Key highlights for Q1’23

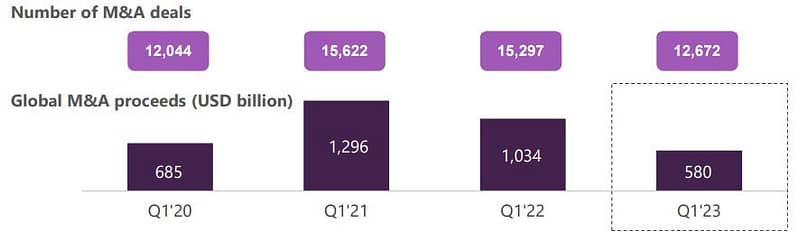

Major slowdown in M&A activity falling to a decade low

Through Q1’23, global M&A deals declined by 44% to USD580 billion, compared with last year, marking the largest YoY percentage decline since 2001. Meanwhile, the number of M&A transactions plummeted by 17% globally, making it a three-year low. In terms of M&A activity, Europe was hit the hardest, as evident in the 60% YoY dive in M&A value to USD90 billion, a 26-year low. Other regions fared relatively better, with the US at USD273 billion (down by 47% YoY) and APAC at USD145 billion (down by 23% YoY). Growing inflation, the banking crisis, rising interest rates and a looming global recession weighed on M&A activity. In terms of sectoral trends, deal-making in healthcare totaled USD97 billion in Q1’23 (an increase of 60% YoY), accounting for 17% of overall deal value while Technology declined by 64% YoY.

Debt capital markets open at four-year low

In Q1’23, overall global debt capital market (DCM) activity totaled USD2.4 trillion, down by 11% compared with Q1’22 and making Q1’23 the slowest opening period for DCM activity since 2019. Meanwhile, the number of new DCM offerings declined by 13% YoY and reached a four-year low. Global high yield debt activity during Q1’23 totaled USD51 billion, a decrease of 16% YoY; this was, though, nearly triple the Q4’22 level, which fell below USD20 billion for the first time since 2009. Furthermore, in Q1’23, global DCM issuance increased by 48% compared with Q4’22, marked the slowest quarter for global debt capital markets issuance since the fourth quarter of 2018. Green bond issuance broke quarterly records and totaled USD134 billion in Q1’23, a 25% YoY increase and the strongest quarter since 2015. DCM activity from consumer staples, technology and energy and power issuers registered double-digit percentage increases, compared with year-ago levels.

ECM activity opens at two-year high

Global equity capital market (ECM) activity totaled USD132 billion in Q1’23, an increase of 8% YoY and the strongest opening period for ECM activity in two years. The US accounted for 19% of overall issuance, with proceeds up by 31% compared with Q1’22, while China accounted for 32% of overall issuance. ECM offerings from EMEA issuers registered a 37% YoY increase, reaching a two-year high, while APAC fell by 17% YoY. Global convertible offerings totaled USD23 billion in Q1’23, an increase of 15% YoY and accounting for 17% of ECM activity. Industrials, media and entertainment, and energy and power were the most active sectors in convertible offerings accounting for 55% of overall issuance.

|

Announcement Date

|

Acquirer’s Name

|

Acquirer’s Nation

|

Target’s Name

|

Target’s Nation

|

Value (USD billion)

