As part of the European Union’s action plan for financing sustainable growth, the European Commission, the executive arm of the EU, introduced the Sustainable Finance Disclosure Regulation (SFDR) in March 2021. SFDR Level 1 set out actionable guidelines for classifying investment products and reporting on the inclusion of sustainability risks in investments as well as the impact of sustainability risks on investment returns. Level 2 of the SFDR was effective since the first week of 2023, and it made it mandatory for asset managers to disclose additional information related to integration of sustainability risks in the investment decision-making process, quantify the performance of investments based on disclosures and reporting, and highlight the impact of sustainability risk on the investment decision-making process, along with mitigation plans for the risk. By adhering to this regulation, asset managers will benefit from reduced exposure to risk and from better long-term financial performance.

The Objectives of SFDR

SFDR aims to improve sustainability-related disclosures (i.e., the impact on climate, emissions to water, and other sustainability information) in investment strategies, which will make it easier for investors to compare different financial products offered in the European region. Another major SFDR objective is to clamp down on greenwashing, with the regulation requiring asset managers to disclose actual sustainability characteristics and objectives of a financial product with no scope for overstating product characteristics.

How Greenwashing Happens

Asset managers may inadvertently engage in greenwashing due to multiple reasons:

- Subjectivity and lack of standardization of sustainability data: Several ESG reporting standards exist, each with varying levels of reporting requirements. A rating agency may prioritize different aspects of sustainability depending on its areas of interests and values and may apply some data assumptions for reported data in case of incomplete disclosures.

- Inadequate expertise: Asset managers may lack the expertise or resources needed to conduct thorough sustainability assessments of their investments. In some cases, they may rely on third-party data providers to make sustainability claims, without fully understanding the methodology or limitations of the data.

- Self-reported green actions: Portfolio companies self-disclose their green practices, increasing the risk of asset managers being exposed to greenwashing.

The Scope of SFDR

SFDR covers financial market participants and advisers based in the EU, as well as investment managers or advisers based outside the EU who market (or plan to market) their products to clients in the EU under Article 42 of the Alternative Investment Fund Managers Directive (AIFMD).

Investment products launched after March 10, 2021, must fully comply with SFDR. Products launched before March 10, 2021, are not required to amend their precontractual disclosures; however, they are mandated to provide website disclosures alongside periodic disclosures.

Principle Adverse Impacts (PAIs) are a list of sustainability factors that firms need to consider when implementing their investment policies and taking investment decisions. PAIs are measured by a set of 18 mandatory indicators and two additional indicators (one environmental and one social) from a list of 46 remaining indicators that asset managers must disclose. For asset managers who do not consider PAIs of investment decision on sustainability factors are required to explain the reasons on their websites.

The Details of SFDR Level 1

SFDR Level 1 (core disclosures), effective March 2021, applies at the entity level and requires the disclosure of sustainability risks considered in the investment process and the PAIs of investment decisions on sustainability factors. It also requires transparency of remuneration policies in relation to the integration of sustainability risks. SFDR Level 1 disclosure requirements at the product level for products under Article 6, 8, and 9 are explained below:

Article 6, Article 8, and Article 9 under SFDR Level 1

|

Fund Type

|

Definition

|

Additional Details

|

|||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

|

Article 6 Fund

|

Funds with no ESG objective

|

• This is the default classification for funds.

• Sustainability is not an objective of these funds. |

|||||||||

|

Article 8 Fund (or light green fund)

|

Products that promote environmental or social traits

|

• ESG is one of the factors considered in the investment process.

• Firms need to disclose the extent to which they align with EU taxonomy regulations |

|||||||||

|

Article 9 Fund (or dark green fund)

|

Products with environment or social investment as their objective

|

• These products must comply with the ‘do no significant harm’ (DNSH) principle.

|

|||||||||

The Details of SFDR Level 2

-

Effective January 01, 2023

From this date, asset managers must publish website disclosures for Article 8 and Article 9 funds in accordance with SFDR Level 2 requirements. -

January 01, 2023 onward

For Article 8 and Article 9 funds, Level 2 financial report disclosures must be included in fund reports. The disclosures for these funds could be for any financial year or reference period. -

June 30, 2023

This is the SFDR Level 2 deadline for asset managers to publish entity-level PAIs for calendar year 2022.

Level 2 (enhanced disclosures) sets out additional disclosure requirements at two levels:

- Entity level: Disclose summary of PAIs, description of PAIs on sustainability factors, engagement policies, reference to international standards, additional content, and methodology for PAIs on the website of the asset manager, including

- Policy description to identify PAIs, including how policy is implemented and updated in a timely manner

- Methodology employed by the fund manager to select PAI indicators

- (Where information on PAI indicators is not readily available) Details of actions taken to obtain information from other relevant sources, such as directly from portfolio companies, external sources, third-party data providers, or industry experts, along with assumptions made, if any

- Product level: Disclose requirements followed to strengthen reporting to justify Article 8 and 9 product labels

Level 2 requirements also include identifying, measuring, and reporting the extent to which product investments are aligned with EU taxonomy.

