The cruise industry is recovering at the fastest pace on record as customer demand continues to stay strong. At the end of FY23, the three largest (top 3) publicly listed companies in the industry [Carnival Cruise (CCL), Royal Caribbean (RCL), and Norwegian Cruise (NCLH)], which account for ~70% of the total capacity, reported stellar operating metrics and record revenues. All companies cited extremely strong customer demand and record pricing as revenge travel continues unabated. While retail companies in the US have started talking about inflation putting pressure on the wallets of customers, the cruise industry continues to see a very positive customer sentiment and expects growth to continue in FY24.

Bookings, a leading indicator of near-term demand, are at the highest record and exceed the levels witnessed by the three largest companies before the pandemic in 2019. This unforeseen and seemingly unabating demand has pleasantly surprised industry veterans and investors, especially after the pandemic, and ravaged the cruise industry.

A Pandemic that Shut Down Industry Overnight

The COVID-19 pandemic had a devastating impact on the cruise industry, as stay-in-place orders were issued, and bookings were canceled. Sailings across the globe were canceled overnight as companies arranged to transport stranded customers from various locations. As bookings were canceled, cruise companies introduced future cruise credits (FCCs) to conserve cash by allowing customers to opt for FCCs instead of cash refunds. These credits allowed customers to cruise in the future when sailings resumed.

Cruise companies borrowed heavily during the COVID-19 outbreak to fund operations as cash flows became negative with fixed expenses. Employees were furloughed, government assistance funds were tapped, and financial covenants were waived by banks, export credit agencies, and other lenders. Passengers carried in the month, following stay-in-place restrictions, ground to a halt.

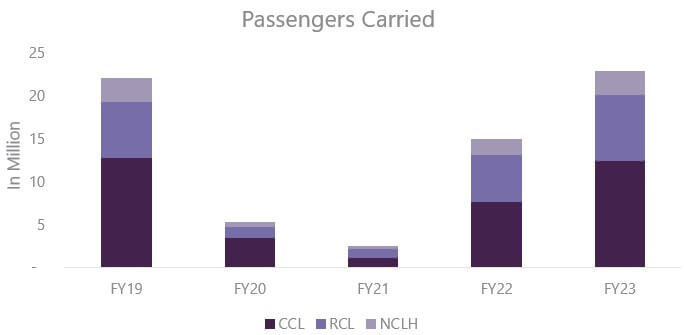

Initially, the recovery was expected within a few months; however, the horror of the pandemic and an uneven global vaccination program stalled the recovery. Passengers carried on a combined basis for the three companies only began recovering meaningfully in mid-2022 and eclipsed its FY19 record in FY23.

Most companies had to borrow hand over fist to sustain operations. As ships were docked, companies raised cash at exceptionally high rates to sustain operations. With continuing uncertainty about a full-scale reopening in late FY20 and in 1H21, companies deferred re-opening plans many times to their dismay.

With customers locked in their homes and anticipated high borrowings by companies to sustain operations, credit rating agencies downgraded credit ratings of the top three companies to many notches below their prior ratings. Total debt for the three companies combined almost doubled in a year and kept rising until FY22 before declining 8% YoY in FY23 as companies began generating positive cash flow and sailing normalcy was restored.

A Sea Change – The Recovery

As vaccination rates improved across the globe and rapid result tests were introduced, the COVID-19 threat began to abate, and cruise companies embarked on a full-fledged reopening. The industry had been preparing for a return to normal sailings for over 18 months now, and gradually, customers started returning.

Since demand was stronger than anticipated, especially in North America, cash flow from operations allowed companies to reduce cash burn. While average occupancy is yet to exceed 2019 levels, an expected strong demand environment in FY24 should allow companies to eclipse the occupancy levels reached prior to the pandemic. Average occupancy for the three companies combined reached 103% in FY23, driven by a robust demand environment, which was partially offset by capacity growth.

Pricing also improved more than anticipated, and companies revised guidance upwards, driven by a strong pricing environment and, consequently, higher yields. Revenue and profitability expectations continued to surprise on the upside, driven by strong demand as people continued to travel on their dream vacations and spend at elevated levels.

As spending on goods slows in the US, consumers continue to spend on experiences. They are highly engaged with their respective cruise brands. They are planning and booking their vacations earlier than usual, including advance bookings for on-board activities. Consumers have also increased on-board spending, compared with the pre-pandemic period.

Growth and Profitability Drivers of Industry in FY23

Although guest loyalty was the initial driver in the past, the cruise industry continues to add new guests to its vacation ecosystem and widen its customer base. Stronger-than-expected demand and return to profitability are also driving capacity growth in the Industry, which slowed during the pandemic years but picked up thereafter. The industry continues to add capacity over the next couple of years and expects to grow capacity in mid-single digits, as both new and repeat customers continue to find more value in cruise vacations than their land-based counterparts.

Source: Cruise Industry News (via CCL- 10K)

Outlook

FY23 was a banner year for the industry, as the demand outlook continued to stay robust. On a combined basis, the three companies expect continued upward momentum in occupancy, mid-to-high single-digit yield growth, moderate capacity additions, and strong cost controls. These factors are expected to drive continued earnings growth and allow companies to further improve profitability and generate free cash flow. The additional cash flow will be used to pay down debt and strengthen their balance sheets over the next couple of years.

Additionally, bookings continue to remain at an all-time high with higher prices than in FY23, driven by a record wave season. Booking channels, both direct and indirect, are exceeding expectations as companies broke prior records in the two weeks around Black Friday and Cyber Monday. Customer deposits (advances received against tickets) increased 25% YoY in FY23 and were up 43% compared with the peak registered in 2019.

Back to Growth – Conclusion

Stronger bookings and higher pricing in FY24 than in FY23 indicate robust demand for cruise travel. The industry is expected to continue remaining on the growth path, primarily driven by a growing appetite for cruising and the value that it offers compared with land-based alternatives.

At present, the debt levels are higher than normal, with deleveraging already underway. Companies are expected to deleverage over the next couple of years and retain their pre-pandemic credit ratings. Driven by robust demand, ongoing cost control initiatives, moderate capacity growth that focuses on profitability, and free cash flow generation, the industry is poised to put in rear view a once-in-a-century aberration that knocked it down in March 2020.

How can Evalueserve help?

Evalueserve is a leading provider of investment research services to global asset and wealth management firms. We cater to clients across asset classes and offer equity and fixed-income research support. Our services include undertaking economic and financial modeling, conducting in-depth company analysis, and developing industry trend reports. We leverage the latest technologies, including GenAI, and human expertise to provide actionable insights that help our clients improve efficiency and save time that they can use to focus on other high-value activities.

Talk to One of Our Experts

Get in touch today to find out about how Evalueserve can help you improve your processes, making you better, faster and more efficient.