|

Target’s Industry

|

Consideration type

|

|---|---|---|---|---|---|---|---|

|

Mar 13, 2023

|

Pfizer

|

US

|

Seagen

|

US

|

43.8

|

Healthcare

|

Cash

|

|

Mar 12, 2023

|

Investor Group

|

US

|

Qualtrics

|

US

|

10.9

|

Software

|

Cash

|

|

Feb 08, 2023

|

CVS Health

|

US

|

Oak Street Health

|

US

|

9.9

|

Healthcare

|

Cash

|

|

Mar 06, 2023

|

Vistra

|

US

|

Energy Harbor

|

US

|

6.8

|

Energy

|

Cash + stock

|

|

Jan 23, 2023

|

Xylem

|

US

|

Evoqua Water Technologies

|

US

|

6.6

|

Industrial

|

Stock

|

Unfavorable market continues to create headwinds for global investment banks

In Q1’23, investment banking revenues of all major investment banks (except Barclays) declined due to globally weak market conditions that led to a sharp fall across all areas of business. A halt in deal-making amid heightened fears of a recession, rising inflation, restrictive policies of major central banks and a volatile market were the main reasons for the decline. Going forward, market performance is expected to be better due to pent-up M&A demand and a strong pipeline, provided the macro environment is stable.

Note: Revenues for Barclays and Deutsche Bank were converted into USD using the exchange rate as on 31 Mar 2023 Note: Revenues for Deutsche Bank reflect revenues from Origination & Advisory services

Bulge bracket investment banks’ performance – key highlights

JP Morgan’s investment banking (IB) revenue declined by 24% and fees by 19% YoY in Q1’23. Advisory fees were down by 6%, compared with a strong first quarter last year. Underwriting businesses continued to be affected by market conditions, which decreased debt fees by 34% YoY and equity fees by 6% YoY in Q1’23. The bank expects these conditions to continue despite its robust pipeline, because of sensitivity to market conditions and weak sentiment on economic outlook.

Goldman Sachs’ IB fees declined by 26% YoY in Q1’23, primarily due to significantly lower net revenues in advisory (reflecting a significant decline in industry-wide completed M&A transactions) and debt underwriting (reflecting a decline in industrywide volumes). The bank expects investors will need to see more certainty before financing markets reopen more broadly, and expects some positive signs in market activity, particularly in investment-grade markets, which have started the year strongly in the US and Europe.

Morgan Stanley’s IB revenue declined by 24% YoY in Q1’23. The decrease in advisory revenue was driven by fewer completed M&A transactions. Equity underwriting revenues were down by 22% YoY, largely due to depressed IPO activity. While IPO and follow-on activity remained muted, issuers selectively accessed market windows. An open investment grade market and opportunistic loan activity supported fixed-income underwriting results. Issuance activity during constructive windows is an encouraging sign for the underwriting business. Further, conversion from pipeline to realized is predicated on clarity around macroeconomic conditions, stable financing markets, and increased corporate confidence.

Morgan Stanley’s IB revenue declined by 24% YoY in Q1’23. The decrease in advisory revenue was driven by fewer completed M&A transactions. Equity underwriting revenues were down by 22% YoY, largely due to depressed IPO activity. While IPO and follow-on activity remained muted, issuers selectively accessed market windows. An open investment grade market and opportunistic loan activity supported fixed-income underwriting results. Issuance activity during constructive windows is an encouraging sign for the underwriting business. Further, conversion from pipeline to realized is predicated on clarity around macroeconomic conditions, stable financing markets, and increased corporate confidence.

Citi’s IB revenue declined by 25% YoY in Q1’23, as continued geopolitical uncertainty as well as heightened macroeconomic uncertainty and volatility continued to impact client activity. Revenues from its advisory, equity, and debt underwriting businesses declined by 17%, 41%, and 24%, respectively, but were within the range of the overall decline in volume across the industry. However, with a promising pipeline, the bank expects an improvement in client sentiment and a rebound in IB revenue, as the macroeconomic backdrop will likely become more conducive to client activity.

Barclays’ IB fees decreased by 7% YoY in Q1’23, due to a reduced fee pool. The upside was partially offset by a strong performance in advisory business, which represented the best Q1’23 performance. The bank’s deal pipeline remains strong, which will likely increase its fee income as rates and market conditions stabilize.

