Market Sentiments and Outlook for PE Consulting Firms

Private equity is not rebounding; it is resetting.

After two years of valuation compression, capital-market volatility, and delayed exits, deal activity returned in 2025 with force, but not with familiarity. Q1 2026 data confirms that capital is flowing again, yet it is being deployed into fewer, larger, and higher conviction transactions. For PE firms, the rules have changed.

For PE advisors and consulting firms, the shift is even more consequential.

This is a market that rewards discipline, depth, and execution, not volume.

By early 2026, PE sentiment has moved from uncertainty to measured optimism.

Financing conditions have stabilized in Q1, supported by lower volatility, easing inflation pressures, and buyers and sellers have largely realigned on pricing. Deal value surged in 2025, exits reopened selectively, and megadeals returned to the market.

Global PE deal value reached ~USD 436B in Q1 2026 across ~4,168 deals, while rolling 12-month investment totals softened marginally from ~USD 2.2T to ~USD 2.1T, reflecting continued selectivity rather than retrenchment. But risk appetite has not broadly returned. Instead, sponsors have become decisive but selective.

"Tariff turmoil froze activity in spring 2025. Deals resumed, but only where sponsors had the clearest line of sight on value creation and exit."

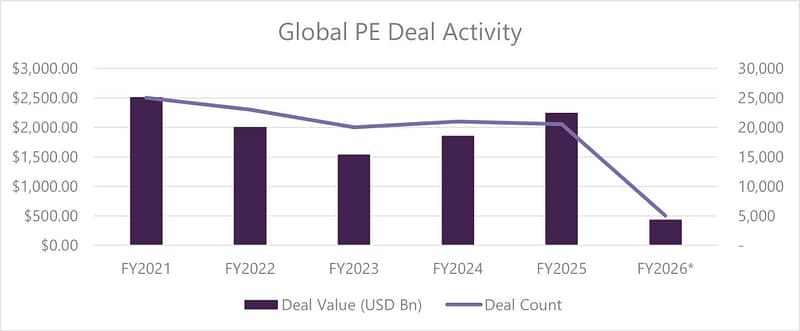

What the Data Signals: A Market of Fewer, Bigger, Higher Conviction Deals

The chart reinforces three critical shifts shaping Q1 2026:

- First, the market has structurally moved toward scale - Deal value recovery post-2023 is being driven by a relatively small number of large transactions, including multi-billiondollar take privates and infrastructure led deals.

- Second, deal volume contraction reflects rising selectivity, not weak demand - Private equity firms are sitting on significant dry powder but are deploying capital selectively, prioritizing assets with clear value creation pathways, resilience, and strategic relevance.

- Third, capital is increasingly concentrated in high-conviction thematic plays - Q1 2026 activity is dominated by sectors linked to AI, energy, infrastructure, and asset-backed platforms, signalling a strong tilt toward long duration, scalable, and tech-enabled business models.

This phenomenon has directly elevated the role of advisors. Sponsors prioritized fewer, larger, and more conviction-driven opportunities, with volume increasing a measured 15% even as deal value surged 57% year-on-year. The USD 56.6 billion Electronic Arts take private - the largest buyout in history - exemplified the willingness of well-capitalized sponsors to act at scale when conviction is high

Sector Selectivity

Capital in 2025–26 has flowed decisively toward sectors where operational differentiation and scale advantages are achievable

Deal activity in Q1 2026 is heavily concentrated in technology, with more selective but steady investment in industrials and healthcare, while capital deployment remains limited in consumer and BFSI sectors and continues to favour scalable, operationally differentiated opportunities.

Deal activity across industry verticals in Q1 2026 is highly concentrated in AI at 20% and manufacturing-led segments (19%), with cloud computing also maintaining a meaningful share of 15%, while consumer-facing and fintech-driven categories such as mobile apps, health-tech, and fintech see comparatively lower activity, indicating that capital is increasingly being directed toward scalable, infrastructure driven, and capability enabling technologies rather than end market applications.

The data suggests buyout capital has remained structurally more resilient, rising about 30% from FY2021 before easing slightly in FY2026*, while growth capital is only about 8% above FY2021 and has declined for three consecutive years after peaking in FY2023. For PE consulting teams, this reinforces the need to support clients with sharper valuation work, more robust downside scenarios, and value-creation plans that can withstand a slower exit market.

For advisors, this has increased the premium on sector depth and expanded the scope of work PE clients expect across the deal cycle. In addition to recognizing patterns across past deals and benchmarking on PE relevant metrics, advisors are increasingly expected to support:

- Commercial and financial diligence: commercial due diligence, market sizing, financial due diligence, and quality-of-earnings analysis.

- Operational and synergy assessment: operational due diligence, synergy review, and carve-out or standalone operating model assessment.

- Value creation and performance improvement: value creation planning, 100-day planning, portfolio benchmarking, KPI design, and working capital or cash-flow improvement.

- Growth and margin optimization: pricing, margin, and cost-transformation diagnostics, along with go-to-market and revenue-growth strategy.

- Exit and broader strategic support: exit readiness, sell-side support, equity story development, supply chain and procurement optimization, and ESG/sustainability diligence where relevant.

Uneven Recovery Across Geographies

Geographic divergence became even clearer in early 2026.

