LIBOR or London Interbank Offered Rate, the benchmark interest rate at which major global banks lend to one another, was a very important number until recently. However, it fell out of favor after a large number of banks manipulated it to boost their profits. Subsequently, UK’s Financial Conduct Authority (FCA) decided to phase out LIBOR completely by 2021.

Following the FCA’s verdict, companies dependent on LIBOR, such as investment banks and mortgage lenders, will have to change their systems to new alternative benchmarks within a short span of two years. The transition will be challenging, as it will involve diverse stakeholders, including company departments, top management, industry associations, and regulatory agencies. Are you prepared to handle the change?

LIBOR Liabilities

LIBOR has been around for more than 50 years. However, the mechanism used to fix the rate is flawed and open to manipulation. LIBOR bench rates are determined through a survey of rates at which large banks are ‘willing to borrow from each other.’

The survey, conducted by an administering agency (currently ICE Benchmark Administration Limited, earlier British Bankers’ Association), covers five currencies across seven tenors (from overnight to 12 months). The rates provided by the banks are averaged to arrive at a ‘mid-rate’, which is published by Thomson Reuters. Thus, LIBOR is based on estimates rather than actual transactions, and does not involve any audit.

While LIBOR served as an indicator of confidence in the financial system, it gave rise to questions on conflict of interest, as participating banks had derivative positions to the tune of trillions of dollars tied to it. It is not surprising that banks colluded to manipulate LIBOR to generate unprecedented profits for themselves.

The LIBOR scandal became public in 2012, when the UK Serious Fraud Office started criminal investigation and found that several banks had understated LIBOR survey rates for unlawful gains.

Continued investigation resulted in regulatory authorities slapping fines worth billions of dollars on large banks, such as Deutsche Bank, Barclays, UBS, Rabobank, and the Royal Bank of Scotland. It also led to several discussions on the need to change LIBOR, which finally culminated in regulators deciding to phase out LIBOR altogether. In 2017, the UK FCA informed that it would phase out LIBOR by 2021.

In the face of these dramatic developments, the search for an alternative to LIBOR has begun, and regulators around the world are actively engaged in the process.

Benchmark Basics

In order to counter their disadvantages and limitations and to arrest manipulation, the International Organization of Securities Commissions (IOSCO) and the Financial Stability Board (FSB) have set some pre-requisites for interest rate benchmarks.

According to these bodies, a benchmark should have the following features:

Reliability – It should reflect the ground reality of a financial system and risk levels in a banking system as closely as possible. Incorrect estimation has the potential to not only adversely impact the health of the financial industry but also the economy as a whole, as even the smallest miss-pricing can have a domino effect.

Resilience – It should be able to accommodate crisis and market stress. Benchmarks need to be strong enough to withstand market dislocations, accommodate diverse market situations, and spur confidence during uncertainty.

Transparent and replicable methodology – The benchmark determination process should be clearly defined and replicable.

Minimized probability of manipulation – Benchmarks must be based on actual transactions and not hypothetical estimates. Also, only large volume transactions should be included to determine benchmarks, to accurately reflect market reality and improve confidence.

Accountability – Adequate mechanisms must be established to ensure auditability and prevent manipulation of the system by vested interests.

Will SONIA be Next?

A number of benchmarks have been developed to replace LIBOR. In April 2017, a working group set up by the Bank of England (BoE) recommended the Sterling Overnight Index Average (SONIA) as the preferred benchmark for the British pound. Benchmarks developed for other currencies include the Secured Overnight Financing Rate (SOFR) for the US dollar, Tokyo Overnight Average Rate (TONAR) for the Japanese yen, Swiss Average Rate Overnight for the Swiss franc (SARON), and the Euro Short-Term Rate (ESTER) for the euro.

While all these are being published and are beginning to find uses, we detail determination mechanism of SONIA, and how it compares to LIBOR, as FCA has mandated it will replace LIBOR by end 2021.

SONIA, which is based on the interest paid on sterling short-term wholesale funds, is administered by the BoE.

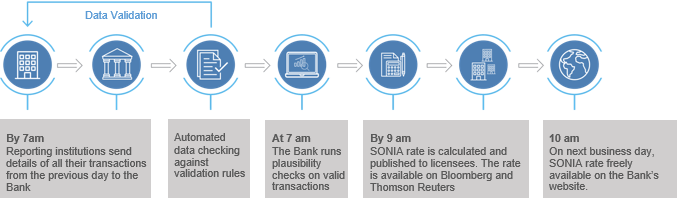

The chart below explains the SONIA determination process.

Source: Bank of England, SONIA Statement of compliance with the IOSCO principles for Financial Benchmarks

SONIA calculation is based on:

- Interest paid on sterling overnight transactions under normal conditions

- Rates data collected from BoE’s Sterling Money Market Daily data collection form

- Volume weighted average focused on central 50% of distribution

- Transactions worth more than GBP 25 million

The BoE reviews the methodology periodically to ensure that data quality is robust, the benchmark adheres to its purpose, and data collection is in line with benchmark requirements.

SONIA is more robust and less susceptible to manipulation than LIBOR, as it is based on actual transactions. The data for SONIA is collected from the BoE system, rather than from banks, as opposed to LIBOR. Moreover, SONIA tracks banks’ rates fairly closely, and is already referenced in a liquid sterling overnight indexed swap (OIS) market.

SONIA, or any other transaction-based interest rate alternative, will work for currencies and tenor for which liquid markets exist, and one can borrow in ‘size’ (i.e. large value). However, there will be cases when a market may be illiquid and unrepresentative; in such instances, LIBOR will be missed.

Looking Forward with Confidence

Now that alternatives have been identified, the next step would be for companies to shift to a new benchmark. The process of shifting from LIBOR will certainly be daunting, considering contracts worth more than USD 350 trillion are tied to it. LIBOR transition will impact every participant differently, as they operate in diverse financial subsectors. Within organizations, this change will lead to significant cross-functional follow-on activities involving business; IT; operations; and the legal, finance, and accounting teams.

In this inescapable commotion, apart from pooling internal resources, companies have the option of using third-party firmswhich have expertise in risk analytics and quantitative support. Such firms can provide support on operational change, regulatory requirements, quantitative modeling, data management, and technology, as well as guidance on the transition process.

Check out this use case to see how we help benchmark administration teams of investment banks implement regulatory control frameworks. Our support leads them to create compliant benchmarks to avoid conflict of interest. Our technology solutions bring efficiency and robustness, and enable easy auditability of calculation processes.

Download as .pdf Benchmark-Compliance-via-Regulatory-Support(use-case)

Would you want to evaluate how the transition will impact your firm, and how we can support you? Click HERE to send a query.