Key highlights for 9M’22

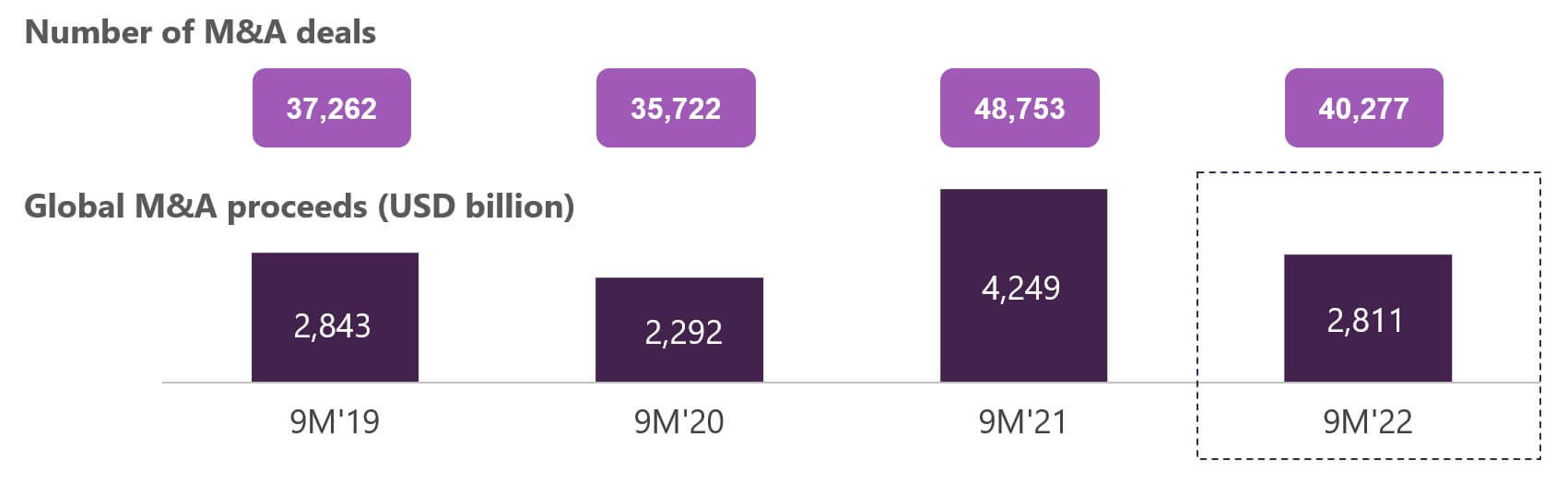

M&A activity witnesses major slowdown

Through 9M’22, global M&A deals declined by almost a third, compared with the last year, to USD 2.8 trillion, while the number of M&A transactions globally plummeted by 17%. Regionally, in terms of M&A activity, the US was hit the hardest, as evident by a 40% dive from last year to USD 1.2 trillion. However, it remained above Europe’s USD 712 billion (down 24%) and APAC’s USD 621 billion (down 30%). In Q3, M&A deal value fell below USD 1 trillion for the first time in the last eight quarters (down 58% YoY, the largest dip since the 2009 financial crisis). Together, growing inflation, rising interest rates, the energy crisis in Europe, a looming recession, and a weaker euro weighed on M&A activities. Generally, M&A activities tend to surge during Q4 as companies seek to close transactions before the end of the year; however, the performance in Q3 suggests activity in Q4 could deviate from the general trend.