In Q1’23, Credit Suisse’s IB, equity, and debt revenues declined by 57%, 52%, and 53% YoY, respectively. The firm’s IB revenue decreased due to low client activities and less favorable conditions, particularly in equity sales and trading, capital markets, and advisory franchises. Credit Suisse and M. Klein & Company have mutually agreed to terminate the bank’s acquisition of the latter’s investment banking business due to the announced merger of Credit Suisse with UBS Group.

UBS’ global banking revenues declined by 30% YoY in Q1’23, mainly driven by lower revenue from capital markets. Advisory revenues decreased by 21% YoY due to lower M&A transaction revenue and a 43% decrease in the global M&A fee pool. Furthermore, revenues from the capital markets business declined by 37% due to a 61% fall in leveraged capital markets fee revenue, compared with a 58% decline in the relevant global fee pool. Revenue from equity capital markets decreased by 44%, compared with a 15% decrease in the relevant global fee pool.

Deutsche Bank’s origination and advisory (O&A) revenue declined by 31% YoY in Q1’23, which reflected low industry fee pools and issuance activities due to continued macroeconomic and geo-political uncertainties. The bank’s share in the global O&A market increased by more than 40 basis points in Q1’23, compared with Q4’22, which reflected its ongoing investments, especially in capital-light business areas.

Advisory firms stayed resilient in Q1’23, despite challenging market conditions

In Q1’23, major firms witnessed a decline in their advisory revenue. However, Greenhill’s revenue increased during the quarter. Most advisory firms also acknowledged increased risks associated with the current geopolitical, economic, inflationary, and market scenarios; however, they were cautiously optimistic about dealmaking in 2023.

Note: Houlihan Lokey’s fiscal year ends in March.

Performance of M&A advisory firms

Houlihan Lokey’s revenues decreased by 6% YoY in Q1’23, due to a slump in the average transaction fee on closed transactions driven by the size and timing of transactions. However, its restructuring practice continued to see strong business activities, and added to its confidence in H1’23. The advisory firm will likely see strong business activities throughout CY’24. In terms of outlook, the firm foresees pent-up M&A activities due to the high costs of debt, which is forcing some lenders to sit on the sidelines until they have a clearer view of the economy.

Evercore’s advisory fees decreased by 26% YoY in Q1’23, which reflected a decline in revenue from large transactions and in the number of advisory fees earned. The firm has appointed one new senior managing director each in private capital advisory business and technology practice. The firm’s private capital advisory and fundraising businesses activities increased in Q1’23, albeit at low levels against peaks in 2021. The fundraising environment across all fund sizes started witnessing marginal improvements in Q1’23, compared with Q1’22.

In Q1’23, Lazard’s financial advisory revenues decreased by 29% YoY. The ongoing slowdown in M&A activities globally continues to present significant headwinds for financial advisory services. However, the firm was actively engaged in advising clients in Europe and the US on a broad range of public and private assignments. The firm’s European advisory business continued its strong performance in Q1’23, and restructuring activities are increasing, especially in the US. Since the beginning of the year, the firm has noted an increase in M&A dialogues, as market sentiment seems to be improving.

Moelis reported a 38% YoY decrease in its revenue in Q1’23, due to the completion of fewer transactions and lower average fees earned per completed transaction compared with Q1’22. The firm has significantly expanded its technology investment banking franchise by hiring 11 managing directors, many of whom have worked together for several years. The firm has also appointed three additional managing directors in areas of key strategic importance. It includes one managing director in the private fund’s advisory group (joined in early April 2023) and two additional managing directors who will join in the coming months and focus on industrials and capital structure advisory.

PJT’s advisory revenues decreased by 7% YoY in Q1’23, due to a fall in strategic advisory and private capital solutions revenues. While the broader M&A environment in strategic advisory business remained challenging, PJT’s revenue from the same business decreased modestly in Q1’23, compared with Q1’22. However, the decline was significantly less than the decline in industry-wide completed volumes. The firm expects declines in strategic advisory revenues and overall M&A activities to be more modest. These declines will likely be offset by increasing restructuring business.

