Introduction

Hydrogen is fast gaining ground as the fuel of the future, be it for power generation or powering the next generation of fuel cell electric vehicles (FCEVs). Hence, ways to generate, transport, and utilize it to fuel this energy transition are constantly being developed and optimized. Amongst these, electrolysis is a major Power-to-X (PtX) solution pathway to generate green hydrogen using electricity and water. Alkaline electrolysis (AE) and proton exchange membrane (PEM) are the currently marketed electrolysis processes in this direction.

However, a new process could soon change things – solid oxide electrolysis cell (SOEC). While it faces the challenges of any new technology, SOEC presents a wholly more efficient way to generate hydrogen. We look at where SOEC technology stands and the decarbonization opportunities it presents for a future driven by the net-zero carbon emissions by the 2050 goals of checking greenhouse gas (GHG) emissions and limiting global temperature rise to under 1.5 degrees Celsius (℃).

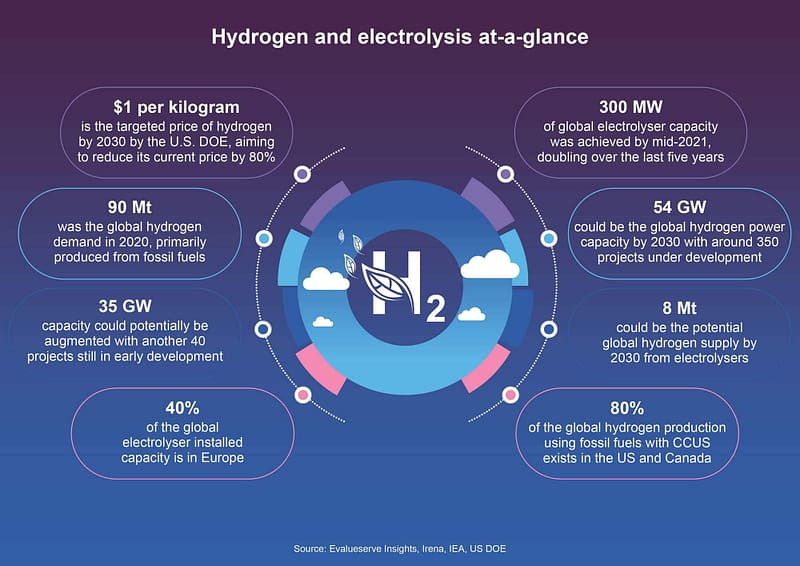

Hydrogen and electrolysis at glance

$1 per kilogram is the targeted price of hydrogen by 2030 by the U.S. DOE, aiming to reduce its current price by 80%

300 MW of global electrolyser capacity was achieved by mid-2021, doubling over the last five years

90 Mt was the global hydrogen demand in 2020, primarily produced from fossil fuels

54 GW could be the global hydrogen power capacity by 2030 with around 350 projects under development

35 GW capacity could potentially be augmented with another 40 projects still in early development

8 Mt could be the potential global hydrogen supply by 2030 from electrolysers

40% of the global electrolyser installed capacity is in Europe

80% of the global hydrogen production using fossil fuels with CCUS exists in the US and Canada

Source: Evalueserve Insights, Irena, IEA, US DOE

What is SOEC?

Solid oxide electrolysis cell (SOEC) is an early commercialization-stage technology to generate green hydrogen. In most cases, it is essentially a stack of solid oxide fuel cells (SOFCs) running in regenerative mode, or in reverse, to achieve electrolysis. While SOFCs store electric energy, SOECs reverse this by feeding electricity to output hydrogen. Operating at high temperatures and hence running at high efficiency, this type of electrolysis splits water into hydrogen (H2) and oxygen (O2) on the two sides of the cell. SOECs can produce green hydrogen using surplus (intermittent) electricity from wind turbines as well as other sustainable sources. This hydrogen can then be stored in fuel cells and later be reconverted into electricity depending upon the demand, ensuring safe energy storage when production exceeds demand.

UNKNOWNS

What is the potential growth target for SOEC technology, factoring in application areas, value-chain creation and, hence determining its overall market?

