The highly discussed Securities Financial Transactions Regulation (SFTR), which aims to bring transparency in security financial transactions and improve post-trade services, was due on April 2020. However, due to the Covid-19 pandemic impacting the EU financial market, concerns were raised by the International Capital Market Association (ICMA) and the International Securities Lending Association (ISLA) with respect to the SFTR timelines. Under the circumstances, the European Securities and Markets Authority (ESMA) has postponed the implementation dates by three months.

The journey of SFTR had initially started in Jan 2016 and is now planned to become partially in force from July 2020. As a result, it has become the most convoluted regulation seen in the financial industry since the 2008 financial crisis.

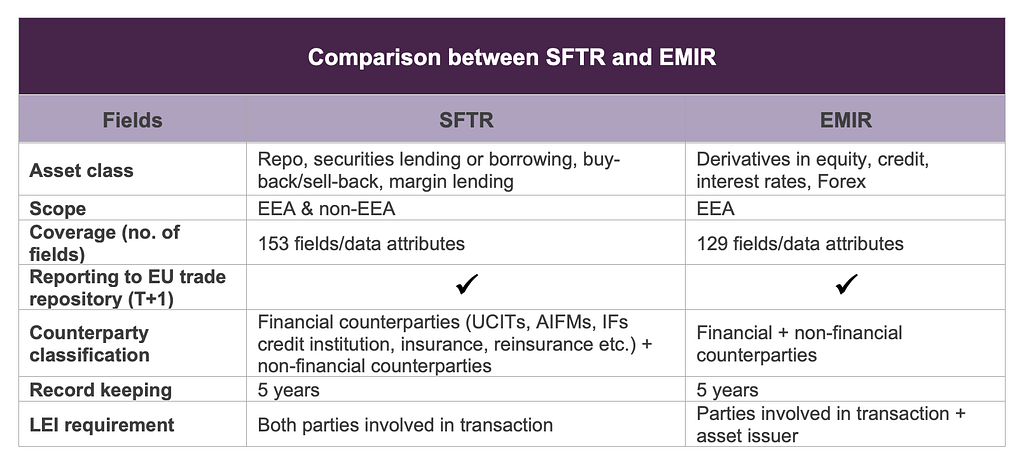

SFTR vs. EMIR

SFTR’s primary requirement is to maintain various data attributes for reporting trade repository. This makes it very similar to the European Market Infrastructure Regulation (EMIR) and can be considered an extended version of EMIR and the Markets in Financial Instruments regulation (MIFIR). The major difference between the two is that EMIR’s reporting requirements are only at 129 data fields, whereas SFTR’s focus on minimizing systematic risk and increasing investor transparency covers 150+ data attributes. Below are more similarities and differences between SFTR and EMIR.

Similarities and differences between SFTR and EMIR

SFTR & Reference Data Attributes

Various reference data points are based on counterparty, margin, transaction, collateral, etc. with a few of the data fields being more complicated than others. SFTR requires counterparties to report details of any SFT that have concluded, modified or terminated to ESMA’s approved Trade Repository on T+1 basis. Financial experts are commenting on SFTR’s heavy-data regulations, which is comprised of various counterparty and instrument reference data points.

Key reference data attributes covered in SFTR

Market participants believe that the main challenges fall under two key attributes: Legal Entity Identifiers (LEI) and Unique Transaction Identifiers (UTI). LEI is 20 alpha numeric code-based ISO guidelines, which is used as a unique global identifier to improve financial systems quality and accuracy. UTI is an alphanumeric code of maximum length defined as 42 or 52 for the US and EU respectively. It is a trade ID assigned to every security financial transaction to identify trade.

SFTR and LEI Implementation

ESMA’s statement on the implementation with respect to LEI requirements, suggests that an asset issuer’s LEI is part of transactional data along with lending & borrowing parties. Market participants have been familiar with LEI information being mandatory for counterparties, but not for the LEI of the issuers. This newer concept in the financial industry previously seen with EMIR and MIFIR only required counterparties involved in the financial transactions to have LEI.

If a borrowing and lending activity is occurring between two entities, it is mandatory for both the counterparties to have a LEI and the collateral in which has been traded.

Securities’ financial transaction and LEI mandatory requirements

SFTR Timelines—Postponed for 3 months

In order to ease the SFTR onboarding process, the implementation was drilled-down to various phases with short intervals of approximately 3 months.

SFTR Covid-19 update and novel SFTR timelines

Phase 1 and phase 2 (13th July): The first wave of financial counterparties (FCs) were comprised of investment firms and credit institutions. After Covid-19, various credit institutions were integrated into this phase as well. The main CCPs covered were central counterparties clearing houses, CSDs central securities depositories, etc.

Phase 3 (13th October): The last leg for financial counterparties must be completed by this date which covers insurance companies, UCITs, AIFs, Pension, etc.

Phase 4 (2021): The year 2021 will be focusing on all non-financial companies and will also bring the cut-off point for non-EEA companies to meet LEI requirements. The ESMA has created a waiver of 1 year (from launch of SFTR) for non-European entities or “Third Country Entities” to not stop the implementation of SFTR. As many companies outside of Europe do not have LEIs, this waiver will keep the implementation of SFTR on track. ESMA expects that by next year, all agent lenders (or third-party agents) involved in SFTs/use collateral securities issued by third-country entities, must apply for LEI and report.

SFTR and LEI Coverage

The launch of SFTR comes as good news for GLEIF and LEI issuing agencies, which are known as LOUs (Local Operating Units), as LEI requests could significantly increase outside of Europe. Currently there are around 34 LEI issuing organizations accredited by GLEIF which issue, renew and provide other entity data-related services to clients globally. LEI issuance reached its peak in 2017 with the launch of MIFID II. MIFID is a directive similar to SFTR, which aims to increase transparency across EU’s financial markets. It was launched with the slogan “No LEI, no Trade”, making LEI mandatory for both counterparties involved in any trade or financial transactions.

Similar to EMIR, reporting for SFTR has also made the LEI number mandatory for third-party agents, brokers, CCPs, clearing members, CSD participants and all parties involved in the financial transaction. The extension that SFTR has brought in LEI coverage from MIFID is primarily covering the LEI of the issuer of security, or the collateral involved in any security financial transaction.

Evalueserve Offering on SFTR

Major challenges investment banks and brokers foresee with SFTR is around data sourcing, as there are multiple sources involved and a lot of data fields. LEI is a 20 digit code authorized by GLEIF, and is one of the most critical attributes which requires mapping with the SFTR report.

Banks and other financial institutions operate with a huge database, which may have stale and duplicate data making LEI mapping difficult.

Evalueserve offers Enhanced Global LEI database providing single, universal standardized LEI against all counterparties, which must have an LEI involved in SFTs.

Evalueserve Enhanced Global LEI Mapping Offering Options:

- One-time mapping activity for existing customer base

- Enhanced Global Evalueserve LEI Daily Feed

- Maintenance Support for M&A, Name Change, New LEI, etc.

If you would like to see how your organization can utilize SFTR, please: