Introduction

The adoption of clean energy transition pathways seems to be muscling up well across the globe, wherein solar PV, wind, and hydropower have proved popular. An urgent need to overcome the energy crisis, which has plagued developed economies in recent years, has led to a rapid ramp-up of renewable energy (RE) generation capacities across various geographies. This is being carried out in a bid to reduce further dependency on non-renewable energy sources and meet the Net Zero 2050 carbon dioxide (CO2) emission reduction targets. The same crisis also had a knock-on effect on the economy.

At the same time, major players from fossil fuel sources, including coal, oil, and gas among others, are also pivoting hard to reduce their carbon footprint and mitigate climate change causing-activities. However, some of the said dependencies are so far unavoidable as well.

We have previously written about how the energy transition is attracting such furore in so many directions, it should be called an energy transformation, which is leading the way to the emergence and unprecedented growth of a new global clean energy economy. At the centre of this move, is a race to identify opportunities and develop pathways that will not only ease the transition but may also create new centres of ‘power’ with some surprising results. We take a look:

Observations

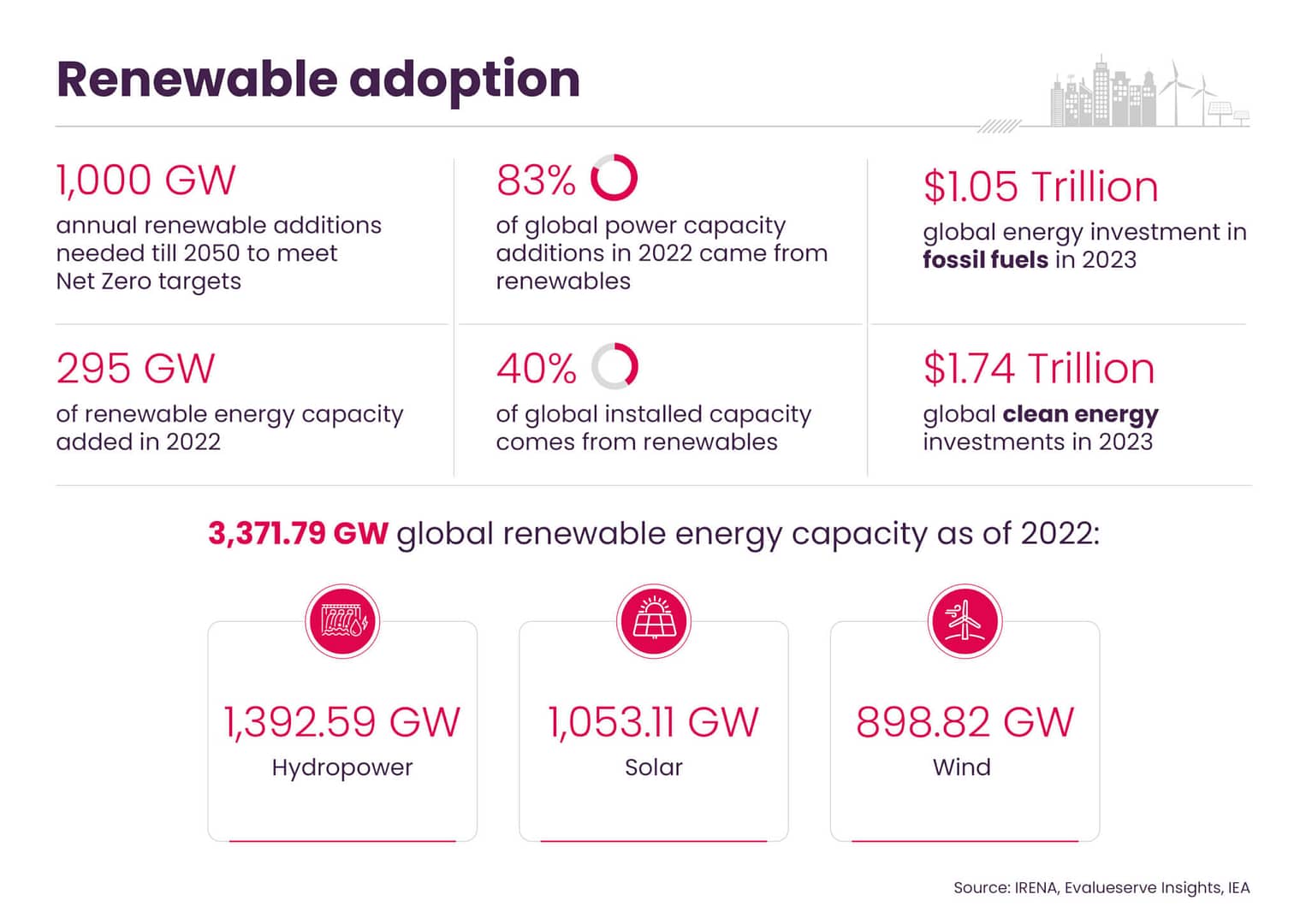

Spend role-reversal: Total energy investments into clean energy have grown significantly in the last 5 years and have consistently been higher than investments into non-renewables, which have been on the decline since 2017. The last time spending on non-renewable fossil fuels was higher than clean energy was in 2015. In 2023, of the estimated $2.8 Trillion global energy investments expected, $1.74 Trillion are going towards renewable energy and about $1.05 Trillion to non-renewables.

China’s overtake: China rules the roost in total renewables-based electricity capacity at around 1,206.58 GW. It also recently announced that of its total installed power generation capacity, non-fossil fuel energy sources now stand at 50.9%. In 2021, China had originally planned to achieve this by 2025 but has completed it in half the time. However, there is a difference between installed capacities and actual energy consumption. China’s consumption of fossil fuels, particularly coal, remains fairly high at 56.2% of its energy mix.

Rising sun: Solar PV is really charging up the energy hill, accounting for the quickest growth as well as the biggest capacity expansion in 2022, making up 83% of the total RE capacity additions in 2022. Not just that, it is projected that investments in solar will outshine those in oil production by the end of 2023. A decade ago, investments in oil production used to be 5 times that of solar. Then, there is the fact that advanced and developing economies alike, including the US, India, and others have incentivised solar PV manufacturing and installation, securing a strong flow of deployment for the coming years.