- North America: Accounted for the majority of Q1 value, with PE exit and deal activity proving resilient despite geopolitical noise. Exit value reached ~USD 307B across ~975 exits in Q1, heavily skewed by large sponsor‑to‑sponsor and strategic transactions. Canada and Latin America both showed resilience in PE investment despite lower deal count.

- Europe: Continued its cautious rebound. Financing availability improved, but deal pacing remained methodical. Carve‑outs and secondary buyouts dominated.

- Middle East: Geopolitical tensions linked to the Middle East led to a pause in deal activity and increased caution

- APAC: Momentum across the region was mixed in Q1 2026, with select Southeast Asian markets, meanwhile, stayed comparatively resilient, supported by growth diligence, new platform formation, and operating model work.

For consulting firms, regional specialization now directly shapes revenue opportunity, not just delivery complexity.

For consulting firms, this creates region‑specific opportunity:

- Carve‑out and cross‑border diligence in Europe and Japan

- Deep operational value creation in North America, where scale amplifies impact

- Increasingly, global sponsors expect partners who can deliver consistent insight and execution across regions, enabled by data, technology, and scalable delivery models

Exit and Financing: Liquidity Is Back - but Selectively

Uneven Recovery Across Geographies

Global PE exit activity softened in Q1 2026, with exit value at ~USD 170.4B across 835 deals-a clear pullback from the late 2025 rebound. Versus Q1 2025, value fell ~28% (from USD 238.1B) and volumes declined ~15% (from 977 deals), underscoring continued timing sensitivity; value also dropped sharply from Q4 2025’s USD 254.8B despite only a modest decline in deal count (852 → 835), suggesting fewer large ticket exits drove the slowdown. Compared with the 2021 peak (Q2 2021: USD 383.2B; 1,621 deals), the market remains structurally reset (value ~56% below peak; volumes ~48% below).

Crucially, exit diligence standards have tightened:

- Buyers now re‑underwrite value‑creation claims, not just historical results

- Operational KPIs, pricing initiatives, and technology narratives face deeper scrutiny

- ESG and resilience narratives require evidence, not aspiration

As a result, demand is shifting beyond transactional support: consultants are increasingly looking for end-to-end partnership to prepare portfolio companies for sale spanning operational improvement, growth acceleration, and profitability enhancement to defend the equity story in a more selective exit market

Market Outlook 2026: A Capabilities Driven PE Cycle

Q1 2026 data reinforces a clear message: this is not a return to 2021‑style exuberance. Recent geopolitical tensions briefly slowed the earlier pace, but investors continued to pursue large, high-quality assets with notable conviction. The market is entering a more institutional, more exacting phase.

EY’s PE Pulse report shows two key strategic shifts:

- Technology and software de‑risking: Tech fell from ~30% of PE deployment value in 2025 to just over 10% in Q1 2026, as AI‑driven disruption makes generalists more cautious and specialists more selective on business models. In coming months, tech will remain important but more bifurcated-winners in AI infrastructure, SaaS with clear differentiation, and vertical specific software will attract premium capital

- Shift toward hard‑assets and “defensive” sectors: Energy, infrastructure, industrials, defence, and AI‑enabled platforms are seeing more concentration of large deals, reflecting a preference for cash‑flow generating, defensible assets

For PE consulting firms, the implications are clear:

- Diligence must be faster, deeper, and decision grade - AI‑augmented due diligence (agentic workflows, benchmarking, normalization, scenario modeling) and data‑driven operating dashboards

- Operational value creation is now core, not adjacent - Consulting firms must act like embedded operating partners, designing and implementing growth, efficiency, and integration programs that are treated as core to PE value creation, not a side activity.

- Sector expertise outperforms generalist scale - Sponsors increasingly favour consultants with deep sector specific know‑how (such as industrial manufacturing, energy, or healthcare) because they can underwrite, integrate, and grow platforms more credibly than generalist models facing fee pressure from scale players.

Fewer deals mean higher stakes and greater reliance on trusted partners. For consulting firms that combine insight with delivery, 2026 represents not just a recovery, but an opportunity to increase relevance, influence, and durability.

How Evalueserve Can Support

Evalueserve supports across the deal lifecycle by delivering structured, scalable, and advisory‑ready deal intelligence.

- In the Pre‑Deal phase, agentic AI is used to extract and structure private equity and corporate transaction data across regions and sectors, enabling rapid market scans, target screening, and landscape analysis, with human expert validation ensuring institutional‑grade accuracy for client‑facing insights.

- During Deal Evaluation, this structured deal intelligence supports benchmarking and precedent transaction analysis, while detailed deal attributes-such as size, sector, geography, transaction rationale, and counterparties-help advisory teams accelerate diligence preparation and integrate evidence‑based insights into their evaluation workflows through system‑enabled access.

- In the Post‑Close stage, Evalueserve maintains continuous data refresh cycles to keep deal intelligence current, enabling longitudinal trend and performance analysis across historical and new transactions, while a centralized, searchable repository preserves institutional knowledge and supports ongoing portfolio analysis and future advisory engagements.

For more information, please visit here

Sources

- Bain & Company - Global Private Equity Report 2026

- Bain & Company - Private Equity Outlook 2026: Gaining Traction

- EY - Private Equity Pulse, Q4 2025

- EY - Private Equity Pulse, Q1 2026

- KPMG - Pulse of Private Equity, Q1 2026

- McKinsey & Company - Global Private Markets Report 2026