PWP’s advisory fees decreased by 13% YoY in Q1’23, due to a reduction in M&A activities driven by a restructuring fee event in Q1’23. The firm witnessed a decrease in average fee size per client and fewer transactions with outsized fee events, despite a modest increase in the number of advisory transactions completed. The geographic composition of revenue shifted toward the US in Q1’23, compared with Q1’22.

Greenhill’s revenues increased by 9% YoY in Q1’23, due to high fees from financing advisory and restructuring retainers. The firm has recruited Jakub Mleczko as a managing director. He will focus on financing advisory and restructuring. The advisory team continues to take on attractive new fund placement projects amid a challenging fundraising environment and should generate more revenues as the year goes on.

The road ahead

Well-capitalized companies to make bold strategic moves

During the global financial crisis in 2008–09, numerous industry-defining deals positioned acquirers for faster, more profitable growth out of the downturn. Likewise, in the current cycle, companies with a strong market position, cash on hand, and debt capacity will have the upper hand in executing transactions in their core businesses. Nearly every sector has a few cash-rich market leaders that stand to gain. Energy, industrials, and technology stand out as sectors where the top players have solid balance sheets and can make bold moves. Companies with strong balance sheets and an experienced M&A track record will be best positioned to complete the largest transformational deals and generate profit in the long run.

Pressure on valuation to present opportunities and roadblocks

Uncertainty regarding the cost and availability of capital, and the overall macroeconomic outlook will likely cause dealmakers to be more conservative in valuations. Yet, strategic buyers hoping for a steal deal will find increased competition from financial buyers. Lower valuations make corporate separations more likely, especially for high-value assets trapped inside larger corporates. Companies that have a valuation overhang from mispriced assets within their portfolio will seek to spin off or sell parts of the business to unlock overall value for their shareholders. Companies exploring the pathway to a potential IPO will not only face problems not only of a bear market and volatility, but will also have to acknowledge that the valuations they achieved from private investors in the last couple of years have not quite caught up with the change in public market sentiment yet.

Rise of activist campaigns

Following a brief decline during the pandemic, shareholder activism rebounded to pre-pandemic levels in 2022 despite volatile markets, depressed share prices, and macro-economic uncertainty, with the US and APAC leading the way. Depressed market valuations present an opportunity for prominent activist investors to launch new proxy fights, which in turn will boost M&A volumes in the coming quarters. More activism is likely due to the presence of a plethora of companies with components favored by activists, such as non-core assets that can be sold or spun off, or accumulated cash that could be better deployed, e.g., for stock buybacks.

Prevalence of small-to-midsized deals to continue

Historically, small-to-midsized deals (valued at less than USD500 million) have made up the bulk of M&A activity, which is expected to continue in FY’23. Such deals are expected to be easier to complete than megadeals, given their relatively lower risk, low reliance on financing, and less regulatory scrutiny. However, regulators may show more tolerance for large consolidation deals in sectors that have struggling assets (banking in Europe, telcos in developing economies, etc.).

Financial sponsors to deploy capital, given high levels of dry powder

In the last decade, private equity firms have become more specialized in industries and sub-sectors, which has helped them to make investment decisions with a higher degree of confidence in how their businesses might perform in different market cycles. Along with the availability of a record amount of uninvested capital, this could help drive more M&A activity despite choppy debt financing markets. While availability of high levels of dry powder can provide flexibility and the ability to take advantage of opportunities as they arise, it can also create pressure to deploy the funds and may lead to overpaying for acquisitions.

Portfolios to be reshaped through separation and divestiture

Down cycles and economic uncertainty will likely drive most companies to accelerate strategic reviews and re-evaluate their portfolios. Divestiture could become more common as it can help fund new investments. It is also likely to continue in the consumer products business, as quick sale unlocks capital and enables the leadership to focus on specific businesses. In 2022, advisory firms were resilient primarily due to restructuring activity; such activity is likely to remain elevated, going forward.