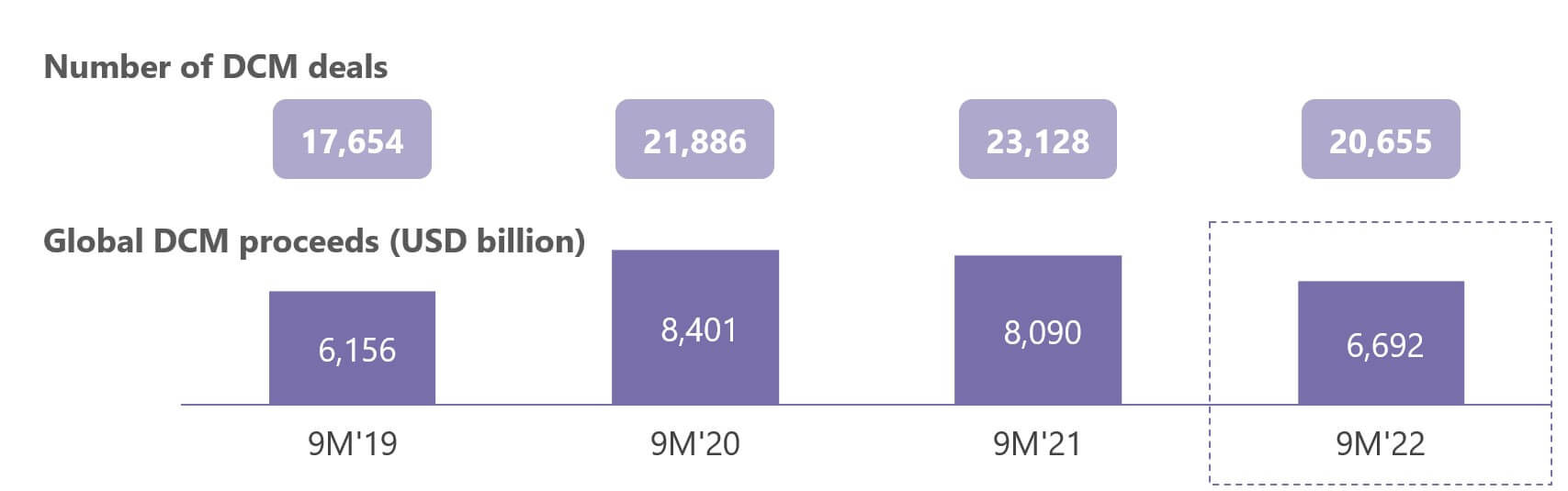

Debt capital markets plummet by 17%

So far in 2022, the overall decline in debt capital markets (DCMs) has been less dramatic than the equity capital markets (ECMs). In 9M’22, DCMs raised USD 6.7 trillion, down by 17% from the year-ago period. During the same period, the number of new offerings declined by a modest 11%. Financials, government, and agencies have increased their market share to 79% so far this year. Furthermore, the downtrend in debt issuance continued in the second half of the year. Debt issuance in Q3 declined by 23% from that in Q2. This was the first time since the end of 2019 that debt issuance missed the USD 2 trillion mark. However, Asia’s local currency debt turned out to be a bright spot in 9M’22. Debt issuance in Asia’s local currency has increased by 10% so far this year to USD 2.6 trillion, the strongest first nine-month period since 1980.