Oil & gas decline? The global energy crisis along with sanctions emanating from Russia’s invasion of Ukraine had resulted in a scramble for oil and gas supplies and an unforeseen cash flow into the coffers of oil & gas majors. However, the industry which had traditionally been directing a vast majority of spending towards capital expenditure and new supply investments until 2016, has spent less than 50% of its surprise cash flow into the same in 2022. While there has been a steady decline in capital expenditure over the past 7 years, the oil & gas industry has not redirected a lot of the balance cash flow towards clean energy.

LNG dilemma: With Russia’s supply of natural gas to the EU reduced by 80%, there was a dash to procure new alternatives, secure supplies, and develop infrastructure. However, the high energy prices and supply shortages can only lead to a short-term spurt in growth, with the longer-term outlook remaining largely uncertain for natural gas, with the chance of a decline.

Low-carbon fuels: There seems to a be resurgence in investment towards low-emission fuels including hydrogen, from the increase in major projects, as well as funding and M&A activity from some oil & gas companies. With incentives from various government policies and the uncertainties of fossil fuels usage allowance for transport in coming years, there is a renewed interest in biofuels as well.

Conclusion

No one wants to face another energy crisis. So, everyone is finding their way to greater energy security, keeping sustainability and resilience in their sights. While impressive, the biggest chunk of investment increases in renewables is primarily focussed in a handful of countries. 90% is concentrated in advanced economies, with China being the exception member. Meanwhile, spending on fossil fuels still rises, especially on the back of a surprise payday for oil & gas.

There is a strange dichotomy here. Some suffered the consequences of power strains from the crisis and would not like a repeat of that. They are hence spending on clean energy with a possible backup plan based on fossil fuels, while others are spending on fossil fuels to augment their short-term returns, and ease debt, but also facing uncertainties in the longer term.

While the concentration of high spending in either direction reflects whether a market has traditionally been an import-dependent or export-dependent one in its energy mix, new names are showing up on the top lists. This change emanates from an assortment of early adopters of energy transition pathways, as well as economies that have previously avoided the high costs of clean energy in its early stages. The latter geographies are now racing to v, and hence reach the comfort of costs through economies of scale.

The advent of a clean energy transition, wherein every few days, we are witnessing a new geography announce their decreasing dependency on fossil fuels, is also showing us potential new leaders in technologies and pathways that did not exist a decade ago. Policy that is looking more inward is also seen from some parts of the market, which suggests incremental self-dependence for these geographies. The unprecedented pace at which development is taking place almost feels like a race to the top of the mountain. All of this points to only one thing – the advent of clean energy industrialisation!

Get decarbonization publications delivered to your inbox by filling out the form below.