keeping

its borrowing needs in check. Now that interest rates have been raised to 4.5-4.75% (higher than the current IPSP rate), the Fed’s earnings have evaporated, leaving a substantial deficit that is contrary to the provisions under the IRA.

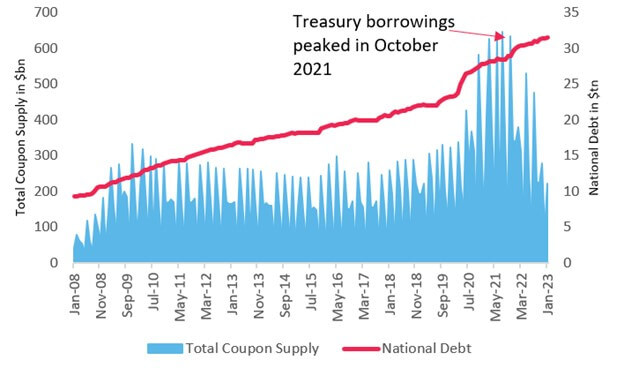

The Treasury would be forced to fund this deficit by raising more debt on the capital markets. Under the prevailing conditions, this would not be possible, as the US already breached the $31.4tn debt ceiling in January 2023[10] after the Treasury was forced to raise auction sizes across all maturities during the financial crisis in 2008-09 and in response to the COVID-19 pandemic (see figure 3). However, total borrowing had peaked in October 2021 and has since fallen before stabilizing in September 2022. It is also worth noting that the debt-to-GDP ratio was 97%[11] at the end of the fiscal year ending September 2022. Going by current assumptions, the ratio would rise to about 100% in 2025 before surging to ~200% by 2046 and ~566% by 2097, implying the current policy is not sustainable while underscoring the need for fiscal prudence adopted by the Treasury and legislative measures put in place to control the deficit.

Figure 3: Total public debt reaches record high as borrowings stabilize after peaking in October 2021

*Treasury Notes and Bonds with maturities ranging from 2 years to 30 years only have been shown as total coupon supply.

Description: The US public debt has hit a record $31.4tn (as shown on the secondary y-axis) fueled by increased government borrowings (as shown on the primary y-axis), following the 2007-08 financial crisis and fiscal response to the Covid-19 pandemic. After reaching its peak in October 2021, government borrowings fell before stabilizing in September 2022. Source: US Treasury Department and FiscalData.Treasury.gov

Mending the ceiling through extraordinary measures

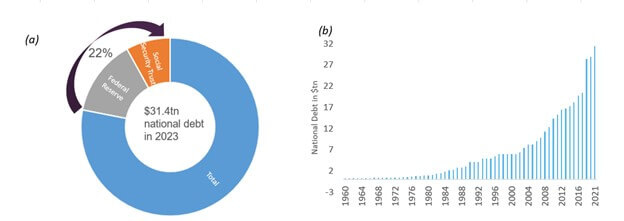

Of the total $31.4tn national debt, the government owes itself about one-quarter (22% to be precise) through Federal Reserve Treasury holdings and social security trust funds, such as retirement, health, and other trust funds (see figure 4-a). The Treasury has already invoked extraordinary measures[12] including redeeming investments from the Civil Service Retirement and Disability Fund and the Postal Service Retiree Health Benefits Fund from January 19th. On January 23rd, the DoT introduced additional measures[13] such as pausing investment in the Government Securities Investment Fund, which is invested in short-term US Treasury securities and issued to the Thrift Savings Plan.

By suspending reinvestments and selling existing investments from these funds, the Treasury expects to temporarily continue paying its debt obligations. However, Treasury Secretary Janet Yellen has cautioned that the extraordinary measures could allow the government to pay its bills only until June 5 and that the only way forward would be to increase the debt ceiling. The debt ceiling has been either raised, temporarily extended, or revised 78 times since 1960 – 49 times under Republicans and 29 times under Democrats (see figure 4-b). Voices have already emerged from different quarters on eliminating the statutory limit altogether given that it is put to vote in Congress each time the country overshoots the borrowing limit and a stalemate to reach an agreement sometimes results in dire financial consequences. However, during a press conference[14] last year, President Biden ruled out scrapping the debt limit, calling the move “irresponsible”. The debt ceiling was last raised in December 2021 by $2.5tn to $31.4tn.

Figure 4: (a) The US govt. owes itself 22% of the total debt; (b) Historical debt ceilings

Description: (a) About one-quarter of $31.4tn total debt the government owes itself through Social Security Trust and Federal Reserve Treasury holdings. (b) The Debt ceiling has been either raised, temporarily extended, or revised 78 times since 1960. Source: FiscalData.Treasury.Gov and USAFACTS.org

Direct fallout: The default scare and partial shutdowns

The United States has never defaulted on its debt obligations, but this time, it looks dangerously close to the X Date[15]. The debt ceiling was last raised in December 2021 when Democrats controlled both the House and the Senate; however, the dynamics have changed after the current administration lost the House of Representatives to Republicans in the 2022 midterm elections. House Speaker Kevin McCarthy has called for first implementing large spending cuts[16] before committing anything on lifting the cap on government borrowings. “We must commit to finding common ground on a responsible debt limit increase. Finding compromise is exactly how governing in America is supposed to work, and exactly what the American people voted for just three months ago,” McCarthy said. If the US defaults, it would send shockwaves across the financial markets and rattle investors’ confidence in its economy. The last time the US came close to a default was during the 2011 debt ceiling crisis, which saw a large market sell-off and its first-ever AAA rating downgrade[17] by the S&P.