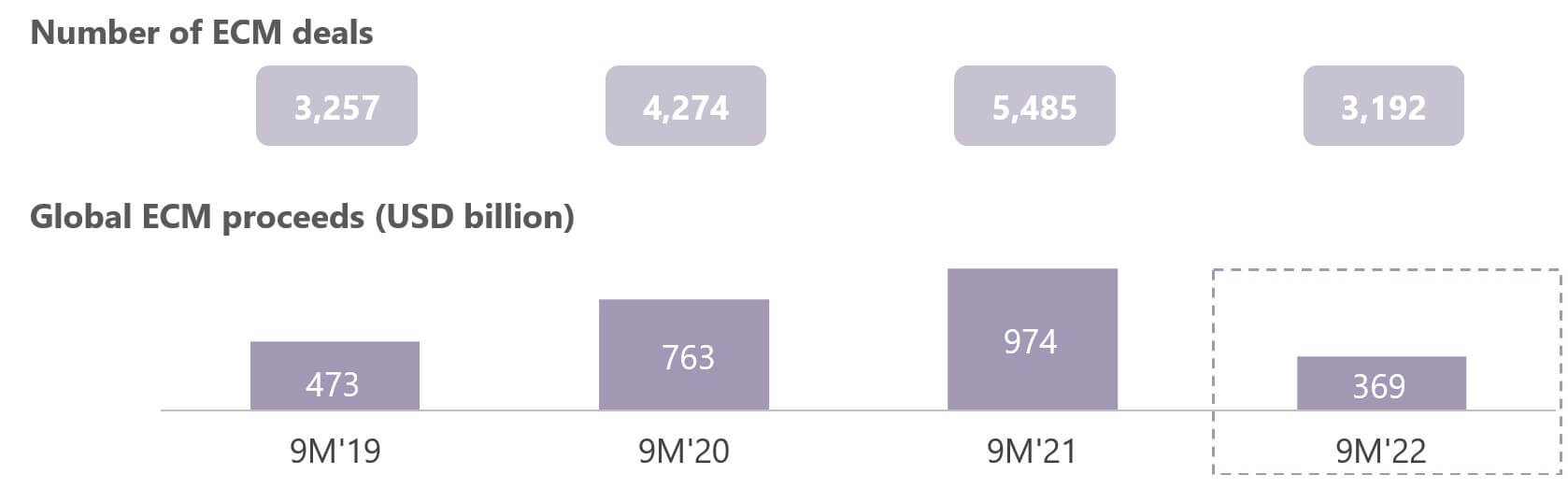

ECM activities decline to 19-year low

Through 9M’22, ECMs have witnessed the lowest opening since 2003, slipping down 62% from that in 9M’21. With equities in a steep decline and fears of a looming recession, the number of companies that launched IPOs in Q3’22 declined considerably on a year-on-year basis.

Globally, secondary offering activity stood at USD 207.9 billion during 9M’22, down 60% from the year-ago period. It was the slowest nine-month period for capital raising since 2003. Japan witnessed the strongest dip in equity issuance. It could only raise USD 5 billion, the lowest in 30 years. US IPOs decreased by 94% during the year to USD 6.6 billion. Proceeds from the EMEA declined by 67% to a 26-year low. Energy and power were the largest equity sector in the EMEA. However, amid the downtrend, China managed to capture a record market share during 9M’22.