The Rules for Level 2 Disclosures

|

Fund Type (i.e., investment labels)

|

Contents of Pre-contractual Reporting (to be done in the main body of the prospectus)

|

Contents of Website Reporting (to be made in a different section of the asset manager’s website under the heading 'Sustainability related disclosures’)

|

Contents of Periodic Reporting (to be done in the main body of the financial disclosure report)

|

||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

Article 8 (promotes ESG characteristics)

|

• Reporting on whether the fund promotes sustainability characteristics without having a sustainable investment objective

• For financial products with environmental objectives, reporting of extent to which sustainable investments are aligned with the EU Taxonomy • For financial products with a social sustainability objective, reporting the minimum share of sustainable investments during the period covered in the periodic report |

• Two-page summary of required website disclosures

• Clear statement of no sustainable investment objective • Investment strategy • Sustainability characteristics of fund • Proportion of investments • Monitoring of sustainability characteristics • Methodology and screening criteria used • Data sources used and processing • Limitations of data and methodology • Due diligence • Engagement policies • Description of any index designated as a reference benchmark for the environmental and social characteristics of the fund differs from a relevant broad market index (if applicable |

• Reporting of extent to which environmental or social characteristics promoted by the financial product were met during the period covered in the periodic report

• Top investments • Asset allocation • Economic sectors in which investments were made • Details of the proportion of investments per environmental objective under the EU Taxonomy • Proportion of socially sustainable investments (if applicable) • Reference benchmark (if applicable) |

||||||||||||||||||

|

Article 9 (has sustainable investment objectives

|

• A statement that the fund has sustainable investment as its objective

• For financial products with environmental objectives, reporting of the taxonomy-aligned investments and concise and transparent information on any non-taxonomy-aligned investments • For financial products with a social sustainability objective, the minimum share of social sustainability investments during the period covered in the periodic report |

• Summary of required website disclosures

• Investment strategy • An explanation of whether and why the fund's investments comply with the Do No Significant Harm (DNSH) principle • Clear statement of sustainability as an investment objective • Monitoring process followed for sustainability as investment objective • Methodology and screening criteria used for evaluating success in achieving objectives • Data sources and processing methods used • Limitations of data and methodology • Due diligence on underlying investments • Engagement policies for portfolio companies • Description of any index designated as a reference benchmark with the sustainable investment objective of the fund differs from a relevant broad market index (if applicable) • Carbon emissions reduction objective (if applicable) |

• Reporting of extent to which sustainable investment objectives of the fund were met during the period covered by the periodic report

• Top investments • Proportion of sustainability-related investments • Details of the proportion of investments per environmental objective under the EU Taxonomy • The proportion of socially sustainable investments (if applicable) • Reference benchmark (if applicable) |

||||||||||||||||||

Evalueserve's ESG Solutions for Asset and Wealth Management

Uncertainty Prevailing After Implementation of Level 2 Regulatory Technical Standards (RTS)

Several points on SFDR implementation have been clarified through the publication of Level 2 RTS (RTS contains the standardized templates for disclosures on fund requirements). However, asset managers are still trying to understand Article 9 fund requirements, with those related to sustainable investments unclear. This makes it difficult for asset managers to classify their products under the Article 9 label. As a result, many asset managers are trying to play it safe by downgrading their Article 9 funds to Article 8 funds, while a few asset managers are still awaiting clarity from the European Commission on whether Article 9 funds should include only sustainable investments. Others have opted to explain their fund objective and characteristics in an elaborate manner while throwing light on why their investments can be considered as sustainable. According to Bloomberg Intelligence data, more than 70 exchange traded funds (ETFs) with assets worth USD57 billion were downgraded from Article 9 to Article 8 in the last quarter of 2022.

As per our analysis, in the next few months, the majority of ESG fund launches in Europe will follow Article 8 requirements until further clarifications and interpretations are made available.

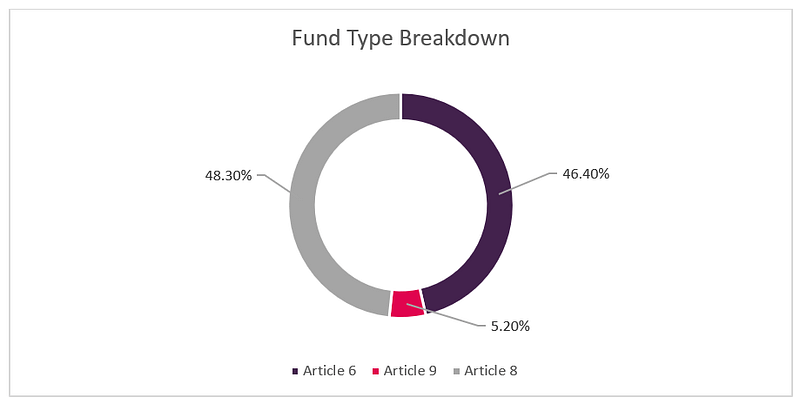

SFDR Fund Type Breakdown by Assets (as of Q3 2022) (1)

How Asset Managers Can Comply with SFDR

- Identify the purpose of the investment product: Asset managers need to figure out the core sustainability objective of their investment product, which will enable them to classify the product under different investment labels.