How does it compare with Alkaline and PEM?

Advantages of SOEC

+ SOEC brings a completely different level of voltage efficiency to the table, compared to the current technologies

+ It does not require rare-earth metals for the process, unlike PEM, making the sourcing of materials and setup easier, lowering material costs

+ Lower working pressure of the SOEC process translates into fewer requirements for high-precision or zero-tolerance devices and could benefit longer-term usage and maintenance

+ SOECs can be operated in reverse mode to turn back into a solid oxide fuel cell for energy storage.

+ The SOEC stacks can also be used in a co-electrolysis mode to produce syngas. SOECs can be beneficial in future integration with downstream synthesis processes for the production of chemicals and fuels including methane, methanol, gasoline, diesel, jet fuel and ammonia.

+ With all its components being solid, the need for maintenance towards electrolyte loss and electrode corrosion is eliminated

+ Higher current densities compared with PEM mean that SOECs can present lower capital costs, requiring fewer stacks to achieve a specific output.

+ This technology is being prepared to go-to-market (GTM), meaning that setting up, optimizing, and embedding into its value chains could give an early-adopter advantage

UNKOWNS

How green are the different electrolyser value chains comparatively, and what level of overall carbon neutrality can be achieved within each?

Challenges for SOEC

– Comparatively higher costs as SOECs have not yet reached full commercialization, and do not currently compete with Alkaline or PEM processes in this regard

– SOEC does have higher operating temperatures, which can increase stress on the components leading to severe material degradation

– Due to the higher temperatures, the cold-start time for SOEC is comparable to Alkaline electrolysis, which is longer than what PEM offers

– SOEC stacks currently have a comparatively shorter life, which can be improved greatly with ongoing research and development

Current applications and outlook

SOECs have moved into the demonstration stages, albeit in small capacities. While alkaline electrolysers have been used for a long, PEM electrolysers have seen strong growth since 2015, and gained relative market share owing to their quicker cold-start times and dynamic behavior. This is reflected in their installed capacities, with a large chunk being located across Europe.

Alkaline electrolyser capacity reached the range of 176 MW by the end of 2020, while that of PEM electrolysers grew from 19 MW in 2015 to 89 MW by 2020-end. SOECs meanwhile have just started showing up on the map, going from a few hundred kW in 2019 to 1 MW at the end of 2020, and now some projects are aiming for 20 MW scale-ups using high-efficiency SOECs in the near term.

Sunfire recently announced a successful test operation of its Generation–2 225 kW electrolysis module, which will add 12 such SOEC modules for a 2.7 MW output system. Haldor Topsoe is preparing for a bigger SOEC future with an announcement of investing in a SOEC manufacturing facility with a capacity of 500 MW worth of electrolysers per year, with the option to scale up electrolyser production to a whopping 5 GW. The facility will be operational in 2023, according to the manufacturer.

Conclusion

It appears that the few players involved in the SOEC space are betting big on its prospects. This is natural as the technology nears commercialization towards a future defined by the use of green hydrogen as one of the primary fuels. This is apparent from the major announcements from governments and bodies across Germany, Denmark among other geographies.

In fact, Germany, just announced sticking primarily with green hydrogen under its national hydrogen policy, in a move that could both speak to its aim for self-sufficiency in the future of green energy as well as having a robust presence in the energy transition for the EU and the rest of the world. The nation had previously also showcased its PtL roadmap for aviation fuels under this policy. There are various other examples from different geographies and economies.

SOEC development will continue well into the future even after it achieves complete marketability. While it certainly needs to meet the cost targets, a better understanding of the processes during electrolysis will keep yielding increased performance and lifetime gains – areas where it needs to be proven. Waste heat from existing processes such as methanol and ammonia syntheses can be utilized to economize on the electrolysis process of SOECs, for example.

More importantly, as it achieves closer value-chain integration with intermittent renewable (wind, solar etc.) electricity sources, SOEC technology will get the boost it needs to scale up to its cost-competitiveness targets. The time is now, as more economies align their policies to favor efficient energy conversion technologies such as SOECs to meet their net-zero goals with each passing day.

Download the full industry insight here.