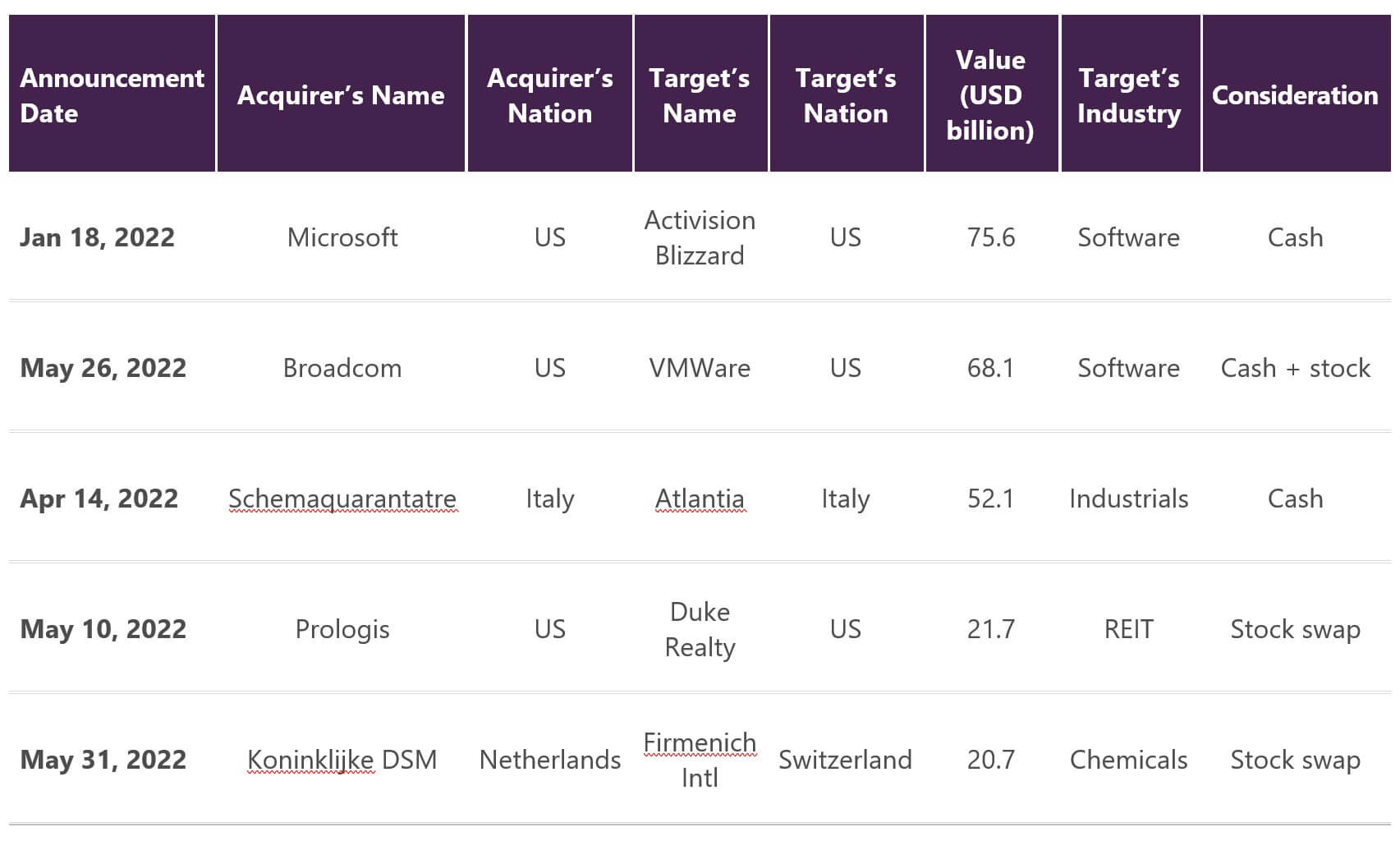

Top 5 M&A deals in 9M’22

Unfavorable market conditions create headwinds for global investment banks

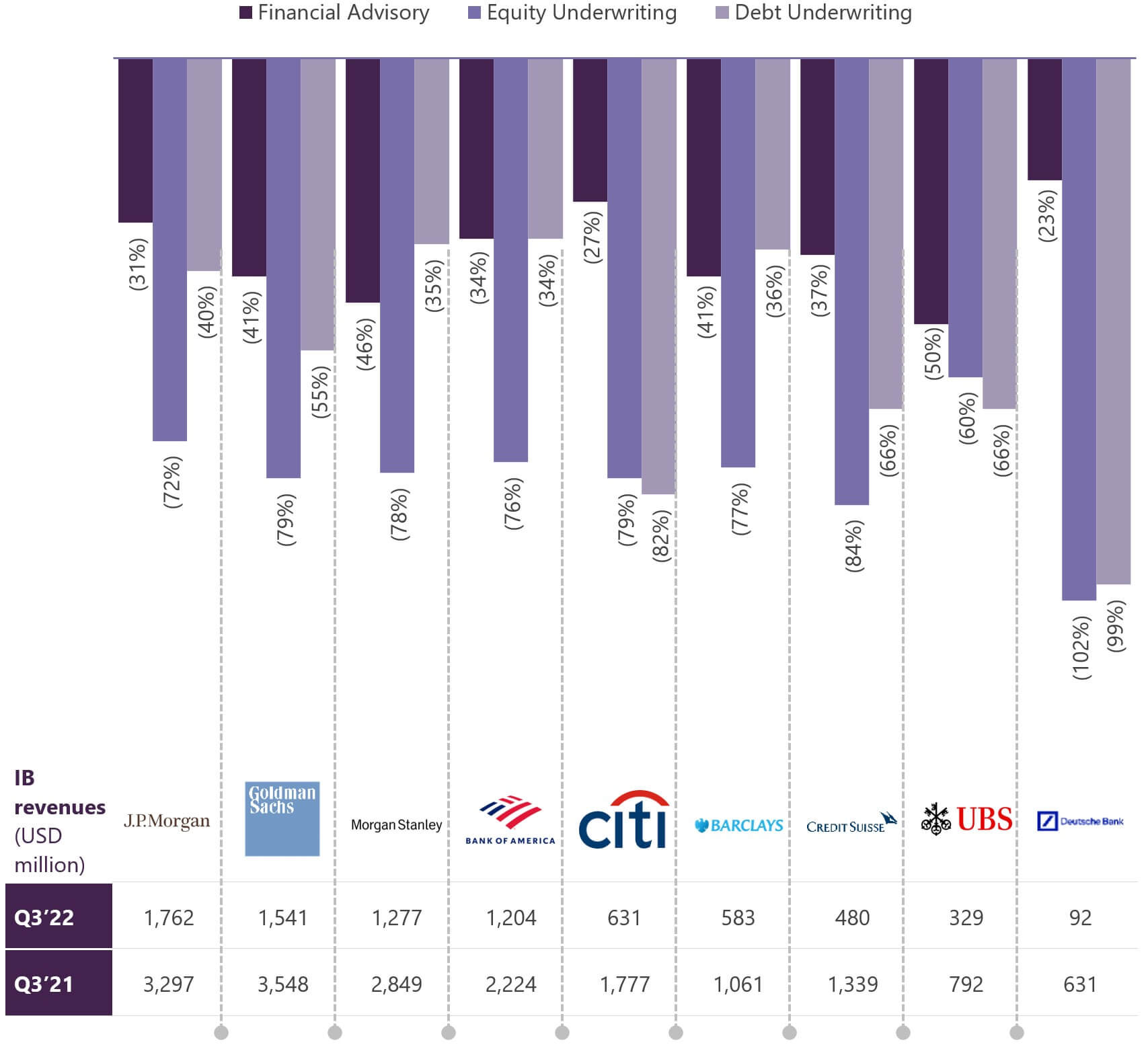

In Q3’22, the investment banking revenues of all major investment banks declined due to globally weak market conditions that led to lower fees from equity and debt underwriting. Most of the results mirrored the Q2’22 results, but with a less upbeat outlook for the rest of this year and 2023. A halt in deal-making amid heightened fears of a recession, rising inflation, restrictive policies of major central banks, and a volatile market were the main reasons for the decline.

Q3’22 investment banking revenues and YoY change

Note: Revenues for Barclays and Deutsche Bank converted into USD using the exchange rate as of September 30, 2022

Revenues for Deutsche Bank reflect revenues from Origination & Advisory services

Bulge bracket investment banks’ performance – key highlights

|

JP Morgan’s investment banking (IB) revenues declined by 43% YoY in Q3’22, due to low fee income. Fees were down by 47%, reflecting a similar trend across all products. In the advisory business, fees were down by 31%, reflecting low announced activities. Revenues from the underwriting business continued to be affected by market volatility, resulting in reductions of 40% and 72% in debt and equity fees, respectively. The bank expects a decline in IB revenues in Q4’22. However, the bank has a healthy pipeline of deals, the conversion of which may change the outlook. |

|

|

Goldman Sachs’ IB revenues fell by 57% YoY in Q3’22, due to significantly low net revenues from the underwriting, financial advisory, and corporate lending businesses. Its underwriting revenues declined due to low-net equity and debt underwriting revenues, reflecting a significant fall in industry-wide volumes. On the other hand, the lower financial advisory services revenues reflected a considerable decline in industry-wide M&A transactions, compared with the elevated levels witnessed in Q3’21. |

|

Morgan Stanley’s IB revenues declined by 55% YoY in Q3’22, driven by limited investment banking activity in an uncertain macroeconomic environment. Its revenues from the advisory business decreased due to low levels of completed M&A transactions, equity underwriting due to a substantial decline in global equity volumes, and fixed-income underwriting due to macroeconomic conditions. |