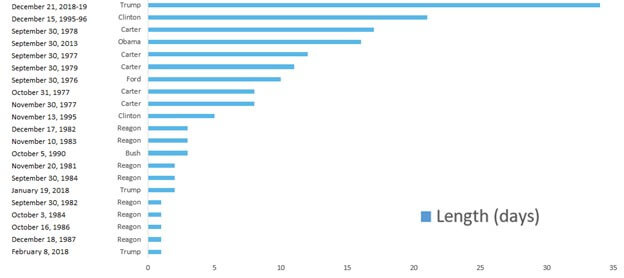

The extraordinary measures currently in place would allow the government to meet its debt obligations only until early June. A failure to lift or temporarily suspend the debt limit after that date would limit the government’s ability to pay its bills while certain government agencies may also be forced to shut down. There have been 21 government shutdowns in the past, with the most recent in 2018-19 being the largest, lasting for 34 days over a deadlock to fund the $5bn border wall under the Trump administration (see figure 5). We also expect the delays in reaching a consensus on the debt limit to put downward pressure on the US dollar, with borrowing costs potentially rising in the form of high interest rates on mortgages, credit cards, and other bank loans.

Figure 5: Length of historical government shutdowns in days

Description: There have been 21 government shutdowns in the past. The most recent was the largest under the Trump administration and involved a deadlock over funding of a border wall that continued for 34 days, leading various sectors of the government to close temporarily. Source: History, Art & Archives

Conclusion: Aligned… yet at odds

The battle to combat inflation is being fought on three different fronts ꟷ the US Federal Reserve, the Treasury and the government. The Fed has raised interest rates eight times (by a cumulative 4.50%) since the beginning of the hiking cycle in March 2022 to tame core inflation, which eased to 4.7% in January but is still at an early-1980 level high. In addition to the increase in rates, the Fed has also been shrinking its balance sheet, assets of which have fallen by ~$445bn since June 2022. Lower reserve levels would tighten liquidity in the market, which in turn would help control inflation. The Fed, on average, has made $4-12bn/month through interest payments from the securities portfolio over the past 11 years, which it passed on to the Treasury, thus keeping its borrowings needs smaller. Falling reserves would influence its proceeds to a certain extent, but nothing that comes close to the rate hikes that would have a devastating impact on the central bank’s earnings. The Federal Reserve has been paying less in interest, as benchmark rates have largely been near-zero (0.25%) for a long time (110 months since December 2008), while it has been making more on its reserves through IPSP. The benchmark rates have now risen to 4.75%, higher than the average coupon of total SOMA holdings, leading to the proceeds that the central bank was passing on to the Treasury to completely run dry, resulting in a significant deficit.

This deficit goes against the fiscal prudence that the Treasury has assumed lately, as any additional deficit is usually funded through increases in auction sizes. The DoT has reduced auction sizes across all maturities after they peaked in October 2021. The country has already hit its borrowing limit of $31.4tn in January this year, meaning the department is in no position to issue additional debt. The Treasury has already invoked extraordinary measures that would allow the government to pay its bills until early June; however, once these emergency steps are exhausted, Congress would have to either lift or temporarily suspend the borrowing limit. Failure to do so could have substantial financial consequences, such as partial shutdowns or even a first-ever default. A deadlock over the debt limit could also affect the country’s sovereign ratings.

The government also finds itself at odds with federal monetary policy, as lawmakers have voted to enact the Inflation Reduction Act, which aims to combat inflation by reducing the fiscal deficit by more than $300bn over the next 10 years.

References

[1] Please read our blog All Eyes on the Fed as the March FOMC Meeting Draws Closer (published in March 2022) to find out more on the Fed hiking cycle.

[2] Read the complete press release (FOMC February statement)

[3] Fed’s words in focus as markets bet rate hikes will soon end (Reuters)

[4] BoA have added in another FOMC rate hike, now see March, May and June +25bp at each (Forexlive)

[5] Fed officials see lots of room to shed bonds from balance sheet (Reuters)

[6] Inflation Reduction Act, 2022 (Congress.gov)

[7] Affordable Care Act, 2010 (HHS.gov)

[8] Please read our blog Eyeing the Global Commitment in Biden’s Made in America Tax Plan (published in July 2021) to find out more on the 15% minimum corporate tax.

[9] Senate-Passed Inflation Reduction Act: Estimates of Budgetary and Macroeconomic Effects (PWBM)

[10] U.S. hits debt ceiling as partisan standoff sparks economic worries (Reuters)

[11] US Financial Report FY 2022 (Treasury.gov)

[12] Yellen says Treasury is taking extraordinary measures to avoid default as U.S. hits debt limit (CNBC)

[13] Treasury takes more extraordinary measures to avoid debt default (CNN)

[14] Biden rules out eliminating the debt ceiling (Politico)

[15] “X Date” — is the day when the US government would be unable to meet its financial obligations

[16] McCarthy calls on Biden to accept spending cuts in debt ceiling fight (The Guardian)