An Overview of the US Mortgage Market

The last few years have been a rollercoaster ride for US mortgage markets. However, the year 2025 is expected to be pivotal for US mortgage lenders. Following many years of elevated inflation and subdued growth caused by dislocations from the pandemic, the US mortgage markets could be poised for an upswing. On the back of strong US economy, improving real estate market fundamentals have certainly boosted demand dynamics for mortgage loans.

Residential mortgages have become a core product for US retail banks. However, the US residential market remains challenging amid soaring home prices and muted demand. In the case of commercial real estate (CRE) lending, banks are a bit more vulnerable as more than a trillion-dollar CRE loans will come due in the next two years. Nevertheless, CRE transactional activities have broadly started to stabilize, and tentative signs of asset value growth are returning to the market. However, CRE lending in certain property segments is still under watch. Despite a few challenges, the US banking system remains resilient, with most lenders experiencing limited stress in their mortgage portfolios. In Q4 24, the asset quality metrics remained generally favourable for most of the banks. However, an increase in non-performing mortgage loans could be especially challenging for certain banks.

As the US mortgage market moves through its downturn into recovery, it will provide banks with new opportunities to help make the most of their lending journey. The challenge, though, will be uncertainty around interest rates as mortgage rates haven't come down as quickly as the market expected. Banks will have to cautiously watch the green shoots that are expected to drive mortgage lending business in 2025 and beyond. How banks choose to navigate the upcoming 6 to 12 months could be crucial in adapting to the new foundational realities shaping the US mortgage industry.

This blog gives a comprehensive analysis of anticipated trends in US mortgage markets, highlighting key areas of risk and opportunity that may arise in the year ahead.

US Mortgage Market Size and Growth Dynamics

Size and Volume Growth of Mortgage Market

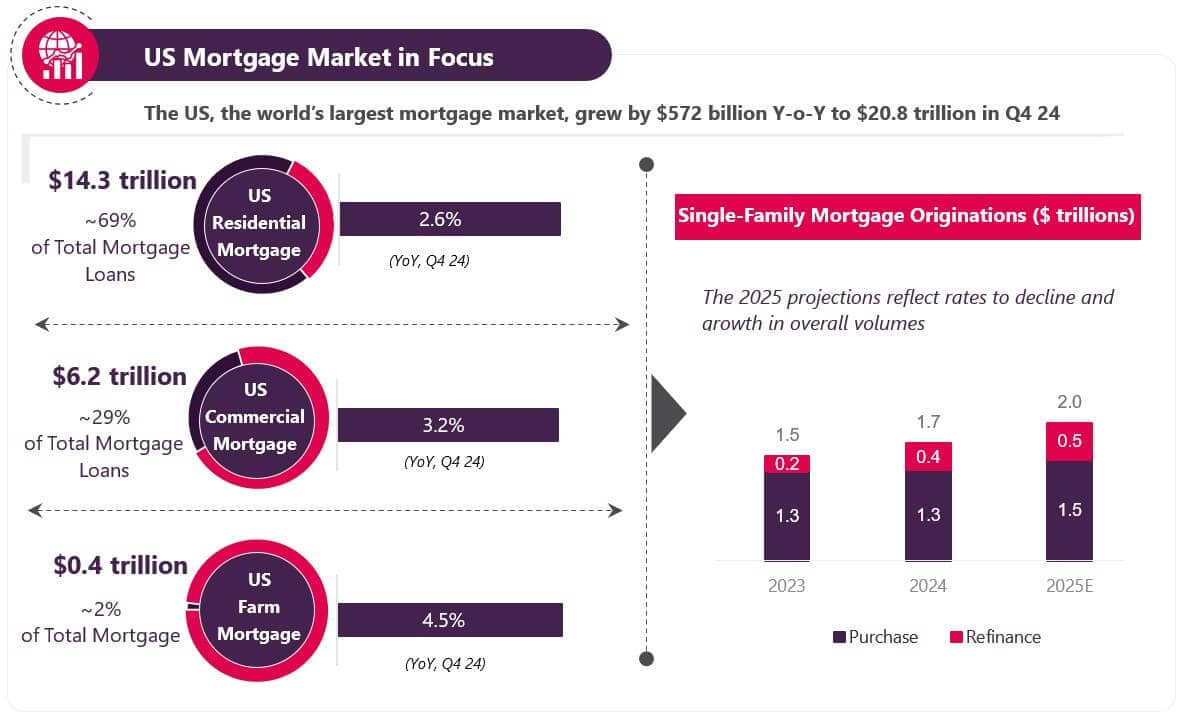

The US mortgage market is among the largest in the world, with an outstanding debt of approximately $20.8 trillion. The residential mortgage market, valued at $14.3 trillion, represents the largest segment. CRE loans, totalling ~$6.2 trillion, also constitute a significant portion of the mortgage market and remain a major business for many commercial banks in the US. The CRE market is divided into five major segments: multifamily, industrial, lodging, retail, and office. Each segment has its own characteristics, making it essential for banks to closely monitor developments within their specific CRE market areas to ensure successful CRE lending.

In the US, almost all banks participate in CRE lending, and their balance sheets reflect substantial holdings of CRE loans. With a share of 38% (~ $1.8 trillion), commercial banks and thrifts hold the largest share of commercial/multifamily loans as reported by Mortgage Bankers Association in its Q4 24 Commercial / Multifamily Quarterly Databook. In Q4 24, commercial and multifamily mortgage loan originations witnessed strong growth, increasing by 84% Y-o-Y and 30% Q-o-Q. However, US single-family mortgage originations showed mixed results, with refinancing activity on the rise and purchase originations on the decline. According to ATTOM’s Q4 24 Residential Property Mortgage Origination Report, the volume of purchase loans fell by 5.5% Q-o-Q to $289.7 billion, which is 45.7% below the peak seen in 2021. Despite higher interest rates, the volume of refinance loans increased to $228.5 billion in Q4 24, marking a 15.7% Q-o-Q growth. This represents the third consecutive quarterly gain, reaching the highest level since mid-2022.