|

|

Bank of America’s IB revenues declined by 46% YoY in Q3’22, due to a 34% YoY decline in revenues from the advisory business. It also witnessed revenue decline of 76% and 34% in the equity and debt underwriting businesses, respectively, due to falling demand. Equity trading fell by 4% YoY due to a weak market in Asia and cash equities. The bank did not reduce its IB headcount despite the weak market activity. Despite the unfavorable market conditions, BoA’s IB revenues improved modestly, compared with Q2’22. |

|

|

Citi’s IB revenues declined by 64% YoY in Q3’22, due to increased macro-economic uncertainty and volatility. Revenues from its advisory business declined by 27% YoY due to a decline in market activities in North America and EMEA, and that of equity and debt underwriting by 79% and 82%, respectively, due to a decline in activities in North America, EMEA, and Asia. The bank expects IB revenues to reflect the overall market environment, which is marked by reduced capital market and M&A activities, during the remaining months of 2022. |

|

In Q3’22, Barclays’ IB revenues decreased by 45% YoY due to a low industry wallet across all business areas. However, the bank’s deal pipeline remains strong. In 9M’22, IB revenues declined by 36% YoY due to the reduced fee pool, particularly in the equity and debt capital markets, which witnessed robust growth in 9M’21. While the market environment for primary offering remains challenging, the same environment drives high-client activities in financing and trading in markets. |

|

|

In Q3’22, Credit Suisse’s IB revenues declined by 64% YoY due to significant revenue reductions in capital markets, low equity, fixed-income sales, and trading revenues, reflecting challenging operating conditions and the bank’s relative underperformance. Market conditions were characterized by continued geopolitical and macroeconomic uncertainty, resulting in higher levels of volatility for equity and interest rates, widened credit spreads, high levels of inflation, and increased energy prices. Although the bank’s pipeline remains robust, market conditions may delay deal completions in 2022. |

|

During Q3’22, UBS’s global banking revenues declined by 58% YoY due to low levels of industry activities across advisory and capital markets. Revenues from the banking and advisory business decreased by ~50% YoY due to low revenues from M&A transactions and a 39% reduction in the global M&A fee pool. Further, revenues decreased from the capital markets by 63% due to a 60% fall in ECM revenues, compared with a 57% decline in the global ECM fee pool, as well as from the leveraged capital markets by 62% YoY, compared with a 73% decrease in the global LCM fee pool. |

|

|

The bank’s revenues from the origination and advisory businesses decreased significantly due to limited origination and advisory (O&A) activities globally. The revenues decreased in all segments of origination and advisory businesses (debt origination, equity origination, and advisory). The leveraged debt capital market is likely to remain challenged in the short term, following a material decline in issuance levels in the rest of 2022. However, with the healthy pipeline and commitments, the bank is expecting a re-emergence in its O&A business in 2023. |