- Establish a governance framework: Asset managers need to establish a governance structure to guide their strategic decision-making process, help implement sustainability across the business, and ensure overall accountability to investors.

- Conduct a sustainability risk assessment: Asset managers need to conduct a sustainability risk assessment to identify and prioritize sustainability risks that are relevant to their investments. This can help them to better understand the potential impact of sustainability risks on their investments and develop strategies for managing these risks.

- Align products with sustainable investment objectives: Once the sustainability risks are identified, asset managers need to sync sustainability characteristics of the investment product with the relevant reporting requirements. This synchronization can be done by

- Screening investments based on sustainability factors

- Providing transparency to investors and demonstrating commitment to sustainability

- Designing products to meet sustainable investment objectives

- Engaging with companies on ESG issues to encourage them to improve their ESG practices

- Reporting disclosures: Asset managers must consistently report and highlight the necessary disclosures related to the investment products and make these disclosures easily accessible to investors. Disclosures can be made in the following ways:

- In pre-contractual documents: These should include sustainability risk information on the investments and the related decision-making process

- On their websites: Disclosures should be in the form of a policy statement on the inclusion of sustainability factors in their investment decision-making process

- In periodic reports: Disclosures should be in the form of annual reporting on the extent to which their investment products align with sustainability objectives and on the impact of sustainability risks on the investment returns

Challenges Posed by SFDR Compliance Requirements

SFDR poses several challenges for asset managers. Here are some of the key challenges:

- Formulating a sustainability strategy: Given the uncertainty in the characteristics of Article 9 funds post Level 2 RTS implementation, it is a tedious task for asset managers to develop the sustainability strategies of their investment products.

- Functional constraints: Asset managers are required to ensure proper sustainability reporting for their investment products. The operational requisites for this purpose include the requirement for all the teams linked with the product (i.e., development, marketing, and others) to scan the product through the ESG lens. This can be difficult if the asset managers lack in-house ESG expertise.

- Poor data quality: For asset managers, data analysis becomes a challenge due to incomplete or non-standardized sustainability data of portfolio companies. Further, interpretations of sustainability data can be subjective, given that ESG data is more qualitative than quantitative.

- Divergence of ESG ratings: Using ratings from rating agencies can create several challenges for asset managers due to the subjectivity of ESG ratings and the limited coverage of sustainability data. The ratings can be subjective as they are based on differing agency criteria and weightages as well as differing methodologies for assessing ESG factors. The methodologies used by rating agencies may not be transparent, which can make it more difficult for asset managers to understand how the ESG ratings are calculated and to assess the quality of the ratings.

How Evalueserve Can Help

Asset managers that overcome sustainability challenges and effectively integrate sustainability risks and factors into their investment processes may be better positioned to meet the long-term needs of clients and investors. SFDR is an important regulation in this regard, and Evalueserve can help asset managers at multiple steps in the SFDR compliance process. Our hybrid support program, driven by proprietary technology and domain experts, creates value by transforming unstructured ESG information from multiple sources into actionable insights. This allows us to provide a scalable solution that addresses the challenges faced by asset managers as they strive to meet SFDR requirements.

Key Components of Our Unique, Scalable Hybrid Solution

- Technology: Automated tracking of ESG controversies, best practices, and assessment criteria, driven by Insightsfirst, our proprietary AI platform, helps provide early warnings and timely indications of portfolio risk, controversies, and regulatory updates. The platform can be customized as per clients’ internal frameworks and taxonomy and can track a wide range of ESG-related data sources, including news articles, social media, and regulatory filings. This provides clients with up-to-date information on the ESG positioning of companies and the potential controversies that may impact their performance.

- Domain expertise: Our domain experts are well versed with multiple ESG frameworks and can ensure that your ESG data and insights meet the necessary regulatory standards. By leveraging our deep expertise, we can help asset managers collect and provide evidence for ESG assessments and scoring based on the material KPIs and their internal frameworks. We provide gap analysis and deeper insights into portfolio companies’ best practices, in turn providing topics that asset managers can use for further engagement with their portfolio companies. Our experts can also help in the process of constructing portfolios by conducting exclusion screening, thematic research, and industry benchmarking.