CRE Lending Dynamics – Emerging Green Shoots in 2025

Manageable Cyclical Challenges

The CRE market is a highly rate-sensitive asset class. The US mortgage rates have jumped by most in April 2025, around 6.83%, as tariffs fear hit the CRE markets. Therefore, most banks have been effectively monitoring their CRE loan portfolio and proactively reserving against any potential losses from mortgage exposure. In 2025, the demand for CRE loans is expected to grow, primarily due to institutional lenders, including government-sponsored enterprises (GSEs) and insurance companies. While CRE markets still have plenty of challenges, there are also signs of stabilization. Therefore, credit losses are not likely to put much pressure on 2025 earnings. The office properties will continue to face structural changes and valuation pressures. The weak demand for office space can affect the repayment and refinancing ability of office borrowers. Growing demand for logistics and e-commerce has boosted the expansion of warehouses and other industrial property projects.

Roughly over $1.7 trillion of US CRE mortgages are estimated to mature between 2024 and 2026. These loans will have to be refinanced. However, with the sharp increase in rates over the last few years, these borrowers may struggle to meet their debt service payments. The rates are expected to drop, which will marginally improve refinancing prospects and debt service on floating-rate loans. However, if rates remain elevated, there will continue to be pressure on NOI for multifamily borrowers, especially those on interest-only loans.

In the April 2025 survey conducted by the Federal Reserve (Fed), senior loan officers reported that banks maintained tighter or unchanged lending standards and experienced weaker or unchanged demand for CRE loans. Despite the ongoing challenges, these results show a slight improvement compared to previous surveys, indicating early signs of stabilization and potential improvement in 2025. Large banks have eased standards for construction and land development as well as multifamily loans, while keeping standards for nonfarm nonresidential loans unchanged. In contrast, smaller banks have tightened standards across all categories, particularly by lowering loan-to-value ratios and increasing debt service coverage ratios. The primary reasons for tightening lending policies include less favorable or uncertain outlooks for CRE property vacancy rates, property prices, market rents, mortgage delinquency rates, and a reduced tolerance for risk.

On the demand side, large banks reported stronger demand for all types of CRE loans, driven by increased customer refinancing of maturing loans, higher customer acquisition, and lower interest rates. However, smaller banks experienced weaker demand due to decreased customer acquisition, higher interest rates, concerns over rental demand, and borrowers shifting to nonbank lenders.

The Outlook for the Mortgage Market in 2025

The outlook for the 2025 CRE continues to be positive, but with several variables at play, banks are cautiously optimistic about their lending approach. The housing market also has a few vulnerabilities due to hardening rates and subpar rental economics.

CRE prices faced downward pressure in the last couple of years as high interest rates dragged property values down. However, the real estate market improved in 2024 and is expected to perform much better in 2025. Due to supply-demand imbalances, the US real estate market is also creating structural opportunities for mortgage lenders. Stabilizing rates and a strong economic environment have improved asset values. In the previous cycle, real estate write-downs have typically come from weakening fundamentals. However, the current cycle has been different. CRE could be at a turning point, but banks should focus on CRE opportunities with strong fundamental dynamics. Excluding office assets, operating metrics across the industry are on relatively solid ground. Due to trends like e-commerce and AI, certain sub-sections of CRE, such as data centres, logistics, and telecom towers, are well-positioned.

The US residential market is likely to remain lacklustre for lenders in 2025 as the housing market is expected to grow at a subdued pace of around 3%. Low vacancy data suggests potential supply constraints. This situation will continue unless mortgage rates drop below 5%.

Modernizing Corporate Lending Technology Stack

GenAI Applications for Next-Gen Mortgage Operating Model

Banks must adopt a modern technology stack to streamline the end-to-end loan servicing life cycle, and GenAI can play a significant role. AI has the capability to excel at synthesizing insights from massive unstructured data, interpreting critical conversations, and quizzing large data sources across loan servicing life cycle issues.

With a GenAI interface, banks and nonbanks are bringing significant improvements to origination, processing, underwriting, and loan servicing. Most of the industry-leading players are technology-driven companies that have invested heavily in GenAI technologies across the value chain to automate underlying processes. United Wholesale Mortgage (UWM), the largest wholesale mortgage lender in the US, is working with Google Cloud to modernize the mortgage lending industry using AI. UWM will use Google Cloud's Gen-AI and data analytics to improve the mortgage process for 50,000 mortgage brokers and their clients, focusing on speed, efficiency, and personalized service.

As per the Fannie Mae Mortgage Lender Sentiment Survey released in 2023, lenders cited improving operational efficiency as the dominant factor for AI/ML adoption. Lenders are using AI applications to automate compliance management, underwriting data verification, processing, and appraisal. Despite the growing interest, the survey highlighted that lenders’ familiarity with AI/ML, adoption status, and adoption challenges remained largely the same as in 2018.

How Evalueserve Can Support Banks in the Mortgage Process

Evalueserve supports major banks around the globe with technology-enhanced services across the lending lifecycle. We partner with corporate and commercial banks to improve efficiency and accuracy and meet the demands of a changing market and heightened regulatory scrutiny. We combine domain expertise with technology accelerators, such as AI-powered Spreadsmart, to help banks make faster, smarter credit decisions.

Talk to One of Our Experts

Get in touch today to find out about how Evalueserve can help you improve your processes, making you better, faster and more efficient.