Mixed Q3 for advisory firms amid challenging market environment

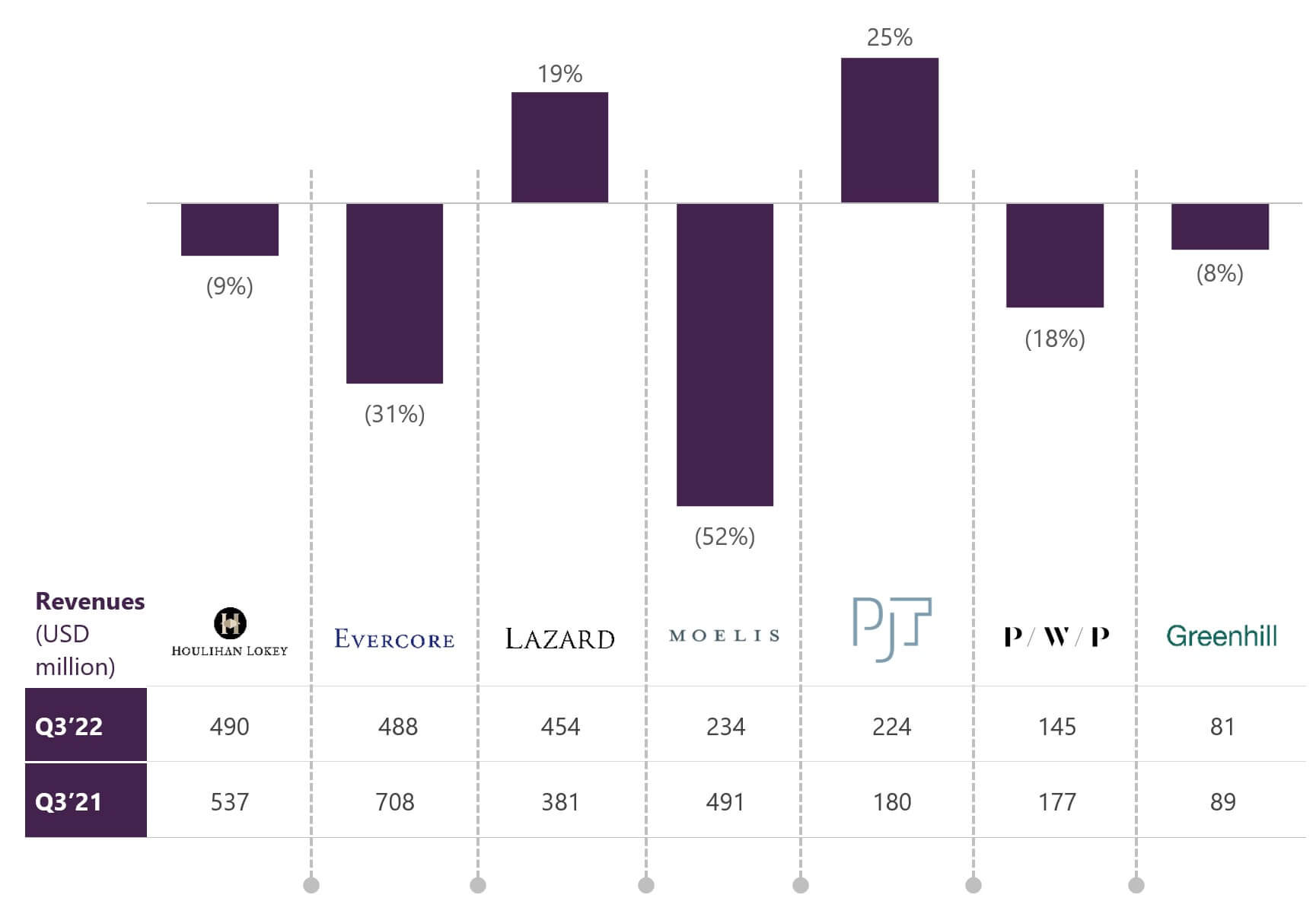

In Q3’22, while advisory revenue for Lazard and PJT Partners increased, it decreased for all other major advisory firms. Most advisory firms acknowledge the increased risks associated with the current geopolitical, economic, inflation, and market scenarios but are confident about their growth strategies.

Q3’22 advisory revenues and YoY change

Note: Houlihan Lokey’s fiscal year ends in March. The advisory revenues data is calculated for the three months that ended in September

M&A advisory firms’ performance – key highlights

|

The decrease in Houlihan Lokey’s revenues was primarily due to reduced numbers of closed deals and a reduction in average transaction fees on completed transactions. However, as compared to last quarter, revenues improved by 17%. Though the firm is expecting healthy new business activities, the market environment would remain challenging as the average time to close transactions remains elongated and elevated. A number of transactions are expected to be put on hold.

|

|

The decrease in Evercore’s advisory fees reflects a reduction in average fees from large transactions, a contraction in M&A activities, and a steep decline in overall market issuance. To reduce the impact of the challenging market environment, the firm is continuing to focus to expand its product capabilities and client coverage. In 2022, seven senior MDs joined Evercore’s advisory team, and one more senior MD (focused on technology) is expected to join in the near term. |

|

|

In Q3’22, Lazard’s financial advisory revenues increased by 19% YoY, reflecting a continuous momentum due to its strong position in Europe. The activity was relatively low in the structuring business; however, engagement with clients remained robust due to current market conditions and demand for liability management. The company continues to invest in diversifying its offerings for clients in financial advisory, including expanding its efforts in infrastructure, broadening the coverage in private credit, and launching a new geopolitical advisory group. |

|

|

Moelis reported USD 234 million in revenues, down by 54% YoY due to low levels of M&A activities and transaction completion in the capital market, driven by volatile markets. To support the M&A market growth in the future and increase its focus on technology, healthcare, industrial, and private fund advisory, the firm added 25 MDs (16 MDs through internal promotion and 9 MDs through external hiring) to its team. |

|

|

PJT’s revenues increased by 15% YoY due to a surge in strategic advisory, restructuring, and PJT Park Hill revenues. The firm reiterated the market conditions have been positive for the restructuring business, but it negatively affected the strategic advisory business, due to deals pushed out and deals withdrawn. PJT is expecting that overall revenues from strategic advisory business in 2022 would remain low compared to 2021 revenues. |

|

|

PWP’s revenues decreased by 18% YoY to USD 145 million during Q3’22, due to a reduction in M&A activities across most industry groups. However, the fall was offset by increased activities in the capital solutions advisory business, including restructuring, liability management, and capital market advisory services. PWP added 8 Advisory Boards in 2022 and plans to add more senior professionals to support strategic growth and increase coverage.

|

|

Greenhill’s revenues decreased by 8% YoY in Q3’22, due to a decline in financing advisory and restructuring completion fees. The downside was partially offset by increased M&A transaction completion fees. The firm witnessed a high level of activities in industrial and telecom infrastructure businesses, with most other businesses also set to make a reasonable contribution. The firm expects a substantial increase in the restructuring activity and related revenues due to favorable business conditions for M&A in Australia, Canada, and the US. |

Road ahead

ESG issues gaining prominence in M&A deals

Many firms are looking at M&A to advance their ESG agendas, either through the sale of legacy technology companies and assets or through the purchase of new net-zero technology. Record amounts of ESG funds have already been raised this year, and it appears that this will continue to be a key driver of M&A activity. Going forward, investors are likely to pay more attention to a company’s proven ESG credentials including SPACs’ top targets, which will likely bring a surge in sustainable investment SPAC IPOs.

Inflation and recession worries drive change in investor considerations

Inflation, rising interest rates, and other pressures may have slowed down M&A, but the situation hints at a recovery to healthy pre-pandemic levels. Investors will likely see buying opportunities in the current environment as buyers pull back in the face of potential stagflation and a possible recession. Over the next few months, dealmakers are expected to focus on technology, ESG, and ‘recession-proof’ opportunities, among others.

Macroeconomic and geopolitical factors slow down ECM deals

The global economic slowdown, inflation, and interest rate hikes by central banks have weighed on the IPO pipeline, which may lead to a dip in ECM volumes and charges. This situation is unlikely to change in Q4’22. Global bond sales are expected to decline due to inflation, supply chain disruptions, concerns over rate hikes, and the Russia-Ukraine crisis.

Private capital set to drive deal activity

Despite fragile global markets and economy, along with increased regulatory intervention, M&A activity is expected to accelerate due to a particularly strong flow of private capital. Capital market conditions have tightened through Q3’22, but PE firms still have large amounts of dry powder that have to be deployed by the end of 2022. Private capital is expected to be used in both equity and debt transactions.

Managing currency risk will be key in cross-border M&A

The current economic environment in the US seems favorable for domestic companies to make investments outside the country due to the strength of the dollar, a beneficial environment for interest rates, and surplus cash at hand. To make sure that currency fluctuations do not adversely affect the target price, businesses will continue to consider cross-border M&A.

Valuation gap likely to widen

There is a discrepancy between sellers’ and buyers’ expectations for deal pricing due to declining valuation levels, particularly for technology companies. Many sellers are expected to continue basing their expectations on the higher valuation levels of prior years, even though buyers are more evidently being drawn to greater financing costs and lower valuations. History shows that it will take sellers several months to adjust their expectations